Ernst & Young (EY) Net Zero Centre analysis revealed that achieving net zero emissions means carbon credits volume will grow by 40x and price be at $150 per ton by 2035.

The pressures to decarbonize are mounting. Over a hundred countries committed to the Paris Agreement and set ambitious climate goals.

Also, the number of organizations and businesses disclosing net zero pledges tripled in 2021. What’s more, investors and consumers are favoring climate action with their money.

All signs are pointing in one direction. Yet, meeting the world’s net zero pledges can be challenging and costly for businesses.

But entities have to find essential and cost-effective emissions reduction and carbon credits can provide that.

As for the EY Net Zero Centre, 50-80% of decarbonization costs in line with the Paris Agreement can be achieved through carbon credit offsets.

Why Carbon Credits Volume Will Balloon by 30x to 40x

The EY’s report provided the outlook for carbon credits and offsets volume between now and 2050. The analysis aims to help companies make clear pathways to net zero emissions by 2050 and manage the uncertainties involved.

Carbon credits are an essential part of the business toolbox. They support earlier and more ambitious net zero commitments of companies.

But hitting net zero emissions can take time and may involve uncertainties. Still, by using carbon credit offsets to reduce emissions, businesses can be profitable in the short run while they’re moving towards net zero in the long run.

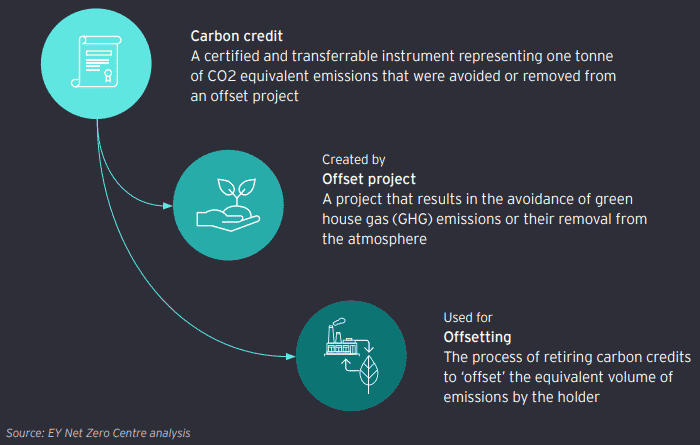

Here’s how emissions offsetting works using carbon credits:

- Carbon credits volume is expected to balloon by 30x to 40x their current levels if the world is to meet the Paris climate goals.

That’s because competition for carbon credits will heat up, emissions reductions will scale up, and regulations will ramp up.

While it’s certain that the voluntary carbon market poses to explode, how the market develops remains uncertain.

