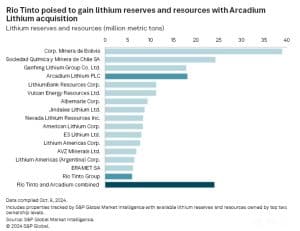

In a major strategic move, Rio Tinto has agreed to acquire U.S.-based Arcadium Lithium for $6.7 billion, marking a significant step in transforming it into a global leader in the lithium market. The all-cash deal, offering a 90% premium to Arcadium’s share price, positions Rio Tinto as the world’s third-largest producer of lithium which is a critical component in electric vehicle (EV) batteries and energy storage solutions.

Significantly, this acquisition, announced on October 9, underscores Rio Tinto’s commitment to the energy transition by expanding its footprint in low-carbon, high-demand raw materials.

A MESSAGE FROM Li-FT POWER LTD.

Lithium Deposits That Can Be Seen From The Sky

Who is Li-FT Power? They are one of the fastest developing North American lithium juniors with a flagship Yellowknife Lithium project located in the Northwest Territories.

Three reasons to consider Li-FT Power:

RESOURCE POTENTIAL | EXPEDITED STRATEGY | INFRASTRUCTURE

Li-FT is advancing five key projects; all located in the extremely safe and friendly mining jurisdiction of Canada.

TXSV: LIFT | OTCQX: LIFFF | FRA: WS0

*** This content was reviewed and approved by Li-FT Power Ltd. and is being disseminated on behalf of Li-FT Power Ltd. by CarbonCredits.com. ***

Why Rio Tinto’s Moment for Lithium is Now?

Lithium prices have recently dipped due to oversupply and slowed EV sales in China, but Rio Tinto’s CEO Jakob Stausholm remains confident about lithium’s long-term trend. The company expects lithium demand to grow by over 10% annually through 2040, driven by the global push toward electrification.

Jakob Stausholm, CEO of Rio Tinto CEO explained,

“Acquiring Arcadium Lithium is a significant step forward in Rio Tinto’s long-term strategy, creating a world-class lithium business alongside our leading aluminum and copper operations to supply materials needed for the energy transition. Arcadium Lithium is an outstanding business today and we will bring our scale, development capabilities, and financial strength to realize the full potential of its Tier 1 portfolio. This is a counter-cyclical expansion aligned with our disciplined capital allocation framework, increasing our exposure to a high-growth, attractive market at the right point in the cycle.”

The mining giant has been facing challenges in the lithium market, notably with its Jadar project in Serbia, which has encountered local opposition and regulatory delays. Thus, the acquisition of Arcadium is an instant boost to Rio Tinto’s lithium production capacity, giving the company access to resources that are already operational or nearing completion.

This acquisition not only strengthens Rio Tinto’s position in the rapidly growing EV market but also provides access to major automakers like Tesla, BMW, and General Motors.

Arcadium’s Role in Expanding Rio Tinto’s Lithium Capacity

Arcadium Lithium has quickly become a global leader in sustainable lithium production. It has operating resources in Argentina and Australia and downstream conversion assets in the U.S., China, Japan, and the U.K. Notably, In the U.S. the company has an exclusive integrated mine-to-metal production facility in the Western Hemisphere for high-purity lithium metal.

The company leads the industry in lithium extraction, excelling in hard-rock mining, brine extraction, and direct lithium extraction (DLE). It also specializes in manufacturing lithium chemicals for high-performance applications.

Arcadium Lithium’s CEO Paul Graves expressed his sentiment,

“We are confident that this is a compelling cash offer that reflects a full and fair long-term value for our business and de-risks our shareholders’ exposure to the execution of our development portfolio and market volatility. This agreement with Rio Tinto demonstrates the value in what we have built over many years at Arcadium Lithium and its predecessor companies, and we are excited that this transaction will give us the opportunity to accelerate and expand our strategy, for the benefit of our customers, our employees, and the communities in which we operate.”

Harnessing Quebec’s Hydropower

Furthermore, Arcadium’s operations, particularly in Quebec, are well-aligned with Rio Tinto’s focus on low-carbon solutions. Both companies utilize Quebec’s hydropower resources, which are critical for sustainable lithium production. This would help Rio produce lithium with a lower carbon footprint, thereby showcasing its sustainable mining practices.

With Arcadium’s plans to have 2X production capacity by 2028, Rio Tinto is poised to play a major role in the global supply of lithium in the future. As demand for clean energy materials continues to rise, the company’s ability to supply high-quality, sustainably produced lithium will be a key factor in its success.

Strategic and Financial Win: A Summary

Rio Tinto’s acquisition of Arcadium will leverage its scale, development skills, and financial strength to maximize Arcadium’s portfolio. The press release has summarized it somewhat this way:

Complementary Strengths

Rio Tinto’s financial strength and proven project management will help speed up the development of Arcadium’s top assets. Both companies have a strong presence in Argentina and Quebec, where Rio Tinto plans to create world-class lithium hubs.

On the other hand, Arcadium’s Tier 1 assets have consistently delivered high profits. With these resources, the company expects to increase its capacity by 130% by 2028. They envision to control the largest lithium resource base in the world in the future.

Solid Financial Gains

Closing the Deal

The acquisition is expected to close by mid-2025 and is pending for regulatory approvals and shareholders’ consent. Both companies’ boards have unanimously approved the deal, and early indications suggest a smooth path to completion.

Once the deal closes, Rio Tinto plans to integrate Arcadium’s operations with its existing lithium assets. Subsequently it would create a new business unit focused on lithium production and processing. The company has also expressed its commitment to retaining Arcadium’s workforce with the new beginning.

Jakob Stausholm assured further saying,

“We look forward to building on Arcadium Lithium’s contributions to the countries and communities where it operates, drawing on the strong presence we already have in these regions. Our team has deep conviction in the long-term value that combining our offerings will deliver to all stakeholders.”

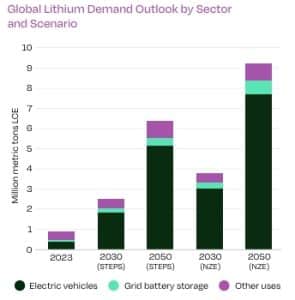

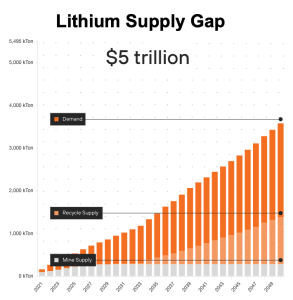

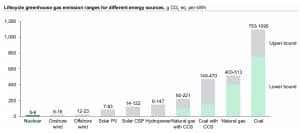

Projections from the International Energy Agency (IEA) indicate that lithium demand will significantly increase, with the EVs and grid battery storage sectors—currently responsible for about 60% of total demand. This is expected to rise to approximately 90% by 2050 under both the Stated Policies (STEPS) and Net Zero Emissions (NZE) scenarios.

Source: Procured from Arcadium’s sustainability report, originally from IEA.

Thus, we hope by the time the market rebounds, Rio Tinto will be well-positioned to meet soaring demand with an expanded and diversified lithium portfolio.

Source: IEA

Source: IEA