Nasdaq and Climate Impact X (CIX) entered into a partnership to boost price transparency and liquidity in voluntary carbon credit market.

The agreement will allow CIX to leverage Nasdaq’s technology to power its spot exchange for quality carbon credits.

Nasdaq is a global tech company serving the capital markets and other industries. Over three thousand public companies trade on the Nasdaq exchange.

CIX is a global marketplace and exchange for quality carbon credits. It was born out of a joint venture between DBS Bank, SGX Group, Standard Chartered and Temasek.

This spot trading platform will launch in early 2023 for financial institutions and institutional investors globally.

CIX – Nasdaq Carbon Exchange Partnership

There are several factors that affect the price of carbon credits. These include the type of project that generates the credits and its location. Credit buyers value both factors in a different way.

It’s for this reason that differences in prices result in inconsistency in the market. In effect, there’s a key challenge when it comes to matching a buyer for a certain credit supplier. Plus, this process can also take much time, making the transaction inefficient.

This is where the CIX and Nasdaq partnership comes in to address the issue.

CIX’s Enabling Role

CIX’s spot exchange will match buyers and sellers based on their certain requirements. So, buyers can find quality credits that meet their regulatory obligations.

CIX exchange also gets rid of some restrictions to supplier financing. It will further help promote growth and development of the carbon markets.

The carbon credit spot exchange will also enable a resilient and scalable trading in Software-as-a-Service (SaaS) environment.

CIX CEO Mikkel Larsen remarked that:

“One of CIX’s goals is to create strong pricing signals for the liquid market… Enabling a trade matching process that is as seamless as possible will help to simplify the buyer’s journey and improve price transparency in the voluntary carbon market.”

Nasdaq’s Part in the Deal

Nasdaq’s SaaS technology powers over 2,300 companies in 50 countries. Its global network spans various industries including capital markets operators, regulators, banks, and other market players.

Nasdaq’s platform will allow CIX to bring trading functions to the VCM. In effect, this will help fix the growing complex needs of buyers and sellers of standardized contracts.

According to CIX, the partnership with Nasdaq will bring unparalleled expertise to the industry. Their joining forces is to build a global carbon exchange supported by quality and transparency.

As per Roland Chai from Nasdaq:

“As a technology partner to trusted market infrastructure operators and new markets around the world, Nasdaq is uniquely positioned to collaborate with a marketplace innovator like CIX… to bring their bold climate vision to life through our SaaS technology platform.”

He also added that Nasdaq’s partnership with CIX will help develop and evolve the carbon credit markets.

This agreement is the most recent move of Nasdaq to bridge technology and carbon market transformation.

Early this year, Nasdaq introduced the world’s first 3 carbon removal indexes. Also, CIX and Nasdaq partner Puro.earth had revealed their recent partnership. It intends to increase access to quality nature- and technology-based carbon removal credits.

The African nation of Gabon is planning to make the largest carbon credits issuance ever. 187 million carbon credits will be issued and 50% of which will be sold on the offsets market.

Gabon comes second to Suriname as the most forested nation. The country wants to harvest its forests in a sustainable manner to generate income for the country.

Last April, Gabon submitted an application to be part of ART’s TREES program. It’s the standard for quantifying, monitoring, reporting, and verifying emission reductions and removals from REDD+ activities.

This application covers Gabon’s entire forest spanning 23.5 million hectares. This is where the carbon credits will be from. They’ll most likely end up on the market before the COP27 event.

Carbon Credits from Protecting Forests

Gabon is 88% covered by tropical rainforest. Its forests are part of the Congo Basin, the Earth’s second-largest tropical forest after the Amazon.

Lee White, Gabon’s environment minister, said that preserving forests is “almost a moral responsibility” and a matter of national security. He also said that:

“The Congo Basin forest sends rainfall to the Sahel, Ethiopia and beyond… and a plunge in precipitation elsewhere could destabilize parts of Africa.”

The country is finding ways to preserve its thick carbon sink while diversifying its economy from oil at the same time. It’s the first African nation to be paid for its forest protection efforts. Such an initiative helps forests capture and store more carbon.

In fact, it received its first payment of $17 million from the Central African Forest Initiative (CAFI) for such work.

The carbon credits Gabon plans to sell can be at around $291 million. It depends on the average price for similar projects calculated by a carbon offsets data provider.

This huge issuance may flood the one billion carbon market if the country sells the credits all at once.

Each carbon credit represents a ton of planet-warming CO2 that’s avoided, reduced, or removed from the atmosphere. Firms use these credits to offset their carbon emissions. They can buy credits traded on carbon exchanges or they can also invest in projects that generate them.

There are some doubts in the impact of REDD+ projects in reducing emissions. Other heavily forested countries suspended their carbon credits programs to ensure proper regulation. Indonesia and Papua New Guinea are some examples.

Yet, REDD+ projects remain the most popular in the voluntary carbon market. In fact, they receive the highest prices and have the biggest share of the market value.

Gabon’s carbon credit generation

White addresses the concern by claiming that Gabon has reduced its emissions by 90 million tons yearly. That’s in comparison to its 2000-2009 baseline emissions. And this is due to preserving its forests and avoiding deforestation/degradation.

In particular, the forest elephants in the country’s jungle increase by over 50% to 95,000. Plus, there are several protected wetland sites, heritage sites, and national parks put up. They help preserve and protect the thick forests.

These vegetation-dense forests suck up more CO2 than they emit. Hence, they’re known as carbon sinks.

The environment minister also revealed the plan of TotalEnergies SE to use the credits as its offsets. This would be via the oil major’s acquisition of Compagnie des Bois du Gabon (CBG). It controls more than 1.48 million acres of forest which is about 2.6% of the country’s land mass.

The oil company plans to produce carbon offset credits along with developing a forest management model. The credits generation will be through reforestation, agroforestry and forest conservation.

But the minister said that they’re relying on allowances (concessions) to fuel their timber transformation efforts. They’d banned the export of unprocessed logs to boost this industry.

About a dozen Chinese firms own forest concessions in Gabon, with over 30 others processing the wood.

He also commented that selective logging is one way to boost carbon capture in the long run than no logging.

That’s because the former lets the sunlight reach the soil ground of the forests. And that’s beneficial as it promotes more tree growth. In effect, more carbon is sequestered.

Meanwhile, Gabon is creating its national REDD+ registry to track payments from different projects. All carbon credits created must enter the registry. And even if issuances are from voluntary carbon standards, the government still owns full rights to them.

The US Supreme Court ruling favored the major coal-producing states while limiting EPA’s authority to regulate carbon emissions.

The court’s 6-3 decision supported West Virginia over the Environmental Protection Agency (EPA). The 6 right-wing justices favored the Republican states and dominated the SC ruling.

Chief Justice John G. Roberts Jr. led the majority. He said that it’s not the EPA but the Congress that has the authority to make decisions on fighting climate change.

Three court’s liberals Justices Stephen Breyer, Sonia Sotomayor, and Elena Kagan dissented.

Regulating Carbon Emissions

It’s the most important climate change case to come before the SC in over a decade. The case got support from other Republican-led states such as Texas and Kentucky.

But the Biden administration believes it was unusual as it was after the Clean Power Plan. It’s the strategy of the Obama administration to cut emissions from coal-fired power plants that never came into effect.

The current administration sought to dismiss the case as baseless given the plan never took effect.

But the Supreme Court decided to side with West Virginia which is a major coal mining state. The winning state argued that the EPA doesn’t have the power to reshape its economy by restricting carbon pollution.

