A massive new green hydrogen project was announced by the Indian Government. India’s National Green Hydrogen Mission is another decarbonization strategy to become energy-independent by 2047 and achieve net zero by 2070.

The mission was approved by the Union Cabinet on 4th January 2023, with a budget allocation of ₹ 19,744 crore. The ultimate objective of the Mission is to make India the Global Hub for the production, usage, and export of Green Hydrogen and its derivatives.

Before moving on to the current scenario of monetary investments and the use of green hydrogen in transport pilot projects, we will examine what this comprehensive plan looks like for the coming years.

India’s Plan to Take a Quantum Leap in the Green Hydrogen Race

To become the world’s largest producer and exporter of green hydrogen in the world, India has set forth a series of milestones. As per data from Govt. of India’s Ministry of New and Renewable Energy they include:

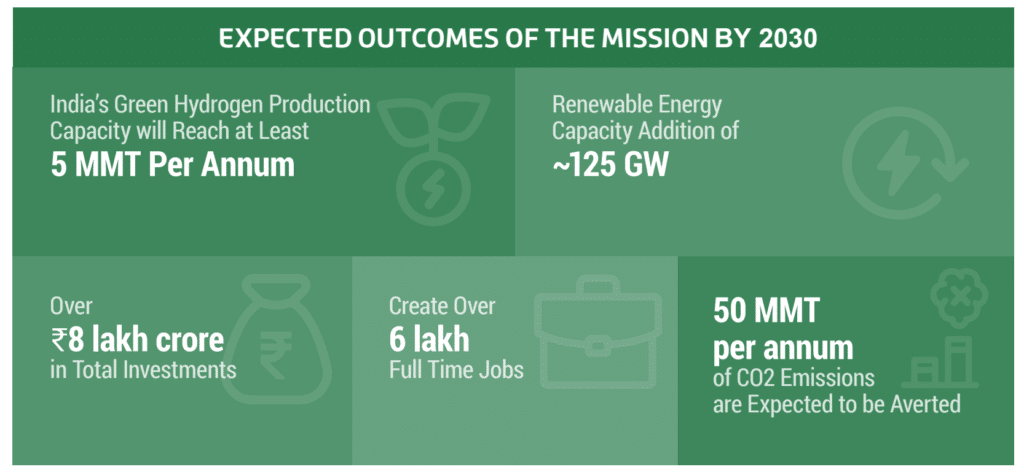

- The Mission aims to establish capacities to produce at least 5 Million Metric Tonne (MMT) of Green Hydrogen annually by 2030, with the potential to reach 10 MMT per annum through expansion of export markets and international partnerships.

- The initial budget for the mission will be Rs 19,744 crore. From this Rs 17,490 crore will be allocated for the SIGHT program, Rs 1,466 crore for pilot projects, Rs 400 crore for R&D, and Rs 388 crore for other mission components.

- Kick-off global demand to nearly 100 million metric tonnes (MMT) for Green Hydrogen and its derivatives, like green ammonia by 2030. The target is to capture 10% of the global market with an annual export demand of about 10 MMT of Green Hydrogen/Green Ammonia.

- The decarbonization target is to mitigate 50 MMT per annum of CO2 emissions with the implementation of the Green Hydrogen initiatives charted under the Mission.

- Replace fossil fuel with green hydrogen and its derivates to reduce f ₹1 lakh crore in fossil fuel imports by the year 2030 and enhance India’s energy security.