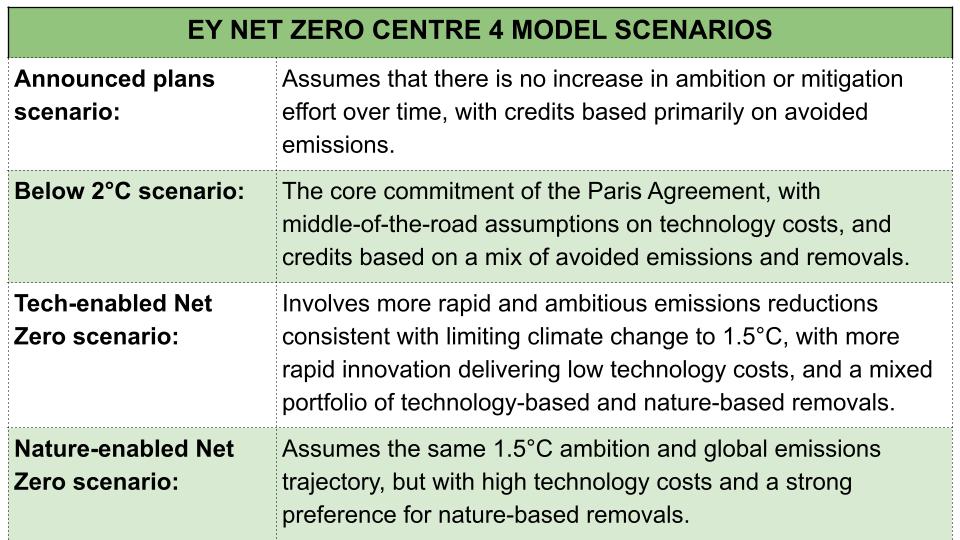

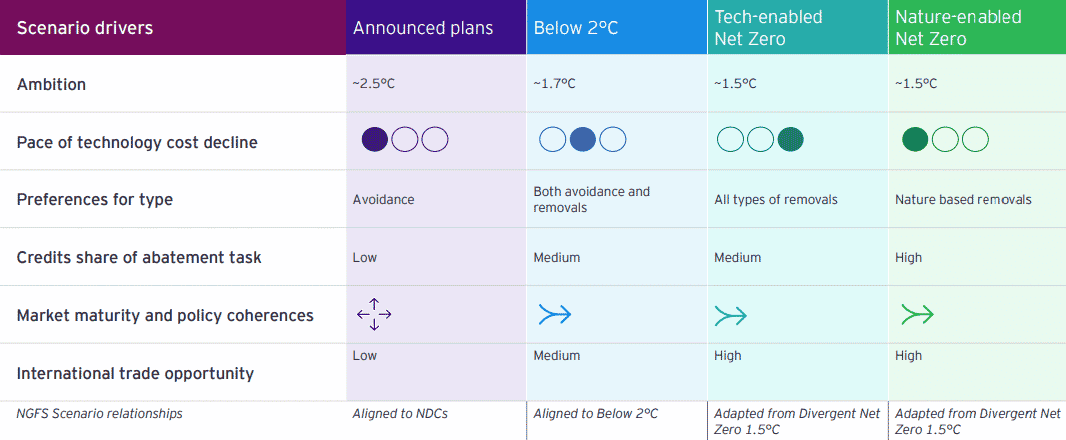

So, to explore the possible carbon credit market role and outlook, the EY Net Zero Centre developed four future scenario models.

The four scenarios consider different combinations of climate, technology, and institutional drivers which are:

Across all four outlooks, the analysis reveals these major findings:

- rising demand,

- a race to quality, and

- higher unit supply costs will make high-quality carbon credits scarce and expensive.

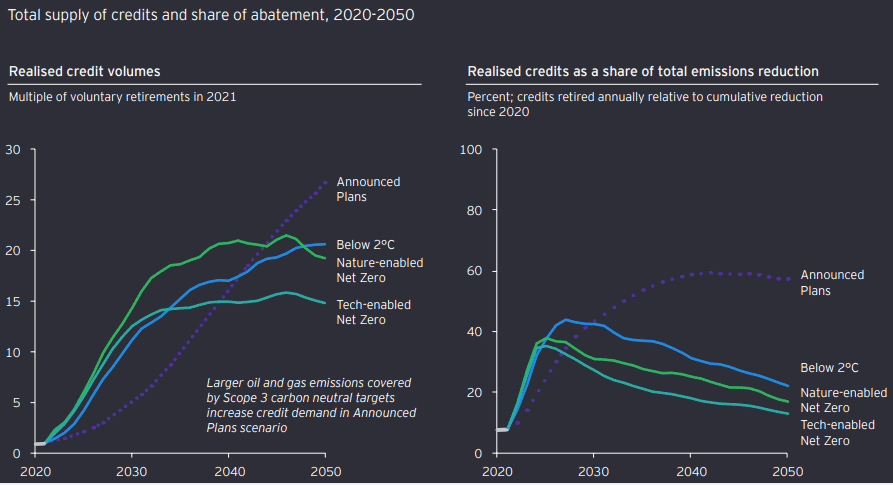

Carbon credit volume will increase to 30-40x current supply by 2035

Rising demand makes the volume and price of carbon credits grow rapidly to 2035. After that, the volume of credits grows more slowly across all the four outlooks analyzed.

The projections for carbon credit supply volumes are shown for four scenarios in the chart below.

