More and more firms are pledging to contribute to climate change mitigation by reducing their own greenhouse-gas emissions as much as possible. Many businesses, however, realize that they are unable to entirely eliminate or even reduce their emissions as quickly as they would want.

The job is more challenging for businesses striving for net-zero emissions, which means eliminating the same amount of greenhouse gas from the environment as they put into it. Many people will be forced to use carbon credits to offset emissions that they cannot reduce via other means.

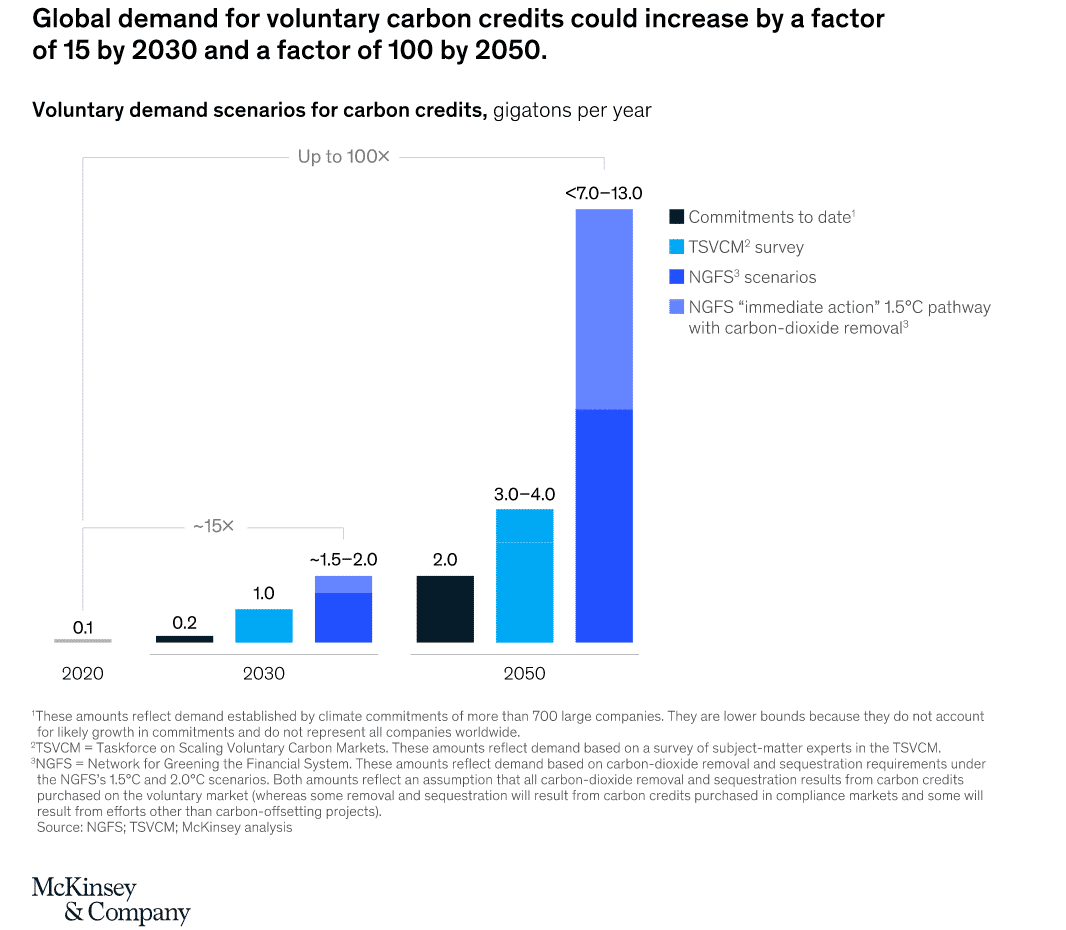

The Taskforce on Scaling Voluntary Carbon Markets (TSVCM) of the Institute of International Finance (IIF) predicts that demand for carbon credits would increase by a factor of 15 or more by 2030, and by a factor of up to 100 by 2050.

By 2030, the carbon credit market may be worth more than $50 billion.

The market for freely obtained carbon credits (rather than for compliance purposes) is significant for a variety of reasons. Voluntary carbon credits redirect private financing to climate-action projects that would not be possible otherwise.