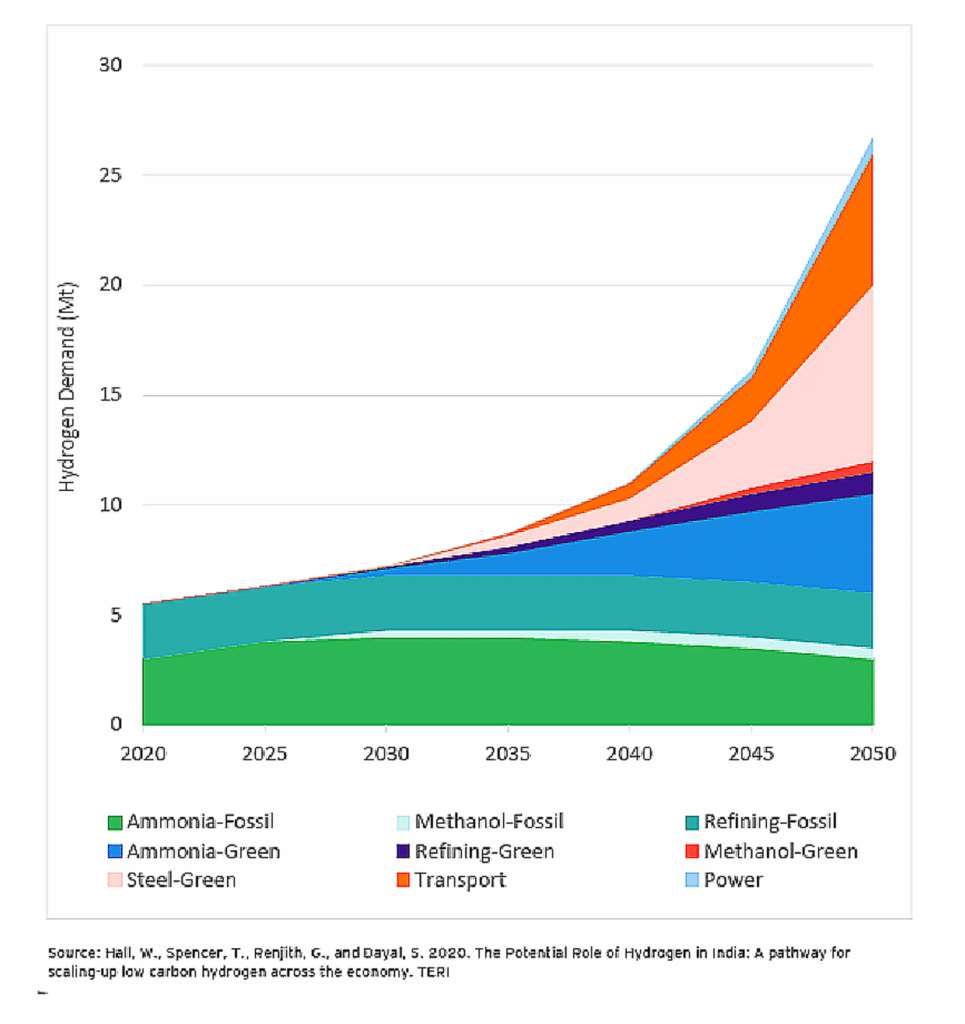

An examination of the industrial sectors that would drive demand for green hydrogen in the future are shown in the growth graph below.

Revving Up Sustainability: Transport Sector Emerges as the Prime Hub for the Green Hydrogen Revolution

Revving Up Sustainability: Transport Sector Emerges as the Prime Hub for the Green Hydrogen Revolution

The Ministry of New & Renewable Energy (MNRE) recently released guidelines for a program aimed at backing pilot projects centered on utilizing green hydrogen as a fuel for four-wheelers, buses, long-haul trucks, and heavy-duty vehicles. The technology uses fuel cell-based and internal combustion engine-based propulsion techniques.

The iron and steel sector and the shipping sector would be bolstered under the Green Hydrogen Mission to undertake the pilot projects. The important features of this project are:

- Pilot Projects through the Ministry of Ports, Shipping and Waterways (MoPSW) to drive green hydrogen innovation with Rs. 115 Crore Budget by 2025-26.

- Inaugurating green hydrogen in maritime for use in piloting maritime propulsion, passenger ferries, boats and cruising, and refueling of ships. Testing technical feasibility, economic viability, and effectiveness in real-world operations.

- The Ministry of Steel and designated Implementing Agencies will oversee pilot projects in the Steel and Iron Sector, aiming to substitute fossil fuels and feedstock with green hydrogen and its derivatives.

- The program will also fund projects exploring innovative hydrogen applications to cut carbon emissions during the iron and steel manufacturing process.

As stated by the MNRE, the initiative will be executed with a total budget allocation of Rs 496 crore until the fiscal year 2025-26. Such a huge budget means primary focus on pilot projects in the transport sector and building hi-tech infrastructure to manufacture green hydrogen and installing hydrogen refueling stations wherever required.

India’s Strategic Edge: Powering the Global Energy Shift with Distinct Advantages

Currently, China is the largest producer and consumer of green hydrogen followed by the US. But India’s ambitious green hydrogen goals would certainly make it a strong player in the race for more production.