The left chart plots the increase in credit volumes needed to meet the emissions reduction commitments by 2050. While the right one shows the share of total reductions met using carbon credits (includes both avoidance-based and removals-based credits).

The volumes rise rapidly in Paris-consistent scenarios. And that’s despite credits having a decreasing share of emissions reductions.

The projections assume that 100% of carbon offsets and credits are high integrity across all scenarios. Also, all credits have additional permanent reductions in emissions.

In other words, there’s no greenwashing. Greenwashing is conveying a false or a misleading claim to make the public believe that a company is reducing its emissions even if it’s not.

Rising demand, race to quality, and climbing unit supply costs = carbon credits become scarce and expensive across all four outlooks

EY’s analysis finds that scaling up carbon credit volumes will deplete available low-cost supply fast. As a result, there’ll be rapid increases in credit prices to 2035 across all four model scenarios.

In a typical market, growing demand for a good/service will not result in higher prices over the long term if supply is elastic.

But the case for the supply of high-quality carbon credits is different. It’s subject to some constraints such as:

- geopolitics of climate commitments (ex. the notion of common but differentiated responsibilities)

- the increasing importance of more costly removals-based credits.

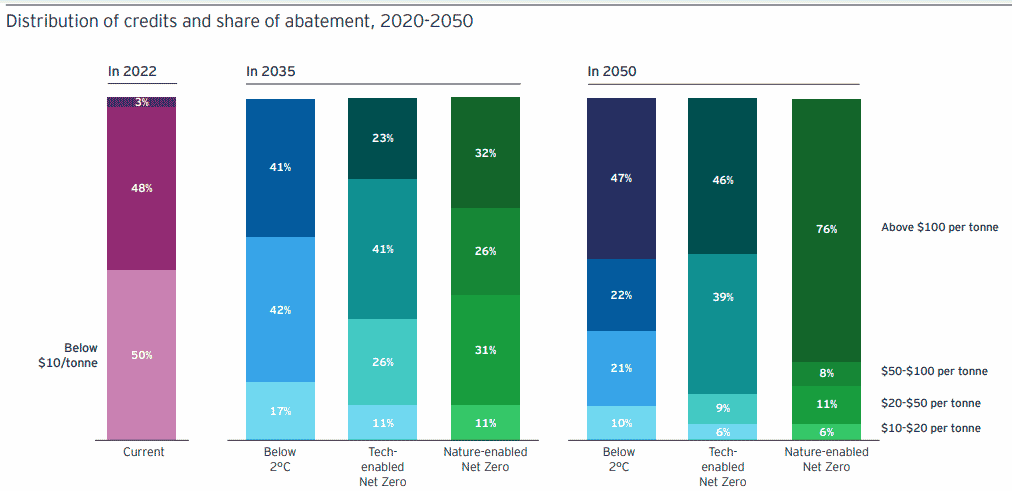

Average costs of high-quality carbon credits supply will rise as volume increases.

About 40-60% of credits will cost over US$50 per tonne by 2035 as the figure shows.

The price increases will continue after 2035 in most scenarios. This is due to an incremental increase in emissions reductions among businesses.

This scenario will boost competition for avoidance-based credits and raise the need for removals-based credits.

But price increases for the Tech-enabled scenario will moderate after 2030 or 2035. This reflects the common assumption for faster and bigger reductions in technology costs.