These activities might include biodiversity conservation, pollution avoidance, public-health improvements, and job development. Carbon credits also stimulate investment in the required innovation to bring the cost of new climate technologies down.

Furthermore, larger voluntary carbon markets would allow money to be mobilized to the Global South (Latin America, Asia, Africa, and Oceania) where the most cost-effective nature-based emissions-reduction efforts exist.

Given the anticipated demand for carbon credits from global attempts to reduce greenhouse-gas emissions, the world will require a large, transparent, verifiable, and environmentally sound voluntary carbon market.

However, the market today is fragmented and complex. Some credits were discovered to indicate emissions reductions that were, at best, questionable. Consumers are unsure if they are paying a fair price, and suppliers are unsure how to handle the risk of investing and working on carbon-reduction efforts without knowing how much consumers would eventually pay for carbon credits.

Using carbon credits to achieve climate change goals

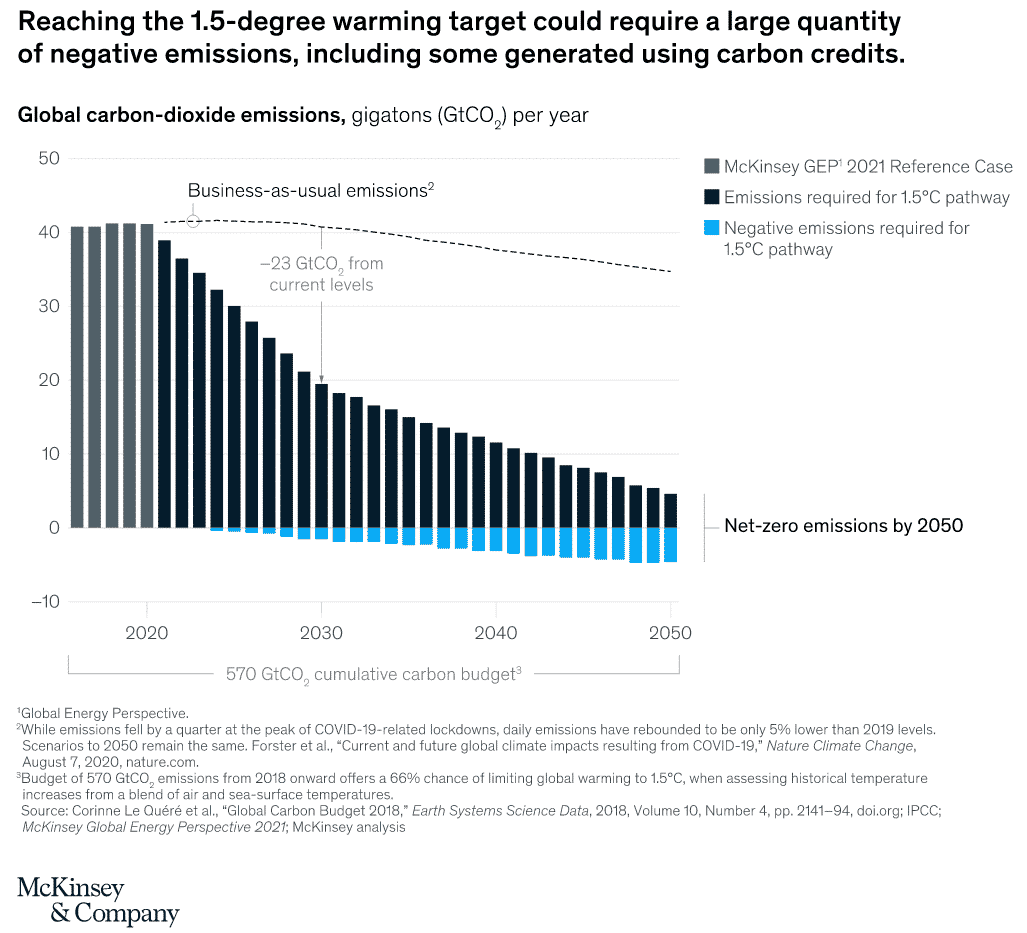

The 2015 Paris Agreement, ratified by almost 200 countries, established a global aim of limiting average temperature rises to 2.0 degrees Celsius over preindustrial levels, ideally 1.5 degrees.

To reach the 1.5-degree target, global greenhouse-gas emissions must be reduced by half by 2030 and to zero by 2050.