Justice Roberts wrote:

“Capping carbon dioxide emissions at a level that will force a nationwide transition away from the use of coal to generate electricity may be a sensible solution to the crisis of the day… But it is not plausible that Congress gave EPA the authority to adopt on its own such a regulatory scheme…”

He also added that a decision of such magnitude and consequence rests with Congress itself, or on an agency it directly forms.

Other conservative justices who joined Roberts are Samuel Alito, Neil Gorsuch, Brett Kavanaugh, and Amy Coney Barrett.

Limiting the government’s power to regulate

The SC ruling reflects the conservative court’s doubt of the federal agency’s regulatory ability. More so when it comes to regulations that go beyond what Congress had authorized.

The outcome hinders broader rules governing the states’ emissions targets and how to hit them. And it can also have sweeping effects on the federal government’s power to set standards and regulate other areas. These include clean air and water, workplace safety and public health

Others believe that it serves as a critical moment for the conservatives aiming to break up the regulatory state. They criticize what they think is the unchecked power of federal agencies.

And so, they decided to go against the EPA and strip it the power Congress gave it to respond to climate change.

In a sense, it may change what the federal government of America is and what it does. Plus, it can also leave technical decisions to a political body that may not understand them as justice Kagan wrote.

“Of course, members [of Congress] can and do provide overall direction. But then they rely, as all of us rely in our daily lives, on people with greater expertise and experience… Those people are found in agencies.”

Environmentalists are rooting for regulations that help tackle climate change. But opposition from the Congress is always there.

For instance, the SC ruling in 2007 also had the same fate. The court ruled that GHG were air pollutants covered by the Clean Air Act of the 1970s.

Then Obama came into office and the EPA was tasked to fight the climate crisis by regulating power plants. The EPA relied on a provision in the Clean Air Act calling to reduce pollution through the “best system of emissions reduction.”

And so the Obama plan came about. Under it, states have to cut their carbon emissions in the most effective way. This includes shifting away from coal-fired power plants to going for solar and wind power.

But the SC ruling in a 5-4 decision prevented Obama’s plan to take effect.

Then the Biden administration promised to come up with similar regulations over power plants. It vowed to cut US emissions in half by 2030 as it rejoins the Paris Agreement.

Over a dozen other Democratic-led states, along with large firms like Apple and Google, supported Biden. They’re also calling for a transition to renewable energy.

But the recent court ruling that limits the EPA’s power to regulate carbon emissions dampens that pledge. West Virginia and other Republican-led states have won the court’s favor not to force emissions reductions.

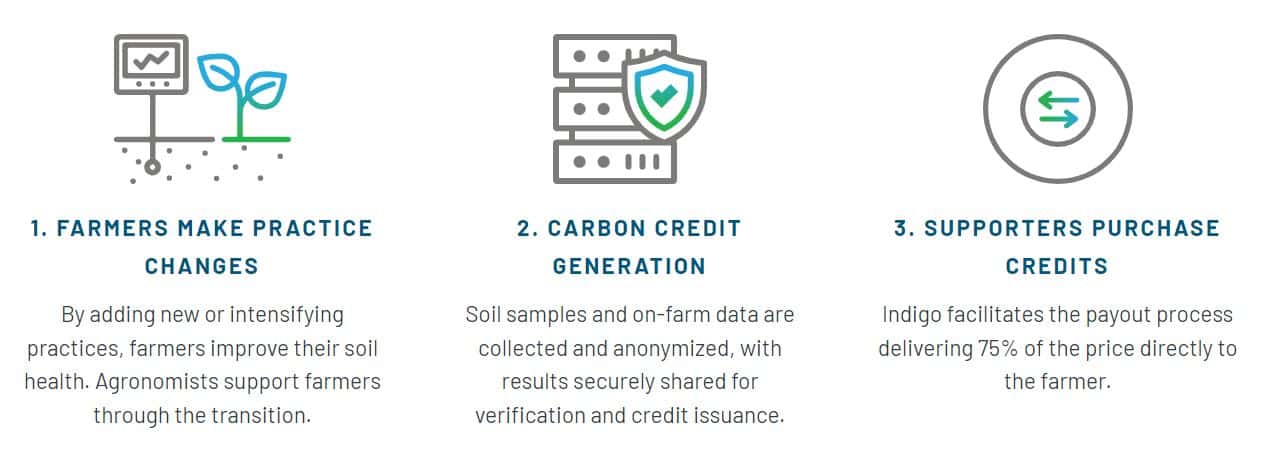

Indigo Agriculture announced its first-ever production of 20,000 soil carbon credits that it will sell as emissions offsets to large companies.

U.S.-based Indigo Ag harnesses science and technology to help improve the sustainability and profitability of the agriculture industry. One of its core products is carbon.

This historic milestone for Indigo’s carbon farming program makes agricultural carbon credits a new revenue stream for farmers. Climate Action Reserve (CAR) will verify and issue these ag carbon credits.

Indigo’s carbon farming program is one of the projects by agriculture firms tapping market-based solutions to capture and store carbon on the farm’s soils. It offers a credible, nature-based climate solution for businesses.

While carbon removal technologies are emerging to help limit global warming, they face the major challenge of scale up. Meanwhile, nature-based solutions have been around in removing greenhouse gases.

Agriculture has historically produced less than 1% of voluntary carbon credits. The issuance of these credits shows how farmers can help mitigate climate change. And that’s through one of the world’s biggest and most vital carbon sinks – the soil.

“It is hard to overstate the importance of this milestone… This issuance validates the role of agriculture in meeting the world’s urgent need for the kind of sustainability and climate solutions… that Indigo’s network of farmers, soil scientists, buyers, and partners have worked tirelessly to realize.”

CAR’s issuance of 20,000 farm soil carbon credits is the very first for generating quality offsets via a carbon farming program. It’s part of the growing voluntary carbon market which experts expect to reach $50 billion by 2030.

Indigo said that partnering with the CAR would reassure buyers of its ag soil credits. Their credit buyers include JPMorgan Chase, Barclays and The North Face.

As for CAR’s President,

“This milestone is the result of a collaborative effort to create an innovative, robust solution for accurate, cost-effective credit generation in agriculture… These credits are tangible evidence that farmers gain a new credible source of income and benefit from the massive global investment in carbon credits needed to solve the climate crisis.”

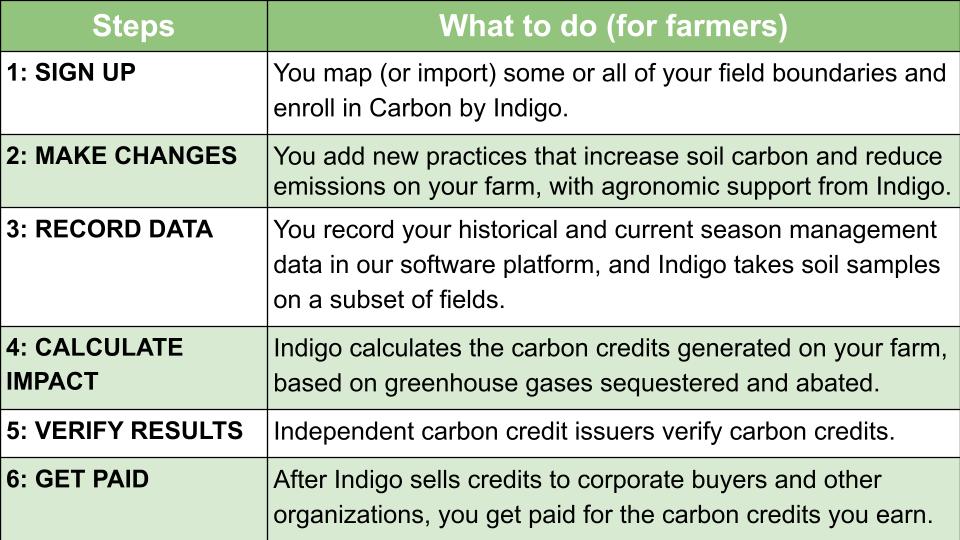

Here’s how ag carbon credit generation by Indigo works:

Generating Soil Carbon Credits

Indigo adopted a hybrid approach that combines soil sampling and modeling to help farmers generate ag carbon credits that meet industry quality standards.

