The surplus of CORSIA-eligible carbon credits is projected to turn negative by 2030 unless new supplies become available, according to an analysis by Abatable.

Currently, the aviation sector contributes about 3% of global emissions. As a sector that’s difficult to decarbonize, it’s exploring direct low-carbon technological solutions like sustainable aviation fuel (SAF) and electrification. However, these solutions face cost and technological hurdles and will take time to become widespread.

The Challenge of Decarbonizing Aviation

To mitigate emissions in the meantime, the International Civil Aviation Organization (ICAO) launched the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) in 2016. CORSIA aims to offset any growth in aviation emissions above 85% of 2019 levels.

CORSIA entered its first phase in January this year, after a pilot period from 2021 to 2023. Phase 1, which runs from 2024 to 2026, is voluntary for participating states, while Phase 2 will be mandatory starting in 2027.

- To comply, airlines can purchase SAF, enhance fleet efficiency, or buy CORSIA-eligible carbon credits.

However, the rollout has been challenging. In March, major carbon credit issuers Verra, Gold Standard, and Climate Action Reserve (CAR) were only conditionally approved by ICAO’s Technical Advisory Body. This status will be reconsidered in September following a resubmission process completed in April 2024.

Currently, CORSIA Phase 1 credits can only be acquired through the American Carbon Registry (ACR) and ART TREES standards. Additionally, CORSIA credits require Letters of Authorization from host countries, further limiting the supply.

As of now, the only recent issuance eligible for the scheme is 7.1 million Guyana ART credits. The ICAO Technical Advisory Body’s decision suggests that this limited supply situation may persist throughout 2024.

