Disseminated on behalf of Surge Battery Metals.

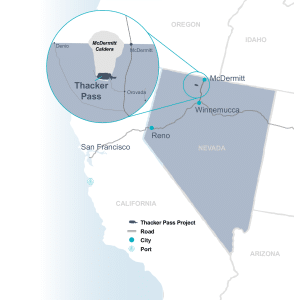

Lithium Americas (LAC) has officially broken ground at Thacker Pass, Nevada. The project is advancing toward its first production target in 2028. LAC CEO Jonathan Evans said in the company’s news release that the project should be mechanically complete by the end of 2026. Commissioning will happen through 2027, with commercial production starting in 2028.

For investors watching Nevada clay lithium, this milestone is more than an update. It’s a market signal that could change the investment landscape.

De-Risking the Clay Lithium Category

For years, clay-based lithium has faced a single recurring objection: “It has never been done at a commercial scale.” Unlike brine or hard-rock lithium, sedimentary clay deposits presented a technological and operational unknown. Investors and lenders were cautious, capital costs were higher, and early-stage projects struggled to secure financing.

Thacker Pass changes that narrative. Once LAC makes battery-grade lithium carbonate from sedimentary clay at a commercial scale, it reduces risks for the whole category. Projects in Nevada now have clear proof that clay-based lithium can be mined and processed effectively.

The historical precedent is instructive. In Chile’s Atacama region, the first brine lithium projects proved the chemistry and cost-effectiveness of large-scale lithium extraction. Later projects attracted capital more easily and on better terms. This created a ripple effect, speeding up the region’s lead in global lithium supply.

Thacker Pass is playing that same role for sedimentary clay. Its success is not just a win for LAC. It marks a key milestone for the whole Nevada clay lithium sector, including the Nevada North Lithium Project (NNLP) of Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF).

Understanding the Technical Landscape

Thacker Pass Phase 1 has lithium levels of 1,500–2,500 ppm. They plan to extract it using sulfuric acid leaching to create battery-grade lithium carbonate. The project is important both geographically and operationally.

It features a large pit, a big processing facility, and integrated infrastructure. This covers access roads, water supply management, and energy sources that meet Nevada’s rules.

While Thacker Pass shows commercial viability, it is crucial to note that NNLP and Thacker Pass are not technically the same. NNLP employs a different beneficiation approach and reagent chemistry to optimize recovery.

NNLP: The Higher-Grade, Next-Generation Project

Thacker Pass shows clay lithium on a large scale. NNLP positions itself as the next evolution of this asset class, with clear geological advantages:

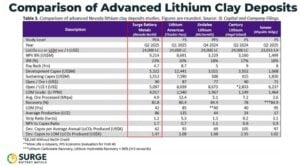

- Grade: NNLP averages 3,010 ppm lithium, significantly higher than Thacker Pass Phase 1 material. Recent drilling results show that step-out drilling found a 31-meter intercept with 4,196 ppm lithium from surface. This gives NNLP a potential extraction advantage.

- Strip Ratio: NNLP’s 1.16:1 strip ratio is among the lowest in the sedimentary clay peer group. This indicates that it has favorable material movement requirements relative to ore recovered.

- Operating Costs: NNLP’s estimated OPEX is US$5,097/t LCE, lower than Thacker Pass guidance of ~US$6,200/t C1. It suggests that it has competitive economic positioning within the peer group.

Both projects produce battery-grade lithium carbonate using sulfuric acid leaching. However, each method is customized for the specific geology of the project. NNLP is not a copy of Thacker Pass. Rather, it is a next-generation clay project designed to leverage lessons learned while improving key parameters.

Moreover, infill drilling showed a steady, thick, high-grade core. It included intercepts like 116 meters at 3,752 ppm Li and 32 meters at 4,521 ppm Li. These results support future resource expansion. They also highlight the project’s scale, quality, and technical readiness as it prepares for a Pre-Feasibility Study.

- SEE MORE: Surge Battery Metals Strengthens Nevada North With High-Grade Expansion and Infill Success

Why Category De-Risking Matters for Investors

In emerging resource sectors, de-risking is often more valuable than the resource itself. Projects that validate a new extraction method or commodity unlock several market advantages:

- Lower financing risk: Investors are more willing to fund projects once proof of concept exists.

- Improved capital terms: Lending rates and equity expectations can improve when technology and economics are validated.

- Accelerated project development: Developers can move faster, reduce contingencies, and focus on optimization rather than proving viability.

Thacker Pass’s progress effectively removes the “first-mover risk” from sedimentary clay projects. NNLP has higher grades, near-surface mineralization, and competitive OPEX. Now, it can be assessed on its own merits, not on doubts about large-scale clay processing.

Strategic Significance in the U.S. Lithium Market

The timing of Thacker Pass’s construction and NNLP’s development aligns with broader policy and market trends. Lithium is a critical input for electric vehicles, grid-scale storage, and advanced defense technologies. The U.S. government has emphasized domestic lithium production as a strategic priority.

In March 2025, President Trump signed an executive order called “Immediate Measures to Increase American Mineral Production.” This order directs federal agencies to speed up permitting and support domestic projects. It also aims to lessen dependence on foreign supply chains for critical minerals.

Projects like Thacker Pass and NNLP benefit from this policy. They provide secure domestic sources that boost the lithium supply chain.

Nevada is central to this strategy. Its clay deposits are among the largest and best in the U.S. They provide a stable base for domestic lithium production, which supports electrification goals and helps reduce reliance on imports.

Thacker Pass’s progress also sends a signal beyond the Nevada clay sector. It demonstrates that investors and capital markets are willing to back sedimentary clay projects at scale. That validation reduces perceived risk for future projects. It also speeds up permitting and development timelines as well as strengthens valuation metrics.

NNLP, with its superior grade and shallower resource, stands to benefit disproportionately. It is no longer constrained by questions of category viability. It can now be evaluated based on its geological quality, operational efficiency, and potential returns.

NNLP’s advantages, combined with the category de-risking effect of Thacker Pass, position it as a next-generation investment opportunity in Nevada’s clay lithium space.

Looking Ahead: Domestic Lithium’s Role in Energy Transition

Lithium demand is set to grow rapidly as electric vehicles, battery storage, and renewable systems expand. Securing a high-quality, domestic supply is critical to maintaining U.S. leadership in clean energy technology.

Thacker Pass proves that commercial-scale sedimentary clay lithium is achievable. NNLP demonstrates the potential for even higher efficiency and superior economics within the same category. Together, these projects show how local resources can support the energy transition while providing compelling investment opportunities.

NNLP’s higher grades, near-surface mineralization, low strip ratio, and competitive OPEX position it as a leading asset within a now-validated category.

For NILI investors, the message is clear: the clay lithium category is no longer theoretical, and NNLP is positioned to capitalize on the proof-of-concept success. The best news of the year is here—and it’s grounded in both science and strategy.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Slump")

Race to Net Zero Gains Speed as Emissions Fall 35%: Can It Really Reach the Finish Line?")