More companies are embracing this movement: in less than a year, the number of organizations with net-zero pledges has more than quadrupled, from 500 in 2019 to over 1,000 in 2020.

To reach the global net-zero goal, companies must reduce their own emissions as much as feasible (while also measuring and reporting on their progress, to achieve the transparency and accountability that investors and other stakeholders increasingly want).

However, lowering emissions using today’s technology is too expensive for certain firms, even though the costs of those technologies may reduce over time. Furthermore, many causes of pollution cannot be eliminated at all businesses.

For example, large-scale cement production often necessitates a chemical process known as calcination, which accounts for a sizable percentage of the cement sector’s carbon emissions. Because of these restrictions, the emissions-reduction strategy for achieving a 1.5-degree target essentially requires “negative emissions,” which are achieved by removing greenhouse gases from the atmosphere.

The chart below shows what needs to be done going forward to meet that target.

Purchasing carbon credits is one way for a company to deal with emissions that it cannot eliminate. Carbon credits are certificates that represent the quantity of greenhouse emissions kept out of or removed from the atmosphere.

While carbon credits have been around for a while, the voluntary carbon credit market has grown significantly in recent years. According to McKinsey, buyers will retire carbon credits totaling about 95 million tonnes of carbon-dioxide equivalent (MtCO2e) in 2020, more than double the quantity retired in 2017.

As attempts to decarbonize the global economy ratchet up, voluntary carbon credits may become increasingly popular.

Based on stated demand for carbon credits, demand projections and the volume of negative emissions required to meet the 1.5-degree warming goal, McKinsey estimates that annual global demand for carbon credits could reach 1.5 to 2.0 gigatonnes of carbon dioxide (GtCO2) by 2030 and 7 to 13 gigatonnes of carbon dioxide (GtCO2) by 2050.

The market size in 2030 might vary from $5 billion to $30 billion at the low end to more than $50 billion at the high end, depending on pricing assumptions and underlying variables.