The CAR then verifies and issues the credits for the use of Indigo’s global network of about 20 entities committed to buying credit offsets.

The credits reflect the works of 175 growers/farmers who shifted to climate-friendly farming practices. Others call this regenerative farming that involves planting cover crops and less soil tillage. They cover over 100,000 acres of land during the 2018-2020 growing seasons.

Indigo plans to at least double the amount of credits offered in its next tranche.

There are concerns, however, that make some farmers still hesitant to join carbon farming programs. These are:

Reluctance to make disruptive changes to farming practices

Hesitant to take on the added costs for things like cover crop seed.

But soil carbon credit buyers, especially the big companies, are willing to pay for their environmental value.

In fact, Indigo contracted to sell the credits at $40 per ton, up 100% from $20 in 2020. Farmers who sequester carbon for about 0.3 to 0.6 tons per acre will receive 75% of the price.

Here are the steps how farmers can earn carbon credits via Indigo’s carbon farming program:

To date, there are almost 2,000 farmers and 5 million acres enrolled in Indigo’s carbon farming program. The firm and its partners give farmers the tools they need to take part in the carbon market and enjoy its benefits.

Indigo’s second carbon credit issuance will be early next year. The firm expects it to be at least double the size of its first tranche.

An $11 million grant from Facebook founder Mark Zuckerberg and his wife Priscilla Chan’s foundation (CZI), is exploring using CRISPR gene-editing to remove carbon.

The recipient, the Innovative Genomics Institute (IGI), is looking to enhance the ability of plants and soil microbes to capture and store carbon dioxide.

As per the Intergovernmental Panel on Climate Change (IPCC), Carbon Dioxide Removal (CDR) has an important role in mitigating the impact of climate change. And that’s on top of measures in reducing actual carbon emissions.

When it comes to removing carbon from the atmosphere, the planet has old technologies to do that very well. Plants, microbes, and other organisms have been doing it already. But they’re naturally designed to do the work without the big amounts of too much CO2 from humans.

And so, the IGI project aims to fill this gap by enhancing the natural carbon removal abilities of living organisms. This is important in meeting the scale of the global warming crisis.

Soil Carbon Removal And Storage

One of the key challenges with nature-based CO2 removal solutions is that they tend to draw and store carbon for a short period of time. Soil microbes often respire CO2 not long enough after it has been captured.

In effect, some people are doubting the ability of natural solutions like soil carbon removal to offer significant impact. After all, carbon has to stay in soils for decades for them to aid in abating climate change.

Around two centuries ago, soils were reliable and long-term carbon sinks. Also, plants and microbes not only have the ability to capture CO2 from the atmosphere. They can also store it in biomass and in soils of croplands covering ⅓ of the Earth’s land surface.

In a sense, focusing on globally important commercial crops like rice ensures that the impacts of adopting this CDR spreads around the world and benefits communities.

But that was until modern agriculture was born and altered things.

For instance, disrupting the soil structure like converting forests and grasslands to farmland, speeds up the process of releasing the captured carbon. When this happens, the planet heats up more.

Since then, soils have released about 487 billion metric tons of CO2. That’s a huge amount, representing the U.S.’s cumulative fossil CO2 emissions since the industrial revolution.

This is where the IGI team enters by grabbing the chance to boost the levels of soil carbon in agricultural lands. Doing so will not only benefit soil structure and reduce emissions. It can also improve water use efficiency and nutrient availability, and feed the good microbes.

Aside from enhancing soil carbon removal ability, the research team expects other benefits, too. These include higher yields and reduced amounts of fertilizers and irrigation. All these can help the whole population.

Plus, farmers or ranchers can also have another revenue stream by earning soil carbon credits. They’re credits that correspond to certain amounts of verified carbon captured and stored in the soils.

CZI’s Investment in IGI’s CRISPR Tech

CZI has been investing in innovative technologies to help fight climate change. CDR technologies are one of them and the IGI program is one of its supported initiatives.

The IGI team is one of the first to use CRISPR genome editing in the field of CDR.

These include correcting genetic defects, treating and preventing the spread of diseases, and improving the growth of crops.

This technology was adapted from the natural defense mechanisms of bacteria and other microorganisms. With this new study, the IGI team thinks that it becomes possible to enhance plants and soil microbe’s carbon capture.

That could be a net increase of 1.4 billion metric tons of CO2e drawn in each year. Half of that can be kept in the long-term if combined with biomass conversion technologies.

Dr. Chan, CZI’s co-CEO and co-founder said that:

“We’re excited to support the Innovative Genomics Institute’s important research into new applications of gene-editing technology… This has the potential to supercharge the natural abilities of plants, enabling them to pull more carbon out of the atmosphere and store more carbon in their roots and the surrounding soil…”

Chan believes that it will provide a new set of innovative tools to address climate change.

As for CRISPR’s application to soil carbon removal, it’s equally a thrilling step on how it was also used in agriculture.

