Following serious discussions and decisions on carbon markets at the COP29 summit, Verra and the state of Amazonas, Brazil, signed an agreement to enhance regional carbon markets on November 13. This Memorandum of Understanding (MOU) was announced during COP29 in Baku, Azerbaijan.

The collaboration aims to strengthen carbon market frameworks, improve regulations, and foster sustainable development in Amazonas.

Eduardo Taveira, Amazonas’ Secretary of State for the Environment and represents Governor Wilson Lima at COP29 in Baku, said,

“Verra is the largest carbon credit certifier in the world. This partnership represents a significant advance in the sustainability trajectory of Amazonas, as it will provide all the necessary support for the State to be a generator of high-integrity credits, following strict environmental criteria, with a guarantee of high environmental, social and low carbon economy impact that we seek.”

Verra: Pioneering Transparent Environmental Solutions

In the past, Verra had addressed global environmental and social challenges by supporting climate action. They have offered transparent standards and tools to assess impacts, reduce emissions, improve livelihoods, and protect natural resources. Notably, they enable funding for verified, scalable projects that have long-lasting environmental benefits.

Source: Verra

Leveraging Amazonas’ Natural Strengths

The press release mentions that Amazonas is uniquely positioned to develop carbon market projects with 92% of its land covered by rainforest. Verra’s methodologies, including the Reducing Emissions from Deforestation and Forest Degradation (REDD) framework, offer tools to protect these forests. Such projects can help reduce emissions, conserve biodiversity, and support local communities.

So, what’s Verra’s role here exactly? Well, Verra a global leader in setting standards for climate action and sustainable development, will work with Amazonas to enhance the state’s capacity and provide technical expertise. The partnership focuses on creating high-integrity carbon credits while adhering to strict environmental and social criteria.

Mandy Rambharos, Verra CEO expressed herself by noting,

“We are honored that the state of Amazonas selected Verra as a partner in strengthening regional carbon markets. These markets hold the key to unlocking the climate finance needed to reduce emissions, save forests, retain biodiversity, and support local communities. We look forward to collaborating closely with the state of Amazonas, who has undertaken critical work in advancing nature-based climate solutions in its jurisdiction.”

- MUST READ: Article 6.2 at COP29: Singapore Partners with Gold Standard and Verra to Advance Climate Action

Key Focus Areas in Verra-Amazonas MOU

Let’s discover the key areas of collaboration that are covered in the MOU.

Capacity Building

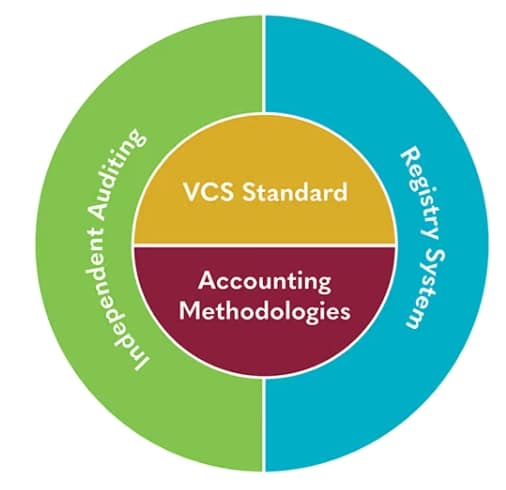

Verra will offer specialized training to Amazonas on carbon markets. The training will cover the Verified Carbon Standard (VCS) Program, Climate, Community & Biodiversity Standards (CCBS), and the Sustainable Development Verified Impact Standard (SD VISta). Additionally, the Verra Registry, which tracks carbon credits, will also be part of the training.

Essential components of Verra’s VCS Program

Source: Verra

Information Exchange

Both will exchange public data to develop robust carbon market frameworks. Further Verra will provide information from its Registry and share insights about its new REDD methodology and modules. Jointly, both parties will explore how Amazonas can apply these methodologies to potential projects.

Strengthening Regulation

Verra will help Amazonas develop and refine significant carbon market regulations. These efforts will include public discussions to ensure transparency and community participation. In the past, Verra has followed a similar process with other countries to meet their sustainability goals. Subsequently, this vast experience working with governments in different regions will guide Amazonas’ regulatory framework.

A Partnership Innovating Climate Finance

This partnership can potentially make Amazonas a leader in sustainable carbon markets. By leveraging Verra’s expertise, the state can do a lot to attract climate finance. For example, it can boost its fund conservation efforts, create more economic opportunities, and strengthen its low-carbon economy.

The collaboration also addresses the global need for effective climate solutions. Amazonas’ commitment to protecting its rainforest and Verra’s innovative methodologies make this partnership a model for other regions. As the state gears up to develop high-integrity carbon credits it can contribute significantly to global efforts to combat climate change.

We have already read at COP29 leaders have agreed on having robust international carbon market standards. And this initiative is just a testament to that even though it reinforces the role of regional carbon markets. All in all, Verra and Amazonas will set a remarkable example of sustainable development by tackling environmental challenges while fostering economic growth.

Source: Verra and State of Amazonas to Collaborate on Strengthening State’s Carbon Markets – Verra

Source: IAEA

Source: IAEA