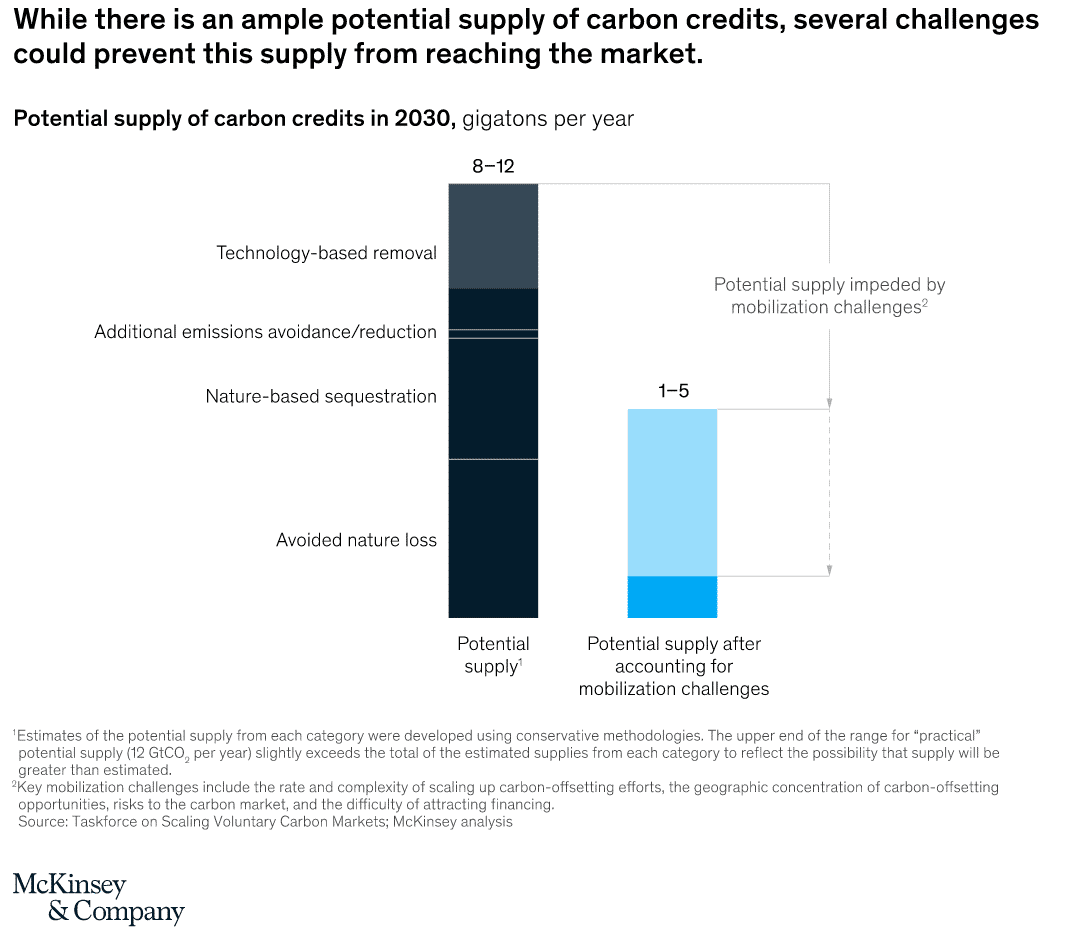

Despite the fact that demand for carbon credits has grown substantially, McKinsey predicts that demand in 2030 may be fulfilled by the potential annual supply of carbon credits: 8 to 12 GtCO2 per year.

These carbon credits would come from four sources: avoided nature loss (including deforestation); nature-based sequestration, such as reforestation; avoidance or reduction of landfill emissions, such as methane; and technology-based removal of CO2 from the atmosphere.

A variety of factors, however, may make mobilizing and bringing the entire potential supply to market challenging. The development of the project would have to be accelerated at an unprecedented rate.

The majority of the potential supply of avoided environmental degradation and natural-based sequestration is concentrated in a few countries. Many sorts of projects may fail to acquire finance due to the large lag times between the initial investment and the ultimate sale of credits.

When these restrictions are considered, the expected supply of carbon credits by 2030 decreases to 1 to 5 GtCO2 per year.

These aren’t the only problems that carbon credit buyers and sellers confront. Due to variations in accounting and verification procedures, as well as co-benefits of credits (such as community economic development and biodiversity protection) that are rarely fully specified, high-quality carbon credits are scarce.

When it comes to evaluating the quality of new credits, suppliers have considerable lead times, which is a critical step in maintaining the market’s integrity. When it comes to selling such credits, suppliers face unpredictable demand and rarely receive competitive price.

Overall, the market is marked by a lack of liquidity, inadequate financing, poor risk-management services, and limited data availability.

These challenges are significant, but they are not insurmountable. Verification techniques may be improved, and verification procedures can be made simpler.

Clearer demand signals would instill greater confidence in suppliers’ project plans and encourage investors and lenders to provide funds. All of these requirements can be met if a large-scale voluntary carbon market is carefully developed.

A fresh action plan is required to scale up voluntary carbon markets and a multi-pronged strategy would be required to establish a viable voluntary carbon market.

In its analysis, the TSVCM identified six areas along the carbon-credit value chain where action may help the voluntary carbon market scale up.

1. Creating standardized criteria for finding and verifying carbon credits

Because carbon credits are so varied, the voluntary carbon market presently lacks the liquidity needed for effective exchange. Each credit is related to the underlying project in some way, such as the type of project or the area in which it was completed.

Because buyers assess additional features differently, these variables influence the credit’s cost. Overall, credit irregularity indicates that linking a single buyer with a corresponding provider is a time-consuming, inefficient over-the-counter procedure.

If all credits could be established using identical qualities, buyer-supplier matching would be more efficient. The first set of qualities is concerned with quality. The quality criteria specified in the “core carbon principles” would serve as the framework for assessing whether carbon credits represent genuine emissions reductions.

The second set of attributes would cover the additional properties of the carbon credit. Standardizing such characteristics in a unified taxonomy will aid suppliers in marketing credits and consumers in identifying credits that meet their needs.

2. Getting contract with Standardized terms

Because of the diversity of carbon credits available in the voluntary carbon market, particular types of credits are exchanged in quantities too small to provide meaningful daily price signals. Making carbon credits more consistent would concentrate trade activity on a few types of credits while also boosting market liquidity.

Following the establishment of the aforementioned fundamental carbon principles and standard features, exchanges may create “reference contracts” for carbon trading. A core contract based on fundamental carbon ideas would be included, with further features specified and paid individually according to a standard taxonomy. Core contracts would make it easier for corporations to purchase large quantities of carbon credits at once: they could bid on credits that met certain criteria, and the market would aggregate smaller quantities of credits to meet their bids.