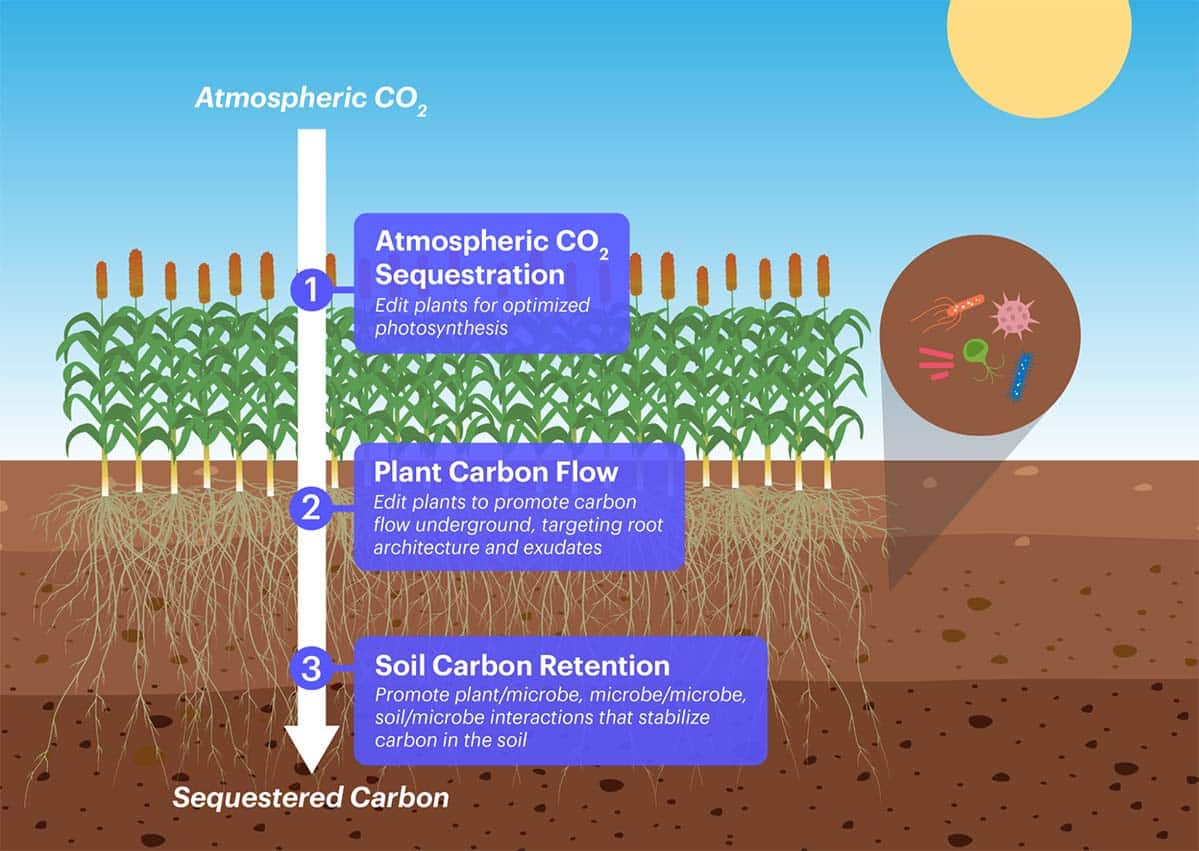

The IGI Program in 3 Groups

As shown in the image below, the IGI’s soil carbon removal program includes three groups. They’re composed of researchers at UC Berkeley, UC Davis and Lawrence Livermore National Laboratory. Each focuses on a different stage of the CO2 journey from the air through plants to roots and into the soil.

1st group: focus on editing rice varieties for improved photosynthesis to remove CO2 from the air. Optimize root development to boost soil CO2 sequestration.

2nd group: develop new genome editing protocols for the biomass crop sorghum to allow editing for enhanced CDR.

3rd group: create techniques to trace CO2 fixed by improved cultivars. Study soil microbial communities that promote long-term CO2 storage.

The success of this initiative in impacting the real-world scenario calls for widespread adoption. And so, another group will ensure that the progress of the teams’ work meets the users needs.

Though efforts were started in local fields, this soil carbon removal is meant to scale up rapidly around the world.

The IGI team’s work is scalable as it also applies to other crops, such as wheat and corn.

The world of carbon offsets and carbon offset programs can be quite complex and intimidating. So, if you’re looking for the best carbon offset programs for 2024 but don’t know your options, this article will guide you through.

You’ll learn the important concepts, which carbon offset program should you choose, and why investing in this space matters.

What is a Carbon Offset?

First things first. We need to define what does it mean by a carbon offset.

Essentially, it refers to a credit bought by an individual or entity to compensate for its carbon emissions or footprint. One carbon offset generally represents one ton of CO2 reduced or removed.

And so carbon offsetting means financially supporting a project that can reduce emissions.

Carbon offsets are produced by companies that remove CO2 from the atmosphere. The offsets are then sold to firms that emit (or have emitted) CO2 into the air.

In a sense, you can think that offset-producing entities are funded by companies that emit CO2 or its equivalent.

A very identical concept to carbon offsets is carbon credits. While both terms are created for the same goal – to abate climate change – carbon credits are originally created through government regulations.

The government limits the amount of GHG that companies can emit by setting a cap on them with certain tons of CO2 emissions they’re permitted to emit. These allowed emissions correspond to carbon credits.

Same with a carbon offset, one carbon credit equals one ton of CO2 reduced or removed.

Below is the rising trend of voluntary carbon offsets issued since 2017 in metric ton CO2e.

Carbon offset project vs. carbon offset program

Many people often take carbon offset programs one and the same as carbon offset projects. But they’re actually two different concepts.

A carbon offset project is an initiative developed to reduce actual GHG emissions. It can be in any sector, agricultural to industrial.

On the other hand, a carbon offset program refers to a set of standards made by an organization to measure, regulate, and review carbon offset projects.

The best carbon offset programs are also known as carbon standards or registries. They allow individuals or companies to invest in carbon offset projects locally or internationally to balance their carbon footprint. They ensure that the projects are trustworthy.

Here are the 4 largest and best carbon offset programs for 2024 that you can find in the market. They all have a solid track record of performance that you can verify.

Top 4 Carbon Offset Programs

Let’s discuss each one of them in detail so that you know which one fits for your carbon offsetting needs.

1. Verra: The Verified Carbon Standard

Verra is a non-profit organization headquartered in Washington, D.C. Since it was launched in 2006, Verra’s VCS is the most known voluntary carbon offsetting program available today.

It’s the world’s most widely applied program and you’re most likely familiar with its logo. It appears when you decide to offset your carbon footprint when buying airline tickets.

Offset projects certified by VCS Program

To date, Verra has more than 1,806 certified VCS projects that collectively reduced or removed over 928 million tons of CO2 and other GHG emissions. The VCS program allows certified projects to turn their GHG emission reductions and removals into carbon credits.

The Program focuses on GHG reduction attributes only and does not require projects to have additional environmental or social benefits. It’s supported by the carbon offset industry players – project developers, big offset buyers, verifiers, and projects consultants.

The projects in Verra’s carbon offset program fall under 15 major sectors. They all undergo Verra’s rigorous rules and requirements. They include a number of technologies and measures that reduce or remove CO2 and other GHGs.

These involve the renewable energy, forest and wetland conservation/restoration, transport efficiency improvements, and more.

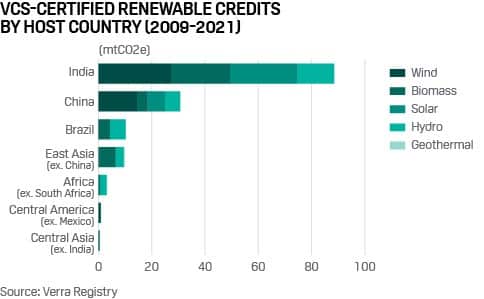

When it comes to renewables, here’s Verra-certified credits by country from 2009-2021.

Same with the other best carbon offset programs for 2024, Verra issues a unique number to each carbon credit generated by an offset project.

These numbers are called Verified Carbon Units, or VCUs. Individuals and companies wanting to offset their emissions can buy these credits in various carbon exchanges in the VCM.

VCS is also working to develop carbon crediting procedures for seabased activities, such as kelp farming, sustainable fishing and seagrass meadow restoration.

These projects have the potential to reduce or remove over one billion tons of CO2 from the air each year, all while restoring ocean ecosystems.

How does the VCS process work?

A process exists for approving GHG programs that meet VCS Program criteria. The project/program should meet the following criteria:

must comply with the VCS Program,

hire an external qualified consultant team for a detailed gap analysis of the two programs to evaluate the proposed program, and

then the Verra Board decides to either fully adopt or adopt elements of the other offset program

If an entire offset standard is adopted by the VCS, all the auditors and methodologies are automatically accepted. Also, credits certified by that standard can be fungible with VCUs.

Verra periodically reviews approved programs to ensure compliance with the VCS Program.

