NVIDIA shares rebounded to $176.12 (+0.63%) on December 15, 2025, following a mix of product updates, demand signals from China, and revised outlooks from Wall Street analysts. The recovery followed weeks of market ups and downs. These were tied to worries about valuations, export limits, and uncertainty in the tech sector.

The latest movement reflects renewed confidence in NVIDIA’s position in artificial intelligence hardware and software. Investors reacted to the launch of a new software, Nemotron 3. They also noted early demand for the H200 data center chip. Plus, updated forecasts suggest ongoing growth in AI-driven computing.

NVIDIA’s recent updates highlight its role in shaping technology and infrastructure for modern AI. Short-term market swings may still happen, but the company stays focused on innovation.

Nemotron 3 Pushes NVIDIA Deeper Into AI Software

One key driver of the stock rebound was the launch of Nemotron 3. The product expands NVIDIA’s growing portfolio of AI software models designed for enterprise use. Nemotron 3 brings a new set of open-source AI models for agentic uses. These include:

- Nano: 30B total parameters, 3B active

- Super: about 100B

- Ultra: around 500B

The hybrid Mixture-of-Experts (MoE) architecture combines Mamba and Transformer elements. It offers up to 4x more token throughput than Nemotron 2 Nano. With a 1M-token context window, it generates 60% fewer reasoning tokens. This model excels in coding, math, long-context tasks, and multi-agent reasoning, all while lowering inference costs.

Jensen Huang, founder and CEO of NVIDIA, remarked:

“Open innovation is the foundation of AI progress. With Nemotron, we’re transforming advanced AI into an open platform that gives developers the transparency and efficiency they need to build agentic systems at scale.”

The launch reinforces NVIDIA’s shift from being seen only as a chipmaker to a full-stack AI company. Hardware remains central, but software now plays a larger role in driving long-term revenue. Analysts view this approach as a way to create more stable income streams beyond cyclical chip demand.

Nemotron 3 also supports NVIDIA’s ecosystem strategy. The chip company boosts customer reliance by tightly integrating AI models with its chips and platforms.

H200 Chip Demand Shows Strength Despite Constraints

Another factor supporting NVIDIA stock or shares was fresh discussion around demand for its H200 data center chip. The H200 is one of NVIDIA’s most advanced AI accelerators. It targets high-performance workloads such as large-scale AI training and inference.

Market signals suggest that demand remains strong, including interest from Chinese cloud and research clients. While U.S. export controls limit the types of chips NVIDIA can sell to China, modified versions of its products continue to find buyers.

Notably, President Trump greenlighted the H200 sales to “approved” Chinese customers. The U.S. will take a 25% revenue cut. This move reverses Biden-era restrictions after talks with Xi Jinping. However, Senate Democrats labeled it “dangerous” for national security.

The H200 builds on the success of the earlier H100 platform. It offers faster memory and better performance for large models. This matters as AI models grow in size and complexity.

Strong interest in the H200 indicates that global demand for AI infrastructure remains high. Data centers continue to invest heavily as AI adoption spreads across industries. This trend supports NVIDIA’s revenue outlook even as geopolitical risks remain.

Wall Street Forecasts Turn More Balanced

Wall Street analysts also played a role in the stock’s rebound. Several firms updated their forecasts after recent pullbacks in NVIDIA’s stock price. Some analysts were cautious about valuation. Others pointed out strong earnings visibility and market leadership.

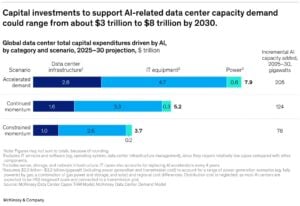

Updated forecasts reflect expectations that AI spending will remain a priority for large technology firms, governments, and enterprises. Per McKinsey & Company estimates, AI-related data center demand may reach up to $8 trillion by 2030. And NVIDIA continues to dominate the market for AI accelerators used in data centers.

Analysts also noted that revenue growth may normalize after years of rapid expansion. However, they still expect NVIDIA to grow faster than most semiconductor peers.

The more balanced tone from Wall Street helped stabilize investor sentiment. Rather than focusing only on risks, forecasts now reflect both strong fundamentals and realistic growth assumptions.

- MUST READ: Nvidia’s (NVDA) Stock Rose on Q3 Strong Results: $57B Revenue, $100B AI Infrastructure Plan

NVIDIA’s Role in the Global AI Buildout

NVIDIA sits at the center of the global AI infrastructure buildout. Its chips power many of the world’s largest AI models. Its software tools support developers, researchers, and enterprises.

As AI adoption grows, demand extends beyond tech companies. Industries such as healthcare, finance, energy, and manufacturing increasingly rely on AI for efficiency and decision-making.

This broad demand base helps reduce reliance on any single sector. It also supports longer-term growth even if consumer technology spending slows.

However, challenges remain. Competition is increasing, and governments are tightening rules on technology exports. Moreover, energy use in data centers is under scrutiny as it will send power demand skyrocketing. These pressures make sustainability and efficiency more important to NVIDIA’s strategy.

Efficiency and Sustainability Take Center Stage

NVIDIA has expanded its focus on sustainability as its technology footprint grows. Data centers powered by AI chips consume large amounts of energy. This creates both environmental and cost concerns.

The company aims to improve energy efficiency across its products. Newer GPUs deliver more performance per watt than earlier generations. This means customers can run larger workloads using less energy.

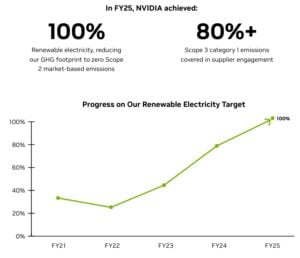

NVIDIA focuses on clean electricity. The company now uses 100% renewable energy for its offices and data centers. This shift helps cut Scope 1 and 2 emissions and lowers its carbon footprint.

The firm has set science-based targets aligned with limiting global warming to 1.5°C, including a 50% cut in Scope 1 and 2 emissions by FY 2030 (FY 2023 baseline). NVIDIA aims for a 75% cut in emissions intensity during customer use per petaflop of computing power by 2030. This focus targets most of its lifecycle emissions, mainly from end-user applications, not manufacturing.

NVIDIA also works with data center partners to improve cooling systems and power management. Better design reduces wasted energy and lowers emissions tied to electricity use.

The company also designs AI systems that support climate research. These systems help model weather patterns, climate risks, and energy systems. While indirect, such applications show how AI can support environmental goals.

Sustainability now plays a larger role in how investors evaluate technology firms. NVIDIA’s focus on efficiency and emissions aligns with this shift, even as demand for computing power continues to rise.

What NVIDIA’s Stock Recovery Tells Investors

NVIDIA’s stock rebound reflects a mix of short-term and long-term factors. The Nemotron 3 launch highlights software growth. H200 demand points to continued strength in AI infrastructure. Analyst updates suggest a more stable outlook after rapid gains earlier in the year.

At the same time, the company faces real constraints. Export rules, competition, and energy use remain key risks. Growth may slow compared to recent years, but the scale of AI adoption still supports expansion.

For investors, the latest developments suggest that NVIDIA remains a central player in AI. Market expectations may be more measured, but confidence in its long-term role remains intact.

As AI reshapes industries, NVIDIA’s mix of hardware, software, and sustainability efforts will continue to shape its position in global markets.