Another advantage of reference contracts is the ability to maintain a constant daily market price. Even if reference contracts are developed, many parties will continue to deal over the counter (OTC). Prices for credits traded via reference contracts might serve as a starting point for OTC trade talks, with other characteristics priced separately.

3. Setting up trading and post-trade infrastructure

A strong, adaptable infrastructure would enable the voluntary carbon market to function smoothly, allowing for high-volume listing and trading of reference contracts as well as contracts with a limited, regularly stated set of additional characteristics. As a consequence, project developers would benefit from the creation of structured finance solutions.

It is also necessary to have post-trade infrastructure such as clearinghouses and meta-registries. Clearinghouses would aid in the development of a futures market while also protecting against counterparty default. Meta-registries would provide buyers and suppliers with custodial services and enable the creation of consistent issue numbers for specific projects (similar to the International Securities Identification Number, or ISIN, in capital markets).

A robust data infrastructure would also increase the transparency of reference and market data. All environmental and financial markets need sophisticated and up-to-date information. Due to restricted data availability and the difficulties of following the OTC market, transparent reference and market statistics are currently unavailable. Buyers and suppliers would benefit from new reporting and analytics services that combine freely accessible reference data from multiple registries via APIs.

4. Getting a common consensus on Carbon Credits

Credits are viewed with skepticism in the context of decarbonization. Some experts are skeptical that businesses will reduce their own emissions much if they had the option of offsetting emissions instead. As part of a wider effort to attain net-zero emissions, businesses would benefit from clear guidance on what constitutes an environmentally efficient offsetting plan. Carbon credit principles would help to ensure that carbon offsetting does not preclude other efforts to decrease emissions and resulting in greater carbon reductions than would otherwise occur.

In accordance with such rules, a company would first calculate its need for carbon credits by disclosing its overall greenhouse-gas emissions, as well as its goals and methods for reducing emissions over time. To compensate for emissions from sources that it can eventually eliminate, the company may purchase and “retire” carbon credits (claiming the reductions as their own and withdrawing the credits from the market, so that another organization cannot claim the same reductions). It may also use carbon credits to offset “remaining emissions” that it will be unable to eliminate in the future.

5. Ensuring Market Integrity

Concerns regarding the integrity of the voluntary carbon market stymie its spread in a number of ways. For starters, the varied nature of credit increases the likelihood of errors and fraud. Money laundering is also a possibility due to the market’s lack of pricing transparency.

One corrective measure would be to implement a computerized system for project registration, credit verification, and issue. Verification organizations should be able to track a project’s impact on a regular basis, not only at the end. A digital approach may minimize issuance costs, shorten payment times, accelerate credit issuance and cash flow for project developers, allow credits to be traced, and boost the credibility of corporate offset claims.

Other upgrades would include the implementation of anti-money-laundering and know-your-customer regulations to prevent fraud, as well as the formation of a regulatory body to check market participants’ eligibility, regulate their behavior, and oversee the market’s operation.

6. Building Demand

Finding an effective way for carbon credit buyers to express their future needs will help incentivize project developers to increase carbon credit supply. Long-term demand signals might include promises to reduce greenhouse gas emissions or upfront agreements with project developers to acquire carbon credits from future developments. To measure medium-term demand, a registry of commitments to purchase carbon credits may be utilized.

Consistent, widely accepted guidelines for companies on acceptable uses of carbon credits to offset emissions; increased industry-wide collaboration, in which consortiums of companies align their emissions-reduction goals or establish shared goals; and improved standards and infrastructure for the development and sale of consumer-oriented carbon credits are all possible ways to promote demand signals.

To keep global warming to 1.5 degrees Celsius, net greenhouse-gas emissions must be reduced quickly and significantly. While companies and other organizations may achieve the majority of the needed reductions by implementing new technologies, energy sources, and operating techniques, many will need to supplement their own abatement efforts with carbon credits in order to achieve net-zero emissions. A strong, well-functioning voluntary carbon credit market would make it easier for companies to locate reputable carbon credit suppliers and execute transactions on their behalf.

Furthermore, such a market would be capable of communicating signs of buyer interest, motivating suppliers to increase credit supply. A voluntary carbon market would speed up the transition to a low-carbon future by allowing for more carbon offsetting.