2. The Gold Standard

The Gold Standard (GS) is a voluntary carbon offset program unique from others. Unlike Verra, it puts the UN Sustainable Development Goals (SDGs) front and center when certifying offset projects.

GS was developed with the leadership of the World Wildlife Fund (WWF), HELIO International, and SouthSouthNorth. It focuses on offset projects that provide lasting social, economic, and environmental benefits.

Also, the GS program is applicable to both voluntary offset projects and to Clean Development Mechanism (CDM) projects.

The GS CDM was launched in 2003 after a 2-year period of consultation with stakeholders, governments, non-governmental organizations, and private sector specialists from over 40 countries.

The GS for voluntary offset projects also known as GS Verified Emission Reduction or VER was launched in 2006. The project registry which contains all projects implemented through the GS program took off in 2018.

Offset projects that Gold Standard certifies

For a carbon offset project to be accepted by GS it must perform assessment of its community impact. It must also ensure that populations nearby are also benefiting from the project.

In general, offset projects need to contribute to at least 3 out of 17 UN SDGs to be certified. And like other best carbon offset programs, GS projects fall under these major categories:

renewable energy,

reforestation, and

community service projects (waste management)

Most of the GS projects are in developing, low, and middle-income countries.

Why offset with Gold Standard?

In a word, impact. This means that every dollar, Euro, pound or peso you spend offsetting creates more value for local communities and ecosystems. It also contributes in a measurable way to the UN SDGs.

The Gold Standard is considered one of the most rigorous carbon credit programs for 2023. In fact, over 80 NGOs are endorsing it, including the David Suzuki Foundation and WWF.

To date, about 2,000 GS-certified projects in over 80 countries have prevented >173 million tons of CO2 emissions.

You can directly support projects certified by Gold Standard through its site. Prices vary per type and purpose. You can also buy credits for Gold Standard–verified projects through various carbon retailers or exchanges.

3. Climate Action Reserve (CAR)

Climate Action Reserve began in 2001 as the California Climate Action Registry. Its mission is to encourage companies and other organizations to measure, manage and reduce GHG emissions.

The CAR is a national offsets program focused on ensuring environmental integrity of GHG emissions reduction projects. Its main purpose is to support financial and environmental value in the voluntary carbon market. CAR does that by:

establishing high-quality standards for quantifying and verifying GHG emissions reduction projects,

overseeing independent third party verification bodies,

tracking the credits over time on a transparent and accessible system.

CRTs are developed and quantified using project protocols. Adherence to these standards ensures emissions reductions are real, additional, and permanent.

Offset projects that CAR certifies

CAR registers and certifies carbon offset projects based on their permanence. Their GHG reductions must also be accounted for and audited.

And same with Gold Standard, CAR also considers the project’s social and economic benefits. But not all carbon offset programs in 2023 do that.

Most of CAR’s projects include:

Coal mine methane capture,

Landfill gas collection,

Forestry and grassland

Even rice cultivation

They’re in the United States but CAR also certifies projects in Canada and Mexico.

All carbon offset credits generated by CAR-certified projects are given a unique serial number. This helps tracking each project effectively.

More importantly, the number assures buyers that a “retired” credit isn’t eligible for selling or transferring. Retired means credits have already been used to offset emissions.

All project information is publicly available in the CAR system.

Why choose CAR?

CAR is considered the premier voluntary carbon offset program for the North American carbon market. In 2021, CAR achieved more than 150 million metric tons of GHG reductions.

CAR doesn’t sell carbon credits directly to consumers. To buy carbon offset credits, you’ve to go directly to a retailer. Then look for the CAR seal of approval.

Examples of retailers that sell CAR-verified credits are Cool Effect, Carbonfund.org and Sterling Planet.

CAR’s emission reduction program has been approved under the Verra’s VCS. CRTs issued by the Reserve can be converted into Verified Carbon Units (VCUs) and transferred to a VCS registry. But VCUs cannot be converted into CRTs.

4. American Carbon Registry (ACR)

ACR is a pioneer on the voluntary emissions and carbon market. It was founded back in 1996 by the Environmental Resources Trust (ERT) as the first GHG registry.

The registry became the American Carbon Registry (ACR) in 2008. And in 2012, ACR was accepted as an approved Offset Project Registry by the California Air Resources Board (CARB). It’s the regulatory body of the California cap-and-trade offset credit market.

ACR operates in both voluntary and regulated carbon markets.

Offset projects that ACR certifies

Projects certified by the ACR are found worldwide and include the following:

improved forest management,

recycling of transformer oil,

carbon capture and storage,

ACR uses “science-based carbon offset standards” for evaluating projects. The program requires projects to show permanent carbon reduction or removal.

Among the many projects that ACR supports is a truck stop electrification initiative. It employs plug-in units that can reduce around 4.1 million tons a year.

It also supports projects that offer farmers financial incentives to voluntarily reduce emissions by curbing their use of nitrogen-based fertilizer.

Why select ACR?

ACR isn’t only the oldest kid on the block when it comes to carbon offset programs. It’s also trusted by the ICAO or International Civil Aviation Organization to supply emission reduction units for the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

It’s a scheme that can offset 2.6 billion tons of carbon over the next 14 years.

As with Verra and CAR, you’ll need to visit a carbon retailer or exchange to buy carbon offset credits from ACR-certified projects.

ACR methodologies and protocols are all based on International Standards Organization (ISO) 14064. The program allows project developers to use methods and tools from the CDM. But as long as they go with the ACR’s own standards.

Projects may be transferred between ACR and another registry provided all unsold, non-transferred, and non-retired offset credits are canceled.

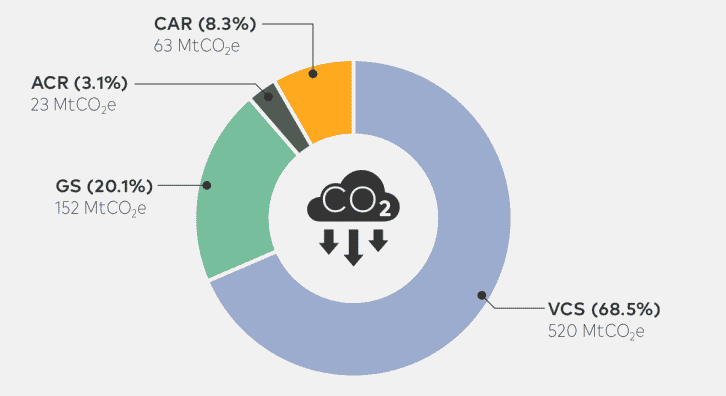

Overall, ACR has a 3.1% share of credits issued in the VCM as shown in the chart. CAR gets the 8.3% credits share while VCS and GS issued 68.5% and 20.1% of credits, respectively.

