Disseminated on behalf of Alaska Energy Metals Corporation.

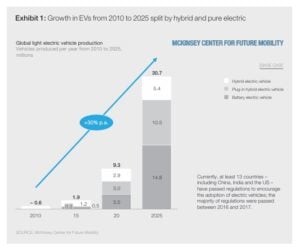

The electric vehicle (EV) revolution is unfolding at full speed. EV sales, battery factories, and electrification plans are all increasing rapidly across the world. But behind this clean‑energy success story lies a growing risk that few people fully grasp: the supply of high‑purity nickel — known as Class 1 nickel — is under increasing strain.

While overall nickel output appears large, the specific kind of nickel that powers EV batteries is far harder to secure. Add in rising geopolitical tensions and energy price shocks, and the result is a supply chain that is both fragile and critical.

Nickel’s Role in the EV Revolution

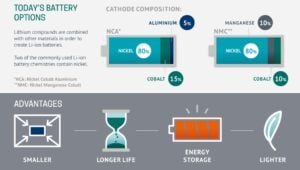

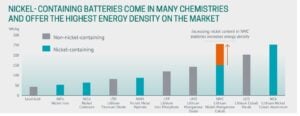

Nickel is a key ingredient in the lithium‑ion batteries that power most long‑range electric vehicles. Modern battery chemistries like NMC (Nickel‑Manganese‑Cobalt) and NCA (Nickel‑Cobalt‑Aluminum) use large amounts of nickel because it improves energy density, which helps EVs travel farther on a single charge.

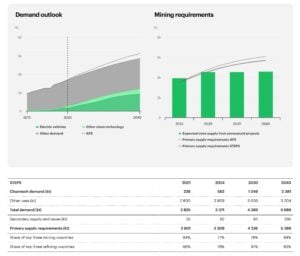

- As a result, demand for nickel from EV batteries is soaring. IRENA data suggested that global demand for nickel used in EV batteries could reach more than 1.09 million tonnes by 2030 under current trends, depending on battery technology and adoption rates.

As per analysts and industry pundits, as EV markets grow across the U.S., Europe, China, and other regions, this nickel demand is only expected to rise further. What makes this particularly challenging is that EV battery producers only accept Class 1 nickel — nickel that is at least 99.8% pure and suitable for conversion into nickel sulfate, which is essential for battery cathodes.

Why Class 1 Nickel Is Scarce

On the surface, the global nickel supply seems large. Countries like Indonesia have rapidly increased production, and numerous mines operate in Asia, Russia, and Latin America. But most of this nickel is Class 2, a lower‑purity type used mainly in stainless steel production, which cannot easily or cheaply be turned into battery‑grade material.

This means the world may have enough nickel in total, but the kind that matters most to the EV industry is limited. This structural imbalance between total output and battery‑grade supply is now one of the EV sector’s biggest supply challenges.

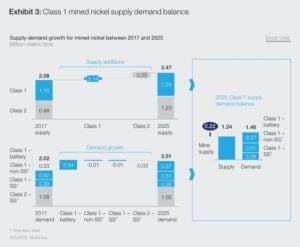

According to McKinsey, Class 1 supply growth is lagging demand growth. Some analysts project that even by 2025, primary Class 1 capacity may only supply around 1.2 million tonnes, compared with demand closer to 1.5 million tonnes, indicating a shortfall right when EV adoption accelerates.

- MUST SEE: The Ultimate Guide to Nickel: Supply, Demand, and Nickel Prices for 2026 and Beyond

- CHECK: LIVE NICKEL PRICES

Global Conflict Adds Supply Risk

Geopolitics is also heightening uncertainty. Russia, historically one of the largest producers of high‑grade nickel, saw its exports disrupted after the Ukraine war began. Sanctions and shifting trade relationships have forced automakers and battery makers to look for alternatives.

Meanwhile, an analysis from S&P Global explained how instability in the Middle East may not directly affect nickel mining, but it does influence everything from energy costs to shipping routes. Critical passages like the Strait of Hormuz handle significant volumes of global oil and gas. Any disruption there can increase fuel prices, which raises costs throughout the mining, refining, and logistics chain.

Since nickel production and refining are energy‑intensive, rising energy costs feed directly into higher production costs. In this way, even conflict far from nickel mines can tighten the Class 1 supply chain.

Processing Bottlenecks Drive Hidden Risk

Another often overlooked factor is processing. Much of the world’s nickel comes from lateritic ores, especially in Indonesia and the Philippines. To turn these ores into battery‑ready nickel sulfate requires a complex High‑Pressure Acid Leach (HPAL) process that depends heavily on sulfuric acid and stable energy inputs.

