Disseminated on behalf of Li-FT Power Ltd

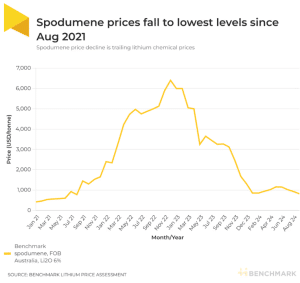

Spodumene prices, a key raw material for lithium production, have hit their lowest levels since August 2021, driven by a significant slump in lithium chemical prices. With major producers feeling the heat, the lithium market faces turbulence.

As of September 4, spodumene FOB (Free on Board) Australia prices fell 14.4% this year, reaching $818 per tonne, according to the Benchmark Lithium Price Assessment. This represents a massive drop from their December 2022 peak of $6,401 per tonne—a fall to just one-eighth of their highest value.

The decline is largely attributed to the falling prices of lithium chemicals, which spodumene prices tend to follow closely.

In addition to this lithium price drop, there’s another factor at play: high inventory levels. Spodumene suppliers and producers in China continue to flood the market to maintain their share, even as prices fall.

A New Competitor Emerges in the Lithium Race

Spodumene isn’t the only game in town anymore. Prices for lepidolite, another lithium-bearing mineral, have also dropped sharply, particularly in China.

In August, lepidolite prices fell significantly, making it a more attractive option for lithium producers. This shift has further reduced demand for spodumene, accelerating its price decline.

In fact, during the two-week assessment period ending on September 4, spodumene prices saw a 3.3% decline. The growing interest in lepidolite as a feedstock, combined with existing inventory surpluses, continues to create a bearish outlook for spodumene producers.

Benchmark’s data also revealed sharp declines in the spot prices of lithium carbonate and lithium hydroxide in China. Lithium carbonate prices have fallen 23.8% this year, while lithium hydroxide prices have dropped 15%. These declines in lithium chemicals mirror the challenges faced by spodumene producers and reflect broader market dynamics.

A MESSAGE FROM Li-FT POWER LTD.

This content was reviewed and approved by Li-FT Power Ltd. and is being disseminated on behalf of CarbonCredits.com.

Lithium Deposits That Can Be Seen From The Sky

Why Li-FT Power? One of the fastest developing North American lithium juniors is Li-FT Power Ltd (TXSV: LIFT | OTCQX: LIFFF | FRA: WS0) with a flagship Yellowknife Lithium project located in the Northwest Territories. Three reasons to consider Li-FT Power:

RESOURCE POTENTIAL | EXPEDITED STRATEGY | INFRASTRUCTURE

Producers on the Ropes: The Pain of Falling Prices

The current lithium price environment is particularly challenging for spodumene producers, especially those with higher production costs. As prices approach the $800 per tonne mark, many higher-cost producers are finding it increasingly difficult to maintain profitability. Some are being forced to make tough decisions, such as cutting production or delaying expansion projects.

Adam Megginson, a senior analyst at Benchmark, explained:

“As we have approached the $800 a tonne mark, we have started to hear lower bids, but they have not closed. So, we’re beginning to see resistance at these levels.”

Producers face a dilemma: announcing production cuts could signal to the market that they are struggling to keep up with the price environment. At the same time, many lithium producers want to keep operating to be ready to capture market share once prices rise again. This means that some upstream players continue to produce even when prices fall below their operational costs.

For instance, Arcadium Lithium recently announced that it plans to place its Mt Cattlin mine into care and maintenance by 2025 due to the low-price environment.

However, Greenbushes, a major spodumene producer, appears to be weathering the storm. Its expansion, expected to ramp up to 60,000 tonnes per year of lithium carbonate equivalent (LCE), is still on track to go online next year.

In contrast, projects in Africa, which are mostly owned by Chinese companies, have continued without pause, driven by vertical integration within the Chinese market.

More Clouds Before the Storm Clears

Sophia Jang, Benchmark’s analyst, noted that any price increases this year are unlikely to be significant. However, she did suggest that there could be a short-term spike in prices in late September as Chinese cathode producers look to secure materials ahead of China’s National Day Golden Week on October 1.

Looking further ahead, the fourth quarter typically sees higher demand for electric vehicles, which could help stabilize demand for lithium. However, it remains uncertain whether this will be enough to drive a meaningful recovery in spodumene prices.

- Lithium Company Spotlight: The Fastest Developing North American Lithium Junior

The Long Game: $1.6 Trillion Needed to Meet Future Demand

While the lithium market is experiencing short-term turbulence, the long-term outlook remains bullish.

Benchmark’s Lithium-ion Battery Database forecasts that at least $1.6 trillion in investment will be needed to meet battery demand by 2040. This is almost triple the $571 billion requirement to meet demand by 2030.

Battery demand could grow significantly in the coming years, from 937 gigawatt-hours (GWh) in 2023 to 3.7 terawatt-hours (TWh) in 2030. This demand will double again between 2030 and 2040, highlighting the immense need for new investment in lithium production, processing, and battery manufacturing.

- A significant portion of this investment—44%—will go towards building gigafactories, which will produce battery cells and assemble battery packs.

Recycling will also play a major role in meeting future lithium demand. As more EVs reach the end of their useful life, the battery scrap pool is set to grow substantially. According to Benchmark, $26 billion will be needed by 2030 to build the capacity to recycle this scrap into usable battery materials. By 2040, this figure will rise to $157 billion.

Lithium Takes the Lead

Among critical raw materials, lithium will require the largest investment to meet future demand. By 2030, $94 billion is needed to scale lithium production, with this figure doubling by 2040.

While the current lithium market may be facing challenges, the long-term trajectory remains positive. This is primarily driven by the growth of electric vehicles and renewable energy storage. Spodumene producers may be navigating rough waters now, but those that can weather the storm are likely to benefit from future demand growth.