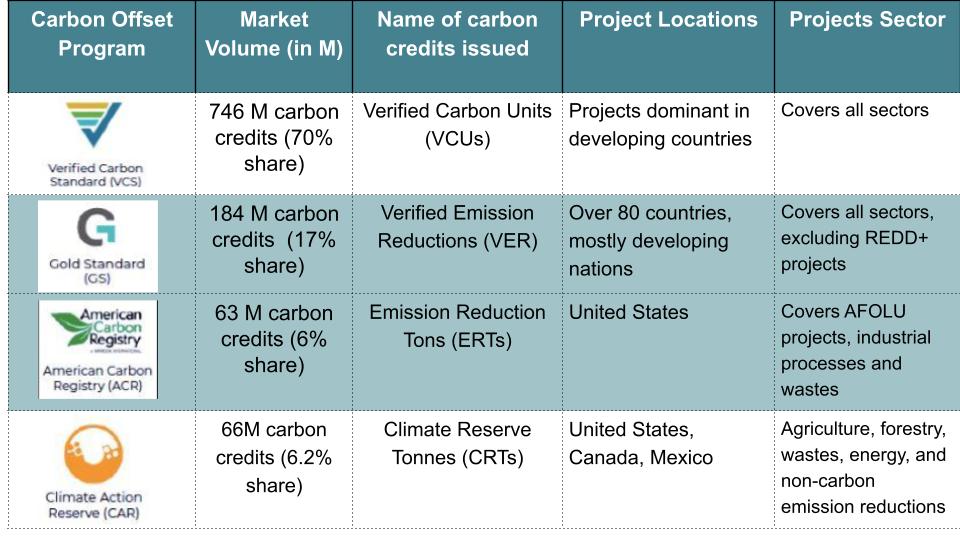

In summary, the table below shows the key comparison among the 4 best carbon offset programs to consider in 2023.

So, why does offsetting your carbon footprint matter?

Take note that offsets aren’t a replacement for actual emissions reduction. BUT they can make a big difference in helping the fight against climate change.

By deciding to buy carbon credits through any of the carbon offset programs above, you’re helping a project remove or prevent planet-warming emissions.

The best part is that buying carbon offset credits will eliminate the last traces of your carbon footprint. For companies, this means addressing their unavoidable emissions.

So, investing in carbon offset credits hits two birds with one stone. It allows you to help people who benefit from the projects and help protect the planet at the same time.

DeepMarkit highlighted its most significant achievements from the first half of 2022. The company focuses on transitioning the global carbon offset market to the more accessible digital economy by minting credits into non-fungible tokens (“NFTs”),

DeepMarkit is also pleased to observe the growing industry consensus of the blockchain becoming a tool for helping traditional carbon trading systems transition into the modern age.

Following its acquisition of First Carbon Corp., DeepMarkit’s most notable highlights this year include:

CA$4.83 million raised via private placements, including Radiance Assets Berhad as a company shareholder;

Registration on the Gold Standard and Verra carbon registries;

Have definitive collaboration agreement with Radiance for introducing carbon credit projects to its MintCarbon.io platform;

Executed an LOI with Top Energy with respect to the minting of clean energy NFTs;

Entered into a $20 million carbon credit Liquidity Support Agreement with Radiance;

Completed 3 inaugural tests (minting, listing, and retiring of carbon credit NFTs)

Became one of Polygon’s key sustainability partners

Engaged Quantstamp for security assessment services; and

Executed an LOI with Japan-based BloomX to introduce MintCarbon.io to the Asian market.

DeepMarkit considered blockchain a natural fit for the industry as a tool to track creation, ownership, and retirement of carbon credits as MintCarbon.io is doing. Via this platform, it’s easy to view, share, and link a project’s profile and story to any blockchain-enabled marketplace.

Thus, DeepMarkit reassures that carbon credit NFTs do help individuals and companies alike to manage their emissions and operate in a carbon-based budget long into the future.

Google is giving access to its Earth Engine to all government and commercial entities. Google Earth Engine launched over a decade ago and access was only granted to researchers, academia, and non-profit organizations.

It is one of the world’s largest, publicly available collections of the Earth’s observation data, combining high-resolution photos and data that allow companies to know how their operations impact the environment.

Google is also launching a Carbon Footprint for Google Workspace will be ready in 2023. It will help users measure, report, and reduce emissions on Google services such as Gmail, Docs, and Meet.

Carbon Emissions Tech: Google Earth Engine

Digital technology always has a role to play in helping other sectors to decarbonize. Justin Keeble, managing director at Google Cloud, noted that,

“Even a small choice for an organization… [For example,] when to proactively water crops ahead of a drought, which green funds to invest in — requires understanding unique and often complex information.”

Earth Engine is a platform for scientific analysis and visual representation of geospatial data for various users. These include academic, non-profit, business, and government users.

Earth Engine hosts satellite imagery and stores it in a public data archive. This data storage includes historical earth images even going back over 40 years. The images are then available for global-scale data mining.

The technology allows one to analyze forest, water coverage, and land use changes. Users can also use it to assess the health of agricultural fields.

With it, users can detect changes, map trends, and quantify differences on the Earth’s surface.

According to users, the World Resources Institute, for instance:

“Google Earth Engine has made it possible for the first time in history to identify where and when tree cover change has occurred at high resolution… Global Forest Watch would not exist without it.”

Potential Carbon Emissions Reduction

The International Energy Agency has set net zero emissions by 2050. This particularly involves the energy, materials, and mobility sectors.

If scaled up across industries, Google Earth Engine can deliver up to 20% of the IEA’s emissions reduction.

A study by the World Economic Forum said that those industries can reduce emissions by 4% – 10% with the help of digital technology. Though not as significant as energy, the technology sector also contributes to carbon emissions in other industries.

A digital carbon footprint refers to the emissions from the production, use and data transfer of digital devices and infrastructure.

In particular, global email usage produces as much CO2 as having 7 million more cars on the road. And so limiting email use can result in meaningful impact.

Take for example the case of email users in the UK alone. If each of them is sending one less email daily, about 16,433 tonnes of CO2 emissions can be reduced. This reduction is equal to 81,152 flights from London to Madrid.

The same use of Earth Engine is possible in many other applications. Thanks to it being one of the largest publicly available data catalogs.

Plus, its global data archive covers the past 50 years and is updated every 15 minutes.

The service can detect trends and understand correlations between human activities and their environmental impact. And that becomes “more precisely than ever before”. This makes Earth Engine a vital tool both for firms and organizations as they tackle climate change effects.

Companies can use Earth Engine in planning and achieving their carbon emissions reduction targets. At least a fifth of large public firms have set their net zero goals by 2050 at the most.

As Mr. Keeble also said, businesses and individuals alike are wondering how to turn sustainability ambition into action. This Google imagery service offers a potential tool for that purpose.

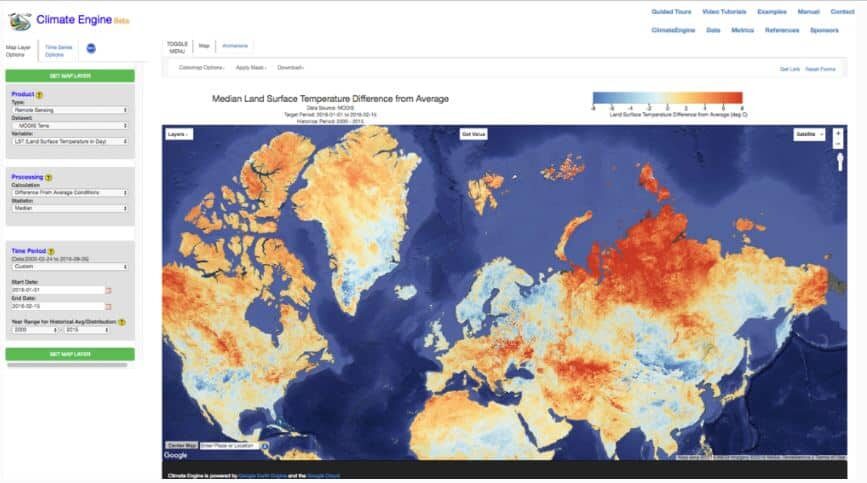

The image below shows a sample use of the technology by Climate Engine to create an interface that can display time-series mapping information. It enabled scientists to obtain surface climate-based data easier and faster.

