Disseminated on behalf of Alaska Energy Metals Corporation

As the world accelerates its shift towards renewable energy, the role of electric vehicles (EVs) in reducing carbon emissions has become more critical. This transition depends heavily on advancements in battery technology, which is pivotal for mass EV adoption.

A key player in this evolution is nickel, an essential material in battery production that has gained increasing attention due to its impact on EV performance and range. This article delves into the demand-supply dynamics of nickel in the EV battery sector and its role in the broader energy transition as reported by the International Renewable Energy Agency (IRENA).

Nickel’s Essential Role in EV Batteries

EV batteries consist of several critical components, with nickel playing a significant role in cathode chemistry. Nickel-rich batteries, such as Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminum (NCA) chemistries, have become prevalent. These chemistries are favored due to their high energy density, which translates to longer driving ranges—a critical factor for widespread EV adoption.

As a result, nickel-rich batteries accounted for over half of the EV battery market in 2023, even as newer alternatives like Lithium Iron Phosphate (LFP) gained traction. Class I nickel, essential for EV batteries, accounts for only about 30% of total nickel production.

Nickel helps improve the energy density of batteries, allowing vehicles to travel further on a single charge. This advantage makes nickel-rich chemistries particularly valuable for larger vehicles like trucks and long-haul freight, where range and efficiency are crucial. As EV adoption spreads to these heavier vehicle segments, the demand for nickel-based batteries is expected to remain robust.

How EV Adoption is Shaping Nickel’s Demand

The rapid increase in EV adoption is directly linked to the rising demand for battery materials, including nickel. In 2023, global EV sales reached about 14 million units, representing 18% of total automobile sales.

By 2030, adhering to a 1.5°C scenario for climate goals would require sales reaching around 60 million units annually. This growth is expected to drive the demand for EV batteries to over 4,300 GWh per year, a significant increase from 2023 levels.

Nickel demand is closely tied to this trend, given the material’s crucial role in enhancing battery capacity.

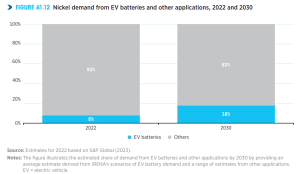

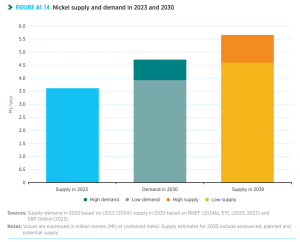

As of 2023, global nickel production reached 3.6 million tonnes, with Indonesia and the Philippines supplying nearly 60% of the world’s nickel. By 2030, demand for nickel in EV batteries is projected to rise to 18%, up from 8% in 2022, potentially reaching between 0.53 million and 1.09 million tonnes, depending on battery technology scenarios.

- The overall global nickel demand is expected to range from 3.9 to 4.7 million tonnes annually by 2030.

This expansion would see global nickel supply grow from 3.6 million metric tons (Mt) in 2023 to potentially 5.6 Mt per year by 2030. The ability of nickel production to keep pace with EV battery demand will be critical to avoiding supply bottlenecks that could hinder EV growth.

Beyond EVs, nickel’s importance extends to other applications like battery energy storage systems (BESS). As countries integrate more renewable energy sources into their grids, BESS becomes crucial for managing energy fluctuations and ensuring a stable supply.

The demand for BESS is expected to grow 6-fold between 2023 and 2030, complementing the growth in EV battery needs. While lithium remains the cornerstone of most battery chemistries, nickel’s contribution to BESS underscores its broadening role in energy storage solutions.

From Mine to Market: Navigating the Nickel Supply Chain

IRENA’s outlook for nickel supply is positive. However, challenges remain in ensuring that this supply materializes.

Despite this growing demand, the analysis indicates a lower risk of supply shortages compared to other critical materials, with a projected supply of 4.6 to 5.6 million tonnes by 2030.

However, while general nickel supplies seem adequate, concerns over high-purity Class I nickel for EV batteries persist.

Current projections suggest sufficient Class I nickel supply until 2028, but without expansion of production, shortages could arise by the end of the decade. Innovations in battery technology could significantly reduce reliance on nickel, potentially halving demand for EV batteries if alternatives gain traction.

Current projections show a potential increase in production, but this hinges on new mining projects and expansions coming online. The Asia-Pacific region, which currently dominates global battery production, is expected to see its share decrease slightly as Europe and North America ramp up capacity.

However, ensuring sufficient nickel supply will require substantial investment in mining operations and refining capacity across multiple regions.

The potential for supply-demand imbalances remains, as the range of estimates for nickel production varies significantly. For example, the difference between the highest and lowest projections represents about 60% of the current supply, highlighting the uncertainty in meeting future demand.

Market conditions, regulatory frameworks, and technological advancements will all play a role in determining how much of this projected supply will be realized by 2030.

The transition to electric vehicles is reshaping the global demand for battery materials, with nickel emerging as a critical component. Its role in enhancing battery energy density makes it indispensable for long-range EVs and larger vehicles like trucks. As global EV adoption surges, the demand for nickel is set to increase, requiring a corresponding expansion in supply to prevent shortages that could slow down the energy transition.

- READ MORE: The Ultimate Guide to Nickel