The real value of the voluntary carbon market is now around $2 billion, with rising price trends of ~170 types of carbon credits as per a recent Ecosystem Marketplace (EM) report.

EM, a Forest Trends initiative, has been tracking and reporting on the state of the VCM since 2006.

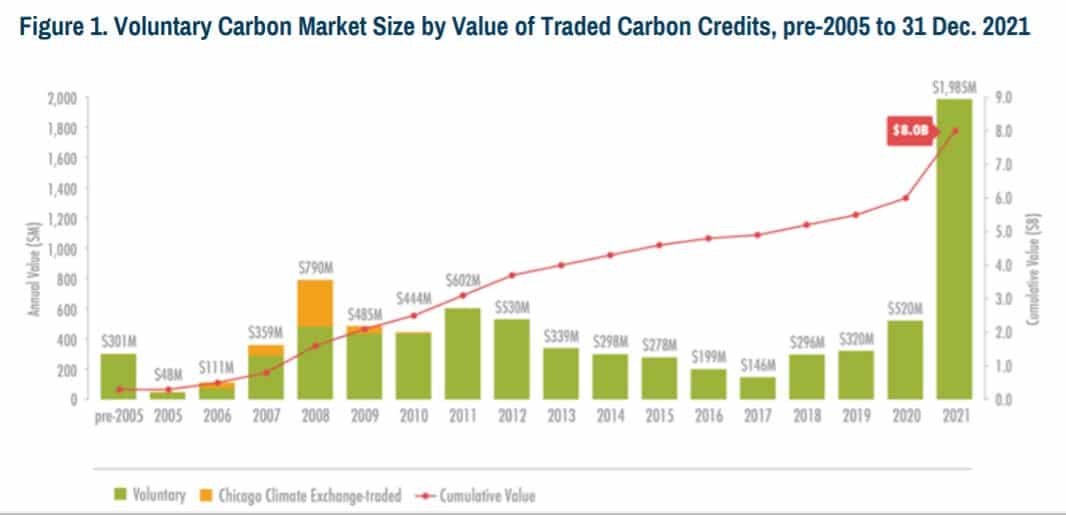

Their latest briefing reveals that the current VCM is almost $2 billion. And about 500 million carbon credits were traded in the same year, surpassing the previous EM report by 66%.

Also, global prices are climbing upwards by 60% more in 2021 ($4.0) than in 2020 ($2.5).

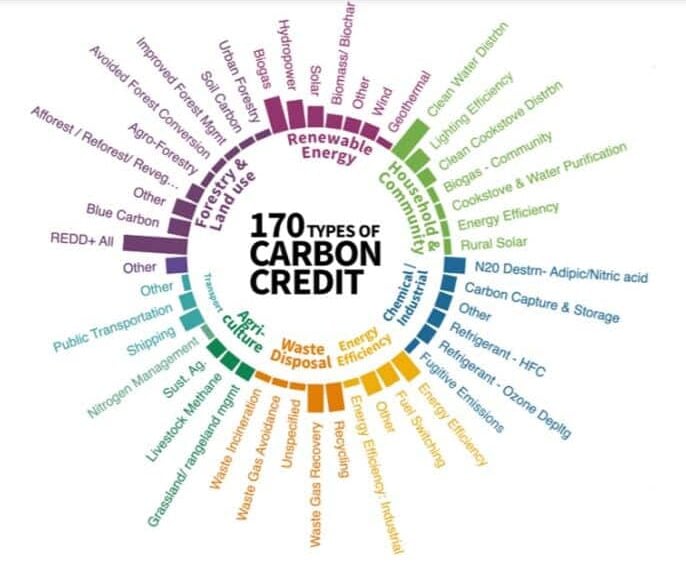

Lastly, EM stated that there are over 170 types of carbon credits falling under 8 categories traded in 2020-2021.

Global Voluntary Carbon Market Value and Prices

The future of voluntary carbon markets (VCM) looked brighter as more interests and investments poured into carbon projects. Plus, global climate and sustainability goals are driving record high demand.

The previous partial year report of EM indicated that VCM value is about $1 billion. But its recent and final brief stated that the real market value is nearly $2 billion.

The chart shows the VCM size by value of traded carbon credits from pre-2005 to year-ended 2021. The market’s total or cumulative value reaches $8 billion.

Likewise, global carbon credit prices are also trending upwards.