Carbon Footprint Tracker

The upcoming Carbon Footprint for Google Workspace service will also have a tool designed to help users access emissions data. It will allow them to track their emissions or to report disclosures.

Same with Earth Engine, the carbon footprint tool will help users assess their environmental impact. It will help them measure and thus, reduce their carbon emissions using Google Cloud services.

In a sense, the tools will aid companies to come up with carbon emissions reduction solutions as the world transitions to net zero.

Vibrant Planet raised a $17M seed round to expand its technology focusing on forest restoration across the Western U.S., Europe, and other at-risk forests worldwide.

Public sector funding to support wildfire risk reduction and forest restoration is on the rise. Yet, there’s no infrastructure to help know where and how efforts must be used to maximize impact.

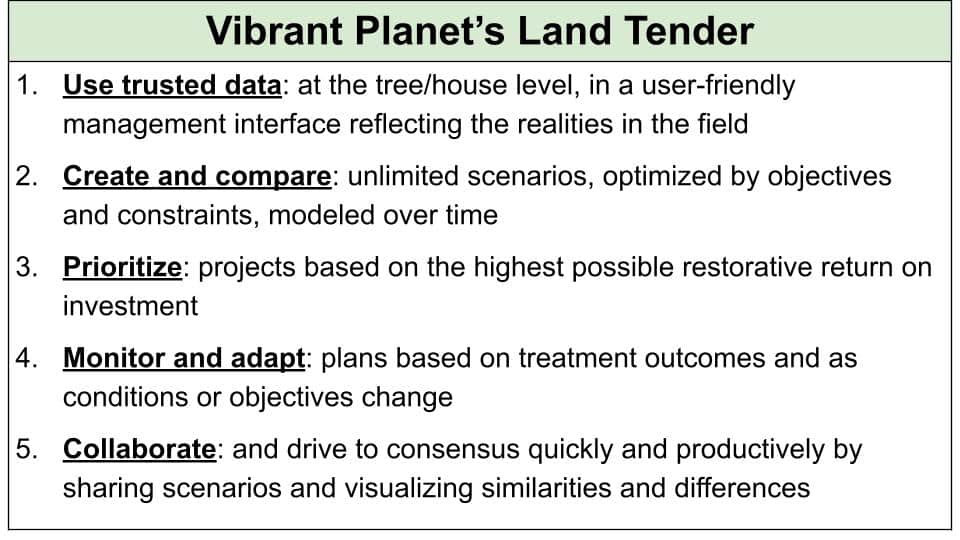

The startup is developing “Land Tender” a Software as a Service (SaaS) platform for forest management.

Vibrant Planet SaaS for Forest Restoration

For the company’s CEO, Allison Wolff:

“We just need to do this — we need to restore forests faster, and they might make it through climate change, and they might help us survive climate change.”

The firm raise a $17 million funding as wildfire season is taking hold again in the West.

Lead investors include the Ecosystem Integrity Fund and The Jeremy and Hannelore Grantham Environmental Trust.

Other investors include:

Valia Ventures,

Earthshot Ventures (backed by John Doerr, Tom Steyer, Microsoft, etc.),

Elemental Excelerator,

Cisco Foundation,

Day One Ventures,

Data Tech Fund, and

Halogen Ventures.

The seed funding will enable Vibrant Planet to grow its team and expand its platform to restore resilience of at-risk forests.

Prior investors include two of Silicon Valley’s top platform creators from Meta and Netflix.

The firm offers the first operating system in the field – Land Tender. It’s for forest treatment planning, decision support, monitoring and reporting, and investment prioritization. It gives organizations, public agencies, and land managers a comprehensive platform.

Vibrant Planet’s technology allows land owners, managers, and administrators to:

Make forest treatment scenarios in real-time with the AI-backed data.

Prioritize where and how funding should be used to cut risks. This will also maximize carbon, water, and biodiversity benefits.

Develop treatment plans together with stakeholders.

Keep track and report on landscape conditions and forest restoration progress.

Use strategies and tactics based on monitoring insights.

Create verified fire-adapted forest carbon projects that aid firms to reach net zero targets.

How the Tender Land Platform Works

Land Tender is a cloud-based planning and monitoring tool for agile, adaptive land management at any scale.

Through Tender Land, users can prioritize their objectives in relation to forest restoration.

For instance, they may prefer to pay attention to fire risk or endangered species conservation. Or they can also look at water quality as the key matter.

Users can then run analysis to know how different landscape treatments can impact their priorities.

Vibrant Planet also offers access to a range of datasets on forest restoration. The centerpiece is a lidar map of the state of California where 6.5 million of its 33 million forested acres burned over the last two fire seasons.

Not to mention that 1.3 million acres of California’s forests experienced high severity burning that killed biomass. In these cases, it may take decades to centuries for forests to recover.

The importance of restoring resilience to key forest landscapes has never been greater. Forests store a third of the carbon dumped by humans into the air each year. They also have a vital role in regulating weather patterns and global warming.

Vibrant Planet focuses its efforts on at-risk forests like in California and the Mediterranean regions. They’re where climate change is hitting the hardest.

The firm sells Land Tender via licenses which cost $3,500 each. This lidar technology is helpful when it comes to mapping forests in 3D and learning their fire risk.

Even dense forests, which are hard to map, are possible with an AI-powered algorithm of Land Tender.

Here’s how this forest restoration platform helps users and stakeholders:

Vibrant Planet’s offering covers the competitive annual pricing for ArcGIS, the industry-standard geographic information system.

It also has less expensive offers depending on the types of ArcGIS extensions a group might spec to meet their needs.

The main difference, though, is that the firm includes a host of data that users would need to find on their own. Plus, what sounds like some clever collaboration tools.

In the words of Dr. Neil Hunt from Vibrant Planet:

“Vibrant Planet is seizing the opportunity to bring modern cloud-based technology, remote sensing, AI/ML, and intuitive user-centered design to create systems that reduce the time and cost of decision-making in forests…”

He further said that developing carbon credits will help fund the interventions necessary to restore forest health and resilience. Large companies buy carbon credits to offset their hard-to-abate carbon footprint.

The second step of the firm’s business model is to provide data and analysis to develop carbon credits. They correspond to certain amount of carbon avoided/removed from the air through the forests.

But this plan is yet to be decided and revealed.

Vibrant Planet’s platform will be available for users across California by the end of the year. It will also be ready in other Western states where demand starts to take off throughout next year.

The company further said it can add more regions or countries depending on the availability of lidar data.

The World Gold Council (WGC) analyzes the impact of climate transition on the gold industry and its stakeholders, focusing on power emissions.

The WGC and its members recognize the risks that climate change brings to the global economy and on the gold sector’s future.

Hence WGC, the global experts on gold, focuses to bring a clearer understanding of how climate-related risks can affect the entire industry.

The group does this by conducting research and promoting how responsible gold mining as a key aspect of its ESG supports the transition to a low carbon economy.

WGC’s Gold and Climate Change

Mining is a very energy-intensive industry that uses up to 11% of total global energy consumption. Estimated emissions for the global gold market are around 126.4 Mt CO2 equivalent a year.

The WGC identified that the major source of the gold’s greenhouse gas (GHG) emissions are from its mining operations. They represent the sector’s Scope 1 (direct) and Scope 2 (indirect) emissions.