Demand to Outpace Supply by 2030

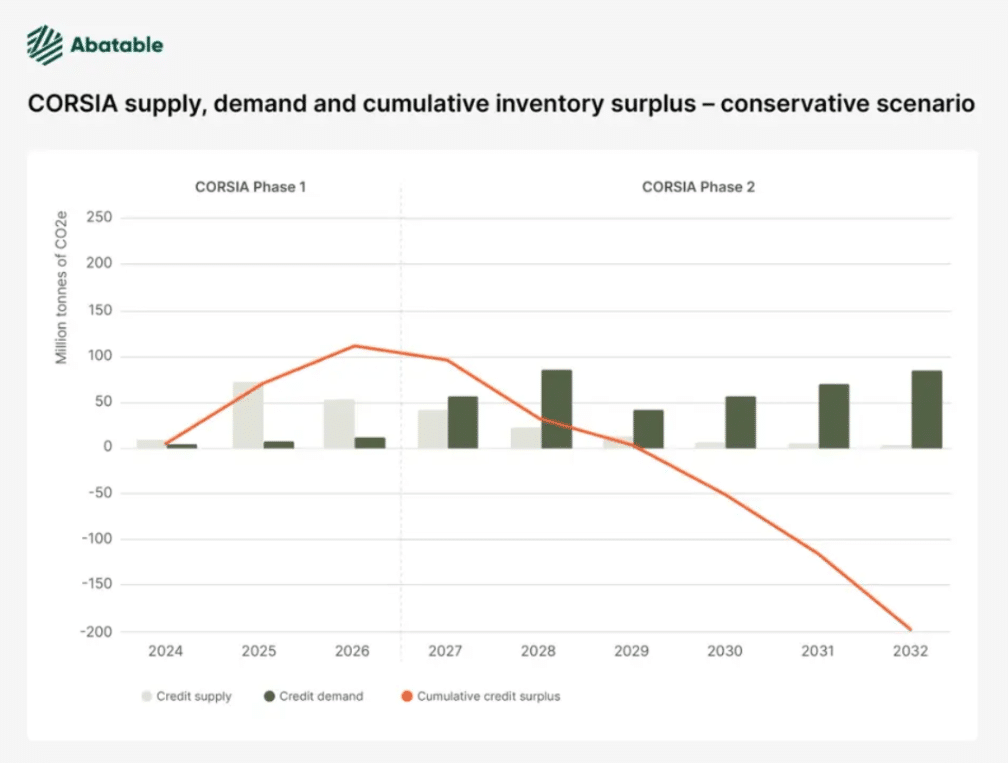

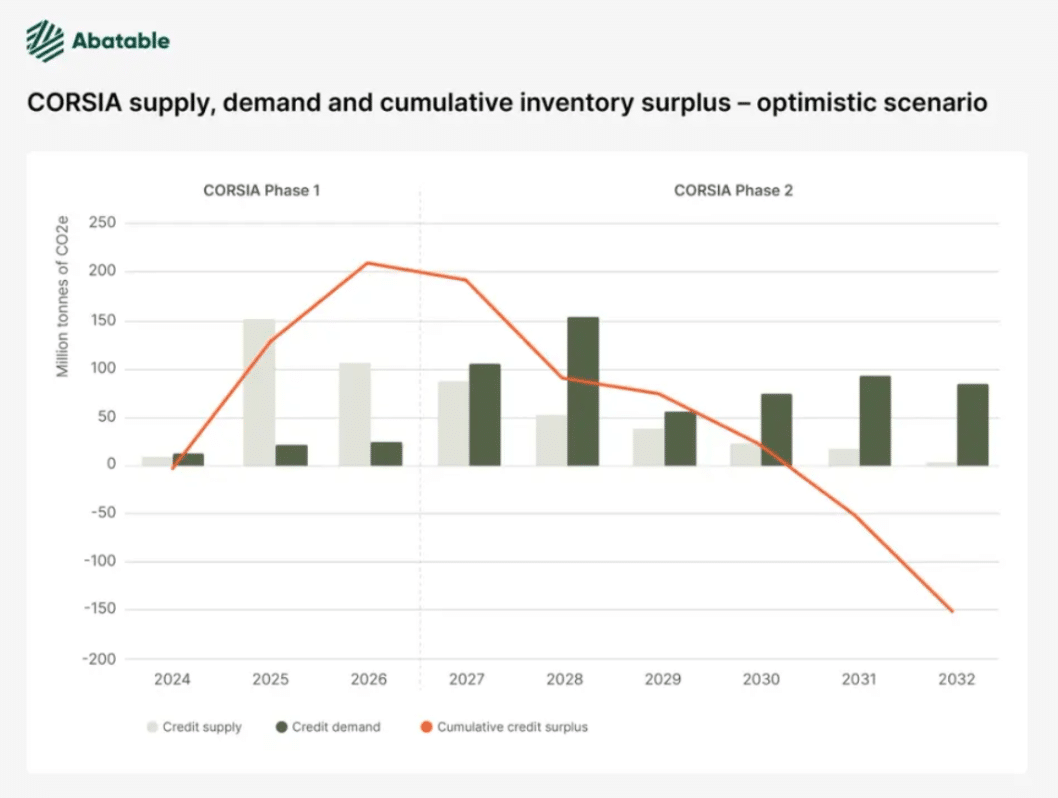

Abatable’s analysis indicates that, under current market conditions and without new supplies, demand for CORSIA credits will exceed supply by 2030. In Phase 2 of the scheme, demand is projected to outpace supply between 2029 and 2030.

In a conservative scenario, CORSIA demand does not exceed 100 million credits until after 2034. However, supply peaks in 2025 and can only meet demand until 2029. Without new projects, demand in Phase 2 could be 14x larger than supply.

In an optimistic scenario, aviation emissions return to 85% of 2019 levels this year, with CORSIA demand surpassing 100 million carbon credits in 2027. Supply, bolstered by projects likely to receive corresponding adjustments, meets demand until 2030. Without new projects, demand in Phase 2 could be 7x larger than supply.

Abatable’s projections include existing projects expected to meet the Integrity Council for the Voluntary Carbon Market’s Core Carbon Principles and likely to receive corresponding adjustments. Supply from Verra, Gold Standard, and CAR is expected from 2025.

CORSIA’s design interfaces with the Paris Agreement’s Article 6, allowing countries to trade emissions reductions to meet Nationally Determined Contributions (NDCs). Corresponding adjustments ensure accurate progress toward NDCs and prevent double counting. These adjustments are required for CORSIA credits, allowing them to be transferred internationally.

However, delays in implementing Article 6 mechanisms could affect CORSIA. While details are being developed, projects receiving Letters of Authorization can list on voluntary market registries as Article 6 compliant. Biennial UN reports will confirm national accounting and the application of corresponding adjustments.

A significant challenge is the liability for the revocation of authorized credits. ICAO’s Technical Advisory Body suggests that standards or project proponents should assume liability, while standards argue it should lie with the revoking country. COP29 decisions may influence this issue, potentially causing even more delays.

Market Response and Developments

The market is reacting to these developments. New commercial structures and carbon insurance products are under conception to mitigate risks and encourage trading activity. These products aim to provide confidence to market participants and enhance liquidity, especially given the current market uncertainties.

So, what’s next for this development in CORSIA carbon credits?

Verra, Gold Standard, and CAR have re-submitted their applications, and the Technical Advisory Board will reassess these in September 2024. If they fail, new supply sources will be delayed until 2025, extending beyond current projections.

To mitigate supply issues, standards should work toward approval while also building capacity to help countries develop market infrastructure and governance for authorizing credits with corresponding adjustments. Large CORSIA participants might invest in upstream projects, although this would require market understanding and time to generate a credit stream and gain necessary adjustments.

Airlines are not required to purchase credits until Phase 1 concludes in January 2028. However, some may buy and retire credits in advance, based on projected obligations from historical emissions data. Final emissions reports and audits will be completed in 2027, indicating that the total credits needed, leading to an increase in credit retirements.

The availability of credits post-2027 will depend on decisions by ICAO, Article 6 negotiators, and governments, as well as the emergence of new supply sources. The actions taken in the interim will be crucial for ensuring there are enough carbon credits to meet future demand.

The future of the CORSIA carbon credit market hinges on increasing the supply of eligible credits. Abatable’s analysis underscores the need for new projects and corresponding adjustments to meet the rising demand by 2030. While pursuing low-carbon technologies, the aviation sector must rely on carbon offsets in the interim.