The rise of Direct Lithium Extraction (DLE) technology promises to open up new sources of lithium supply this decade, potentially helping to avert a forecasted shortfall. According to a new Benchmark special report, DLE represents a group of technologies that selectively extract lithium from brines. This novel technology offers a significant shift in the lithium supply landscape.

What is Direct Lithium Extraction?

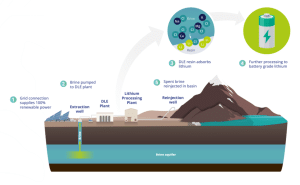

DLE is a well-established technology with operational projects in China and South America. The process begins with extracting brine from aquifers, which is then transported to a processing unit. Here, lithium is selectively extracted using a resin or adsorption material, while the spent brine is reinjected into the aquifer, ensuring no depletion or environmental damage.

The resin captures or adsorbs lithium chloride (LiCl) from the brine. Then the captured lithium is stripped with water, creating a lithium eluate. This eluate undergoes further concentration through reverse osmosis and mechanical evaporation before being processed into battery-grade lithium using industry methods.

One of the key advantages of DLE is its ability to reduce the environmental impact compared to traditional extraction methods. Conventional techniques often lead to soil degradation, water pollution, and destruction of habitats and biodiversity. In contrast, DLE minimizes these issues by avoiding extensive evaporation ponds and using selective extraction methods.

Moreover, DLE technologies help lower the carbon footprint of lithium extraction by reducing energy consumption and greenhouse gas emissions. By employing more efficient and targeted extraction methods, DLE significantly cuts the energy required compared to traditional techniques.

This efficiency contributes to the decarbonization of the energy sector, making DLE a crucial technology for reducing the overall environmental impact of lithium production.

- COMPANY SPOTLIGHT: The Fastest Growing North American Lithium Junior

Current and Future DLE Production

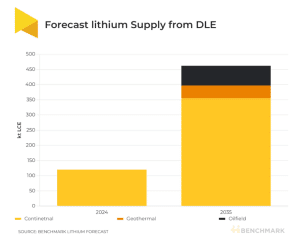

Currently, there are 13 operational DLE projects projected to produce about 124,000 tonnes of lithium chemicals in 2024. By 2035, DLE is expected to contribute 14% of the total lithium supply, amounting to around 470,000 tonnes of lithium carbonate equivalent (LCE), as per Benchmark’s Lithium Forecast.

While most of this supply will come from continental brines, geothermal and oil fields could contribute 9% and 14% respectively.

- CHECK OUT live lithium prices here.

The Role of DLE in New Brine Projects

Almost 75% of new brine projects are expected to use some form of DLE. This highlights the growing importance of unconventional lithium sources and the expanding ecosystem of new players in the lithium value chain, especially oil companies that bring substantial capital and expertise.

Despite its potential, DLE’s path to commercialization faces several challenges, including:

- issues with scalability,

- inflationary pressures, and

- delays at new brine projects.

Technical risks also pose hurdles for new investors. Benchmark’s DLE special report outlines various DLE technologies, including adsorption, ion exchange, solvent extraction, and membranes, with adsorption being the most widely adopted and best-established, particularly in China.

Each brine source is unique in terms of impurity levels and lithium concentration, meaning there is no ‘one-size-fits-all solution’. Consequently, each DLE solution must be tailored to the specific environmental and economic conditions of the project.

Unlocking New Sources: Oil-field Brines

DLE technology has the potential to unlock previously undeveloped sources of lithium, such as petro brines and geothermal deposits, by achieving recovery rates of 80-90% compared to the current evaporation yields of 20-50%. This is particularly significant for “unconventional” brine resources in western jurisdictions, aligning with the political priorities in the US and European Union to build localized and diversified streams of critical minerals.

DLE’s potential is attracting significant interest from major players, including oil and gas companies. For example, Standard Lithium’s Stage 1A project in Arkansas could be the first petro brine project to come online in 2026. It has an initial production of 5,000 tonnes per year.

Additionally, Exxon Mobil has signed a non-binding memorandum of understanding (MOU) with battery producer SK On for the supply of up to 100,000 tonnes from its DLE lithium project in Arkansas.

Despite the enthusiasm, DLE projects face significant capital and operating cost challenges. These projects have seen substantial cost increases as they advance and feasibility studies are updated.

Rising global inflation rates, along with higher equipment, utility, and labor costs, have driven these increases. For example, early-stage DLE projects have an average capital intensity of $37 per kilogram of lithium carbonate equivalent (LCE), while advanced projects average $60 per kilogram of LCE.

Given these challenges, Direct Lithium Extraction is unlikely to be a short-term solution for the lithium industry. Benchmark does not believe that DLE technology alone can bridge the structural deficits in the lithium market. However, it remains a promising avenue for expanding lithium supply in the long run.