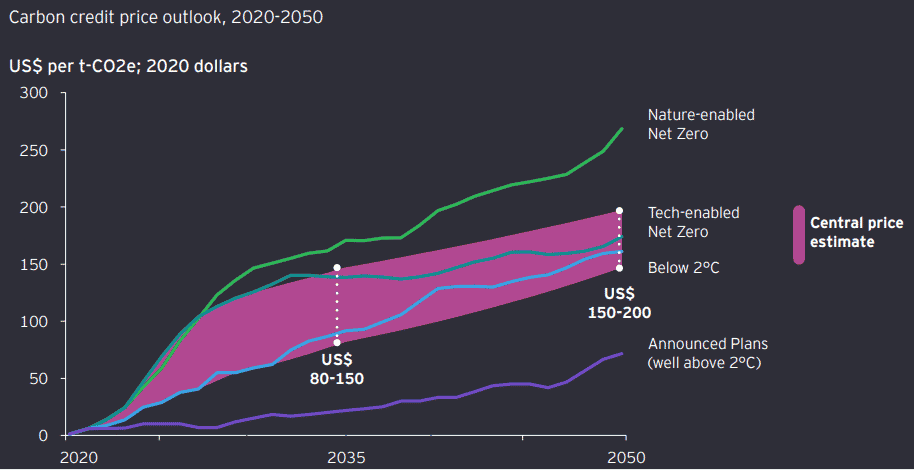

Credit Prices Will Rise to US$80-150/Ton by 2035

EY Net Zero Centre’s central estimate deems that countries and companies move quickly to execute actions and policies that are consistent with the Paris accord.

The projection further assumes that costs of abatement and supply of credits will be in the middle or lower end of the range explored.

The graph below reveals the results of these price assumptions.

The analysis suggests credit prices can rise from under $25/tCO2e today to $80-150/tCO2e in 2035. And they’ll continue to rise to $150-$200/tCOe in 2050 (in real 2020 dollars).

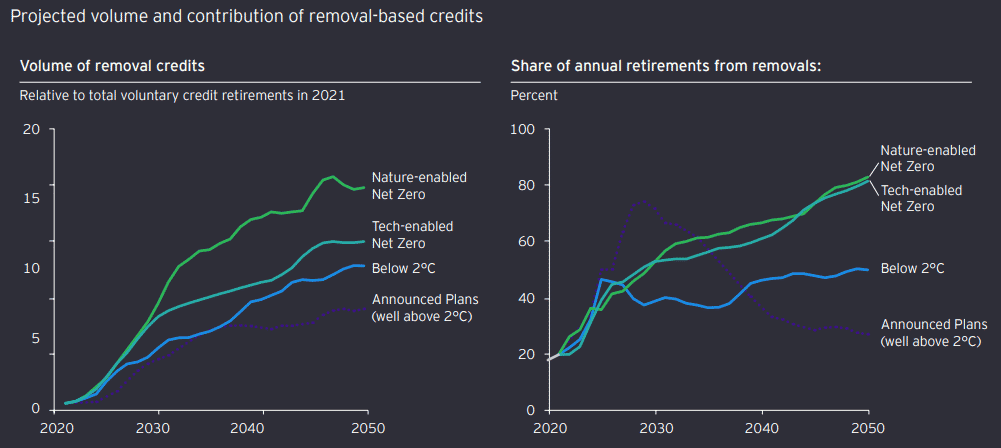

Another key analysis by EY is that tightening emissions budgets will affect the mix of carbon credits demanded and how they are used.

Tighter Emissions Budgets Drive Removals-based Credits Up

Changes in technology costs and policy context will shift baselines for carbon credit offset projects. These will make it harder to create credits based on avoided emissions while sboosting the role of removals-based credits.

And so, removal credits become essential in net zero scenarios.

This forecast is very crucial to note as avoidance-based credits dominate the current global use and volume of carbon credits. They account for ~80% of all credits issued and ~90% of all credits used (or retired) in 2020 across the largest voluntary registries.

Thus, technologies that remove carbon from the air will be a vital part of reducing emissions to limit the harsh effects of climate change.

Moreover, stricter government regulations will drive several changes in carbon credit markets.

- However, this is unlikely to prevent strong growth in the demand for carbon credits as net zero emissions targets still need offsets.

What’s more significant is that tightening regulation will blur the distinction between voluntary and compliance markets for carbon credits.

This will increase the need for companies to use the supply of high-quality carbon credits, especially beyond 2035.

Lastly, market fundamentals will drive the emergence of large and efficient carbon exchanges. This will enable the trading of a high volume of carbon credits through top carbon exchanges linked to various carbon registries.

All these market trends amplify the risks and opportunities created by the need to reach climate goals. For business leaders, this means the need to engage and act urgently.

And every leader needs to have a clear net zero strategy embracing the role of carbon credit to create new value in a rapidly changing industry.