- The annual global average price per ton went up from $2.5 in 2020 to $4.0 in 2021. That represents about a 60% increase to a point never seen since 2013.

Among the eight categories of carbon credits, prices for projects with non-carbon benefits are higher.

Non-carbon benefits refer to the co-benefits that a certain project provides. Examples are local community support and biodiversity conservation.

Alongside sustainable development goals, the co-benefits are either integrated from the outset into carbon standards or bolted onto carbon credit projects with validated GHG emission reductions/removals.

In particular, projects under Gold Standard (one of the major carbon standards) saw a 35% increase in price from 2020 ($3.7) to 2021 ($5.0).

Plan Vivo also recorded a higher price increase of 15% for the same period. The bulk of its transaction volume, 79%, was from projects under the category of Forestry and Land Use (Afforestation, Reforestation, and Revegetation or ARR).

The most common co-benefits certification standard in use today is the CCB (Climate, Community, & Biodiversity) Standards. It’s an add-on for Verified Carbon Standard (VCS) carbon credits that also jumped in volume by 277%.

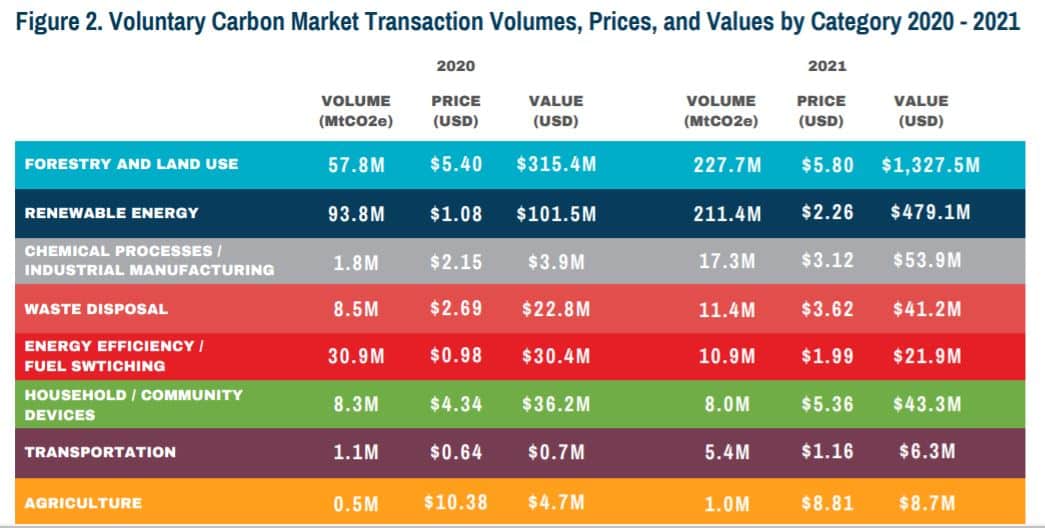

The table below shows the overall VCM transaction volumes, prices, and values by category, comparing 2020 and 2021 results.

Types and Categories of Project-Specific Carbon Credits

As the VCM matures, more and more participants – project developers, investors, buyers, regulators, etc. – are shaping how the market works. They give different attributes and definitions to project-specific carbon credits.

As such, EM tried to simplify things by giving an official Project ID for traded carbon credits data. This is important so that those attributes would be verifiable through the carbon standard that issues the credits.

The Forest Trends initiative also updated its Carbon Offset Project Typology in Q1 of 2022. These updates allowed EM to expand its list of project types, covering 170+ projects.

- All project types are then rolled up into 60 project clusters and narrowed down even further into 8 project categories.

The image illustrates EM’s 8 categories with specific examples of projects.

Another remarkable result reported by EM is that project specificity in trade reporting goes with higher voluntary carbon market value and prices.

It means carbon credits that were cross-referenced with carbon standards’ registries have higher prices than those that were not. Cross-referencing involves providing project-specific metrics for the credits like project name or ID.

Most interestingly, the report suggested that the VCM prefers to buy and sell carbon credits via bilateral deals between project developers and end buyers the most .

That only shows that there are growing opportunities for project developers to respond to corporate requests for proposals.

But in the past years, intermediaries and digital spot trading exchanges began to re-emerge into the VCM.

Futures exchanges (e.g. CME Group) are working with spot exchanges (e.g. CTX and ACX) to develop standardized contracts pegged to specific project attributes.

As more players and money are flooding the voluntary carbon market, its value seems to grow even more.