Disruptions to sulfur supply — linked closely to global energy markets — can slow down or increase the cost of HPAL operations. Analysts have highlighted that future price swings in battery‑grade nickel could be driven not just by ore availability but by these processing input risks tied to sulfur and acid supply.

So even if mines produce enough nickel ore, the ability to convert it into usable battery material can become the real bottleneck.

A Two‑Tier Nickel Market

As a result of these pressures, the nickel world is dividing into a clear two‑tier market:

- A surplus of lower‑grade Class 2 nickel

- A shortage of high‑purity Class 1 nickel demanded by EV makers

This gap is expected to grow as EV battery demand rises more sharply than Class 1 production capacity. Data from IEA shows that demand for nickel in cleantech applications, mainly EVs, could more than double from around 560 kilotonnes in the early 2020s to over 1,349 kilotonnes by 2030.

Yet most new refining capacity is focused on processing laterite ores, and planned Class 1 expansions are relatively limited. This makes high‑purity nickel increasingly strategic.

Tight Battery Nickel Amid Shifting Market Trends

The same S&P report has emphasized this imbalance as a core structural challenge in the nickel market. While overall nickel supply may at times appear ample, the availability of battery‑grade nickel remains tight and vulnerable to both demand shifts and supply disruptions.

Furthermore, tracking the broader nickel market trends showed that industrial demand dynamics and tariff uncertainty have at times weighed on prices, even as battery‑grade demand continues to grow.

This mixed picture of soft prices amid growing strategic demand underscores how complicated the nickel supply story has become.

The Rising Value of Sulphide Nickel in North America

Not all nickel sources are equal. Sulphide nickel deposits — found in places like parts of Canada, Australia, and Alaska — are much easier to process into high‑purity Class 1 material than laterites. They also tend to have lower emissions and simpler refining paths.

Not all nickel sources are equal. Sulphide nickel deposits found in places like parts of Canada, Australia, and Alaska are much easier to process into high‑purity Class 1 material than laterites. They also tend to have lower emissions and simpler refining paths.

However, sulphide deposits are rare compared with laterite ores. Most of the easy‑to‑develop sulphide assets have already been mined. Discoveries are limited, making existing and new sulphide projects more strategically valuable.

This is why automakers and governments in Western countries are placing greater attention on domestic and North American projects as they seek to reduce reliance on geopolitically sensitive supply chains.

Alaska Energy Metals’ Nikolai Project and Cleaner Supply Chains

A high‑profile case is the Nikolai project in Alaska, developed by Alaska Energy Metals Corporation or AEMC. It contains not just nickel but also copper, cobalt, and platinum group metals — all important for EV batteries and broader clean energy technologies.

Projects like this offer several key advantages:

- Cleaner processing pathways

- Simpler conversion to battery‑grade nickel

- Stronger environmental, social, and governance (ESG) transparency

As of March 10, 2025, the nickel junior shows a major increase in contained metals. The resource estimate also confirms the presence of a treasure trove of energy transition metals: copper, cobalt, platinum, and palladium.

- The Indicated category now includes 5.6 billion pounds of nickel and 1.77 billion pounds of copper, and along with the value of the other metals equal to 11.03 billion pounds of nickel equivalent metal. This marks a 46% increase from the previous estimate.

- The Inferred category holds 9.38 billion pounds of nickel and 2.43 billion pounds of copper, and along with the value of the other metals equal to 17.98 billion pounds of nickel equivalent metal. This represents a sharp 122% increase, highlighting the scale of new resource growth.

As automakers push to decarbonize their supply chains, these attributes are becoming more valuable, not just economically but also in regulatory and brand terms.

Friendshoring and Supply Security

The concept of “friendshoring” — sourcing critical materials from politically stable and allied regions — is gaining traction. Governments in the U.S., Europe, and elsewhere are funding and incentivizing projects that can produce strategic minerals like nickel in safer jurisdictions.

This shift aligns with national security goals as well as corporate sustainability targets. Securing battery metals in friendly regions helps reduce exposure to conflicts and sanctions while supporting long‑term industrial planning.

Outlook: Quality Over Quantity

In the early days of the EV transition, the focus was simply on increasing battery production. Today, the conversation has shifted. It is no longer enough for the world to produce more nickel — it must produce the right kind of nickel.

High‑purity, battery‑grade nickel is becoming one of the most strategic materials in the energy transition. Its supply chain is deeply influenced by geopolitics, processing challenges, and shifting industrial priorities.

Conflicts like the Russia‑Ukraine war, energy price shocks, and sulfur supply vulnerabilities have all shown how fragile the nickel ecosystem can be. At the same time, demand projections through 2030 make it clear that EV adoption will continue pushing nickel demand higher.

DISCLAIMER New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals Corp. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.