More insight into the distinct advantages India has over other hydrogen superpowers give weight to these goals:

- That the government foresees a substantial decrease in the costs of renewable energy and electrolyzers paves the way for highly cost-effective use of green hydrogen in passenger and commercial vehicles in the coming years

This could enable India to achieve the world’s lowest green hydrogen production costs, potentially hitting USD 0.75 per kilogram by 2050. This further adds an edge to India’s green hydrogen export market.

India holds rich and vast sources of renewable energy with global giants like Reliance Industries (RIL), GAIL India Ltd., Adani Group, NTPC (National Thermal Power Corporation Limited), Indian Oil Corporation (Indian Oil), and Larsen and Toubro (L&T) owning most if not nearly all of the assets and resources to firmly lead the green hydrogen revolution.

Green Hydrogen is likely to play a critical role in India’s energy transition. Moreover, shifting to green hydrogen aligns India with global climate leaders such as the US and EU. India’s 2030 pledge under the terms of the Paris Agreement to reduce greenhouse gas emissions will eventually empower the country to make it a global hub for production, usage and export of Green Hydrogen and its derivatives.

To Read More About India’s National Green Hydrogen Mission Click Here

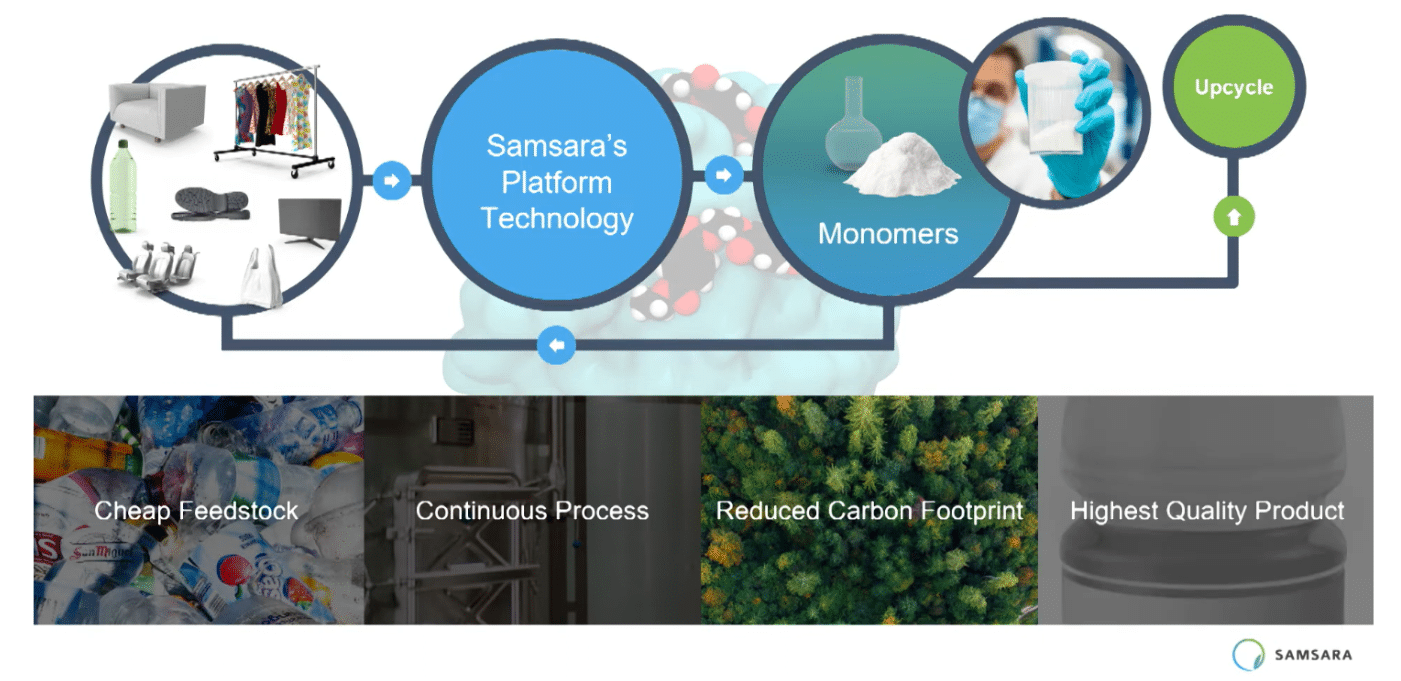

Over 90% of the nylon used in each of the Lululemon Swiftly top samples is from Samsara’s enzymatic recycling process.

Over 90% of the nylon used in each of the Lululemon Swiftly top samples is from Samsara’s enzymatic recycling process.