Disseminated on behalf of Alaska Energy Metals Corporation

Nickel prices have recently climbed to their highest level in nearly two years, driven by supply cuts in Indonesia and growing pressure on global raw materials. The rally highlights how policy decisions in one country can reshape the global market for a critical battery metal.

Nickel futures recently pushed higher, hitting a major peak of $19,587 on May 6. This marks the highest price level for the metal since mid-2024. While the market has since balanced out a bit, prices as of June 4, 2026, are holding steady around $18,800 per tonne. This slight drop shows that even though the market is still very high compared to last year, supply constraints are causing short-term price adjustments.

The surge comes as Indonesia, the world’s largest nickel producer, tightens mining quotas. The move is limiting supply and raising concerns across industries that depend on nickel, including electric vehicles (EVs), stainless steel, and energy storage.

Nickel Price

- CHECK OUT: LIVE NICKEL PRICES

Indonesia Tightens Supply, Driving Price Rally

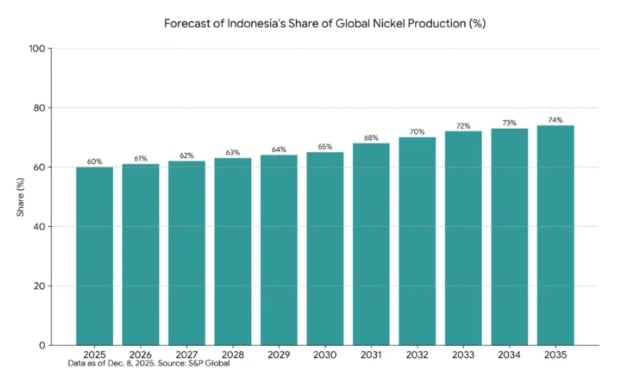

Indonesia plays a dominant role in the nickel market. The country accounts for roughly 50% to two-thirds of global nickel supply, making its policies a major price driver. However, this year, the country reduced its nickel production quota to around 260–270 million tonnes, down from 379 million tonnes in 2025.

This represents a sharp cut of more than 100 million tonnes, or roughly a 30%–34% reduction in output.

The goal is to support higher prices, conserve high-grade ore reserves, and align mining output with domestic processing capacity.

These changes are already tightening supply. Nickel ore shortages are pushing up costs for producers, especially in Indonesia’s nickel pig iron (NPI) and battery-grade materials sectors.

At the same time, disruptions in sulfur supply—a key input for nickel processing—are adding further pressure. This combination is tightening the global supply chain.

Nickel Prices Climb as Supply Risks Grow

The impact on prices has been immediate.

Nickel prices have:

- Risen by about 10% in recent weeks

- Increased by more than 22% year-on-year

- Reached levels close to $20,000 per tonne

This rally reflects both short-term supply disruptions and longer-term structural changes in the market.

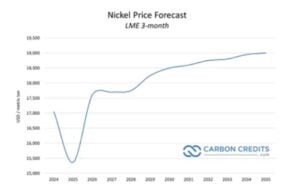

Analysts expect nickel prices to remain supported in 2026. Research firm BMI raised its average price forecast to around $16,600 per tonne, up from earlier estimates.

Meanwhile, Goldman Sachs has projected prices closer to $17,200 per tonne on average, reflecting tighter supply conditions. However, there is still uncertainty. Some forecasts show a continued global surplus of nickel, which could limit how high prices can go.

- MORE DETAILS: Nickel Prices Hit $18,000 in 2026 Amid Global Oversupply, US Boosts Domestic Supply Chain

EV Demand and Energy Transition Drive Long-Term Growth

Nickel is a key material for the global energy transition.

It is widely used in:

- Electric vehicle batteries (especially high-nickel chemistries)

- Stainless steel production

- Renewable energy storage systems

Demand from EVs is a major growth driver. High-nickel batteries offer higher energy density, which allows a longer driving range.

Global EV sales continue to rise, and battery demand is expected to grow strongly through 2030. This is increasing pressure on nickel supply chains. At the same time, governments and companies are investing heavily in clean energy technologies. This is further boosting demand for battery metals.

However, there are also shifts in technology. Some EV makers are moving toward lithium iron phosphate (LFP) batteries, which use less or no nickel. This could slow demand growth in some segments.

ESG Pressure Reshapes Nickel Production

Nickel production is facing rising environmental and ESG scrutiny. Mining and processing nickel can have significant environmental impacts, including high energy use, land degradation, waste generation, and processing emissions.

Indonesia’s policy changes are partly aimed at improving control over the industry. The government wants to reduce environmentally harmful practices and increase domestic value-added processing.

At the same time, global buyers are under pressure to source “cleaner” nickel. And major mining companies and battery producers are now:

- Setting net-zero targets

- Investing in lower-carbon processing technologies

- Improving traceability in supply chains

Some companies are also developing new projects outside Indonesia to diversify supply and reduce geopolitical risk.

Alaska Energy Metals (AEMC) Adds Strategic Supply Diversification Angle

Amid tightening supply from Indonesia, companies like Alaska Energy Metals are gaining attention as potential alternative sources of critical minerals. The company is advancing its flagship Nikolai nickel project in Alaska, which hosts a large-scale polymetallic resource including nickel, copper, cobalt, and platinum group elements.

This project is strategically important for the United States as it looks to reduce reliance on foreign supply chains, particularly for battery metals dominated by Indonesia and China. AEMC is positioning itself as part of a broader push to build a domestic critical minerals ecosystem that supports EV manufacturing and clean energy goals.

The company has also been involved in initiatives such as the Minerals for National Automotive Competitiveness (MINAC), which promotes responsible development of U.S. mineral resources. This aligns with growing policy support for reshoring supply chains and securing raw materials for the energy transition.

While still in the development stage, projects like Nikolai could play a meaningful role in balancing future supply-demand dynamics. As global markets face volatility and geopolitical risks, new sources of nickel outside dominant regions may help stabilize long-term pricing and availability.

Market Outlook: Tight Supply vs Structural Uncertainty

The nickel market is entering a new phase. On one hand, supply is tightening due to:

- Indonesia’s production cuts

- Higher input costs (such as sulfur)

- Policy-driven constraints

On the other hand, long-term uncertainty remains:

- A projected global surplus of over 200,000 tonnes in 2026

- Rapid growth in Indonesian refining capacity

- Shifts in battery technology away from nickel

Some projections suggest that new high-pressure acid leach (HPAL) projects could add up to 600,000 tonnes of refined nickel supply by 2026, potentially pressuring prices later.

This creates a mixed outlook. Prices may stay high in the short term, but are likely to be volatile over time. And therefore, for investors and industry players, the key takeaway is clear: supply diversification and strategic positioning—both within and outside dominant producers like Indonesia—will define the next phase of the global nickel market.

- ALSO READ:

- AEMC’s Nikolai: America’s Answer to Indonesia’s Nickel Crunch

- Why Investors See a High-Upside Catalyst Pipeline Building for Alaska Energy Metals Corporation

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.