For each ounce of gold produced that is roughly 800 kg CO2 (or 0.8 carbon credit equivalency).

About 95% of those emissions come from the power or fuel used in the sector (power emissions). Of this, electricity represents the largest source of emissions at the mine site.

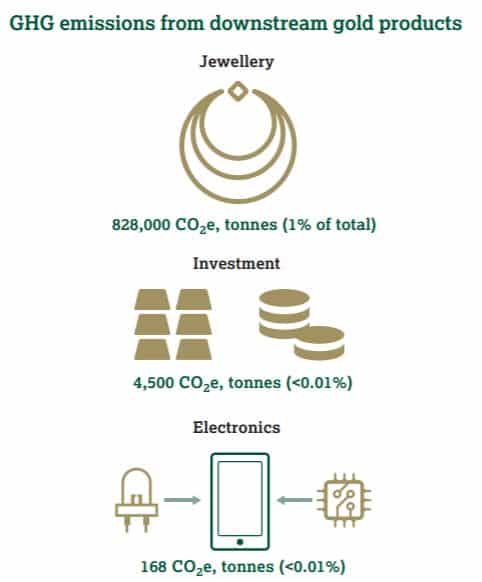

The group also confirmed that carbon footprint from gold’s downstream (Scope 3) uses are relatively small. Here’s gold’s GHG emissions from its total downstream products.

Power emissions indeed play a big part in gold’s total carbon footprint. WGC seeks to provide an analysis of the potential impacts of changes in gold mining’s electricity generation.

More importantly, it aims to offer knowledge of how those changes may reflect the industry’s ability to meet climate targets.

This is to help investors and the wider stakeholder groups to be open to more opportunities as they seek to decarbonize energy sources.

Gold Net Zero Targets and Pathways

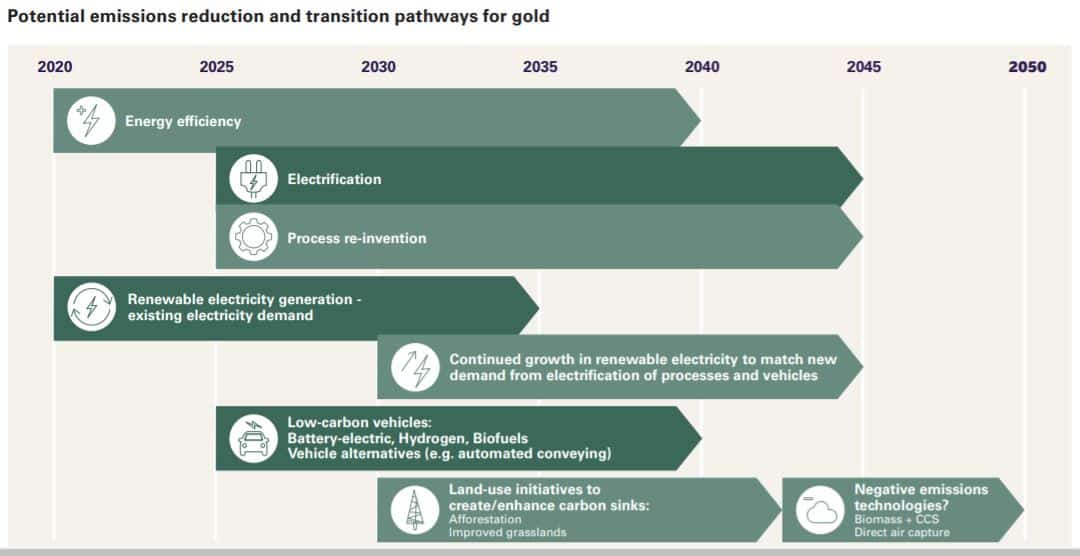

Based on its analysis, WGC outlined a range of possible steps and pathways for the industry to net zero. The image below shows these options.

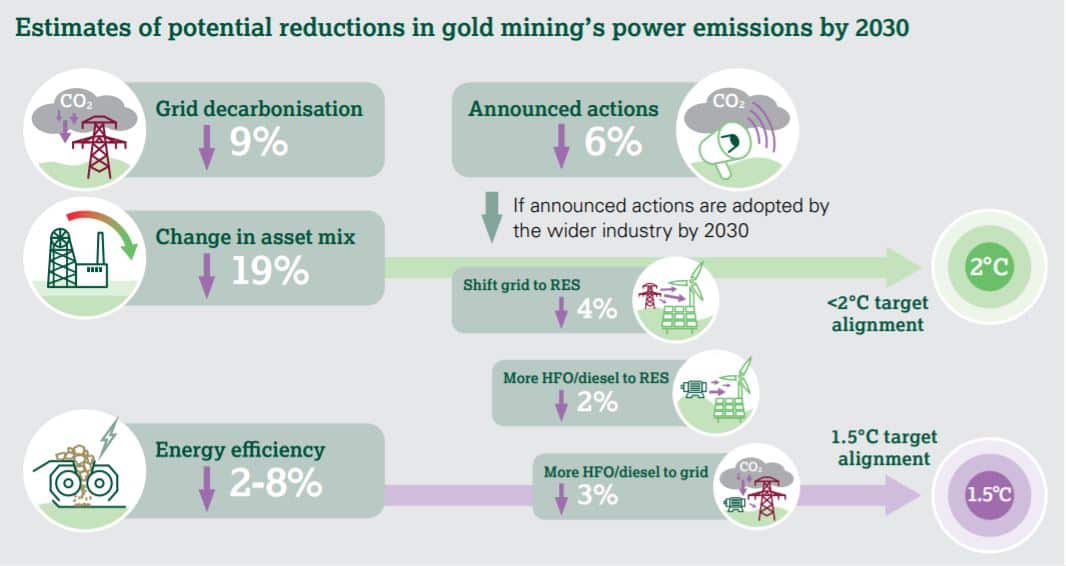

The WGC estimated that the emissions pathway needed for the industry to help limit global warming to <2ºC calls for an emissions reduction of 80% by 2050. And if the industry wishes to achieve a 1.5ºC target, a 92% reduction by 2040 is necessary.

More so, gold mining companies need to achieve around 27% or 46% non-power emissions reduction by 2030.

Today, grids are transitioning to lower emission power sources. And WGC projected that this will translate to a 20% reduction in the emissions intensity of gold mines grid power by 2030.

That’s because new initiatives from gold miners are now focusing on cleaner electricity consumption. Solar energy is their top renewable energy source.

Solar is the preferred technology due to its relatively low cost, scalability and frequent geographic fit.

If single actions were taken to enable 1.5ºC target alignment, this requires either:

replacement of 55% or more of direct fossil fuel generated power with renewables or

replacement of 30% or more of grid supply with renewables.

So overall, the current net zero commitments by WGC gold miners show the vital role of energy in driving more emission reductions in the sector.

But there’s one more important finding that the WGC highlighted as the industry transitions to a low carbon future. That’s the impact of introducing gold as a strategic investment to a global multi-asset portfolio.

Aligning Investment Portfolios with Paris Agreement

One important finding of the group is that holding gold in a diversified portfolio can help reduce its carbon footprint.

For example:

For a portfolio of 70% equities and 30% bonds, introducing a 10% allocation to gold (and reducing the other asset holdings by equal amounts) reduced the emissions intensity of portfolio value by 7%, and a 20% holding in gold lowered it by 17%.

And so, the WGC suggested that gold may play a positive role in mitigating portfolio climate impacts.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")