Disseminated on behalf of Surge Battery Metals

The lithium market is shifting again. After a period of oversupply and price weakness, new disruptions are tightening supply in real time.

Two developments are driving this change: regulatory action in China and export restrictions in Zimbabwe. Together, they are bringing the lithium deficit narrative back into focus and reshaping how supply risk is assessed.

A New Supply Shock Emerges

In early 2026, Zimbabwe, Africa’s top lithium producer, suspended exports of lithium concentrates and other unprocessed minerals. The government cited malpractices and revenue leakages as the reason for the halt.

Now, exports are set to resume under tighter controls. According to Reuters, Zimbabwe will introduce export quotas and require mining companies to commit to local processing investments.

Key measures include:

- Export quotas assigned to individual producers

- A continued 10% export tax on lithium concentrates

- A requirement to build local processing capacity before January 2027, when a full ban on concentrate exports is expected

Zimbabwe is a major player in the global supply chain. In 2025, the country sent 1.128 million metric tons of lithium-bearing spodumene concentrate to China. This made up about 15% of China’s imports.

Any disruption at that scale has an immediate global impact.

China Tightening Adds Pressure

At the same time, China is tightening its control over domestic lithium production. Industry reports from S&P Global Commodity Insights and Fastmarkets show that permit reviews and stricter environmental rules have impacted some operations. This is especially true for smaller or higher-cost mines.

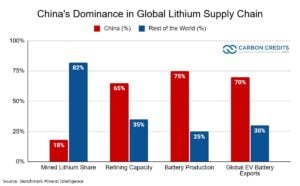

China dominates global lithium processing and refining. When domestic supply slows or becomes less predictable, it affects the entire supply chain. This includes chemical conversion capacity, which is critical for producing battery-grade lithium.

Together, these developments are creating a short-term tightening effect in the market. Supply is becoming less flexible just as demand continues to grow.

Small Disruptions, Big Price Impacts

Lithium markets are highly sensitive to supply changes. Even small disruptions can affect pricing and availability.

The current situation highlights several key dynamics:

- Supply is still concentrated in a few regions

- Policy decisions can quickly impact global availability

- Processing capacity is as important as raw material supply

Zimbabwe’s push for local processing reflects a broader trend. Resource-rich countries are seeking more value from their minerals instead of exporting raw materials. While this may support long-term development, it can reduce short-term supply to global markets.

At the same time, China’s role as the dominant processor means that changes within its domestic system ripple outward. This combination of upstream and downstream pressure is what makes the current situation notable.

From Glut to Squeeze in Just One Year

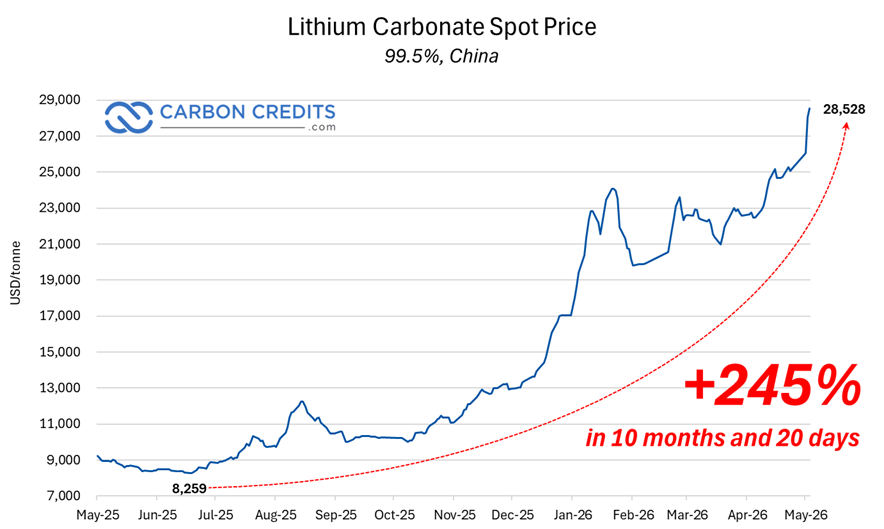

Just a year ago, lithium prices were under pressure. The market saw oversupply, driven by strong production growth and slower-than-expected EV demand in some regions.

Lithium prices fell to $8,259 per tonne in June 2025, before reaching $28,528 per tonne on May 8, 2026, representing a 245% increase in under a year.

Now, supply-side disruptions are shifting sentiment again. While the market is not yet in a severe deficit, the balance is tightening.

This shift reinforces a key point: lithium markets can move swiftly. Oversupply can quickly lead to tighter conditions, especially with policy and geopolitics at play.

Lithium Becomes a Strategic Battleground

The current supply story is not just about mining. It is about geopolitics and control over critical materials.

Zimbabwe’s lithium sector is heavily influenced by Chinese companies, including major operators that dominate production and processing investments.

One of the biggest players is Zhejiang Huayou Cobalt, which operates the Arcadia lithium project and runs both mining and processing facilities. Sinomine Resource Group is another major operator, managing the Bikita lithium mine and expanding processing capacity.

Chengxin Lithium Group is also active in mining and processing, while Yahua (Sichuan Yahua Industrial Group) is building lithium sulfate plants in the country. Even Tsingshan Holding Group has invested in Zimbabwe’s lithium projects. Together, these companies dominate the industry and shape how the country’s lithium resources are developed.

This creates a concentrated supply chain, where decisions in one country can affect availability in another. For governments and industry players, this raises concerns about the security of supply.

As a result, there is an increasing focus on diversification and domestic sourcing. Countries want to rely less on single regions or supply chains. This is especially true for materials needed for energy transition and tech infrastructure.

U.S. Domestic Projects Gain Strategic Edge

These global disruptions are highlighting the value of stable, domestic lithium resources. Projects located in secure jurisdictions are becoming more important as supply risks increase across regions like Africa and parts of Asia.

In the United States, Nevada stands out as a key lithium hub. It offers scale, infrastructure, and a well-established mining framework. Within this context, Surge Battery Metals’ (TSX-V: NILI | OTCQX: NILIF) Nevada North Lithium Project (NNLP) provides a clear example of how domestic supply can align with evolving market needs.

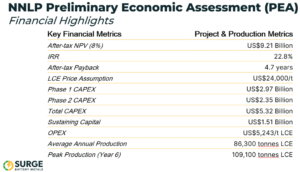

NNLP is not just defined by location, but by scale and economics. The 2025 Preliminary Economic Assessment shows a 42-year mine life, with estimated average annual production at around 86,300 tonnes of lithium carbonate equivalent (LCE). It is expected to produce around 3.6 million tonnes of battery-grade LCE over its lifetime. This positions it as one of the longer-lasting lithium supply assets in North America.

The project is also supported by a large resource base. Current estimates point to more than 11 million tonnes of lithium carbonate equivalent (inferred resource), with mineralization extending across a broad, near-surface footprint. This near-surface shape allows for a regular open-pit mining method. This can make development easier and boost efficiency in operations over time.

Grade is another key factor. NNLP reports an average lithium grade of around 3,010 ppm, with some zones exceeding 4,000 ppm. This positions the project among the higher-grade clay lithium resources in the United States. Higher grades can lead to better recovery efficiency. They also lower processing intensity per tonne, which matters in a cost-sensitive commodity market.

From an economic perspective, the project shows strong baseline metrics. Surge Battery Metals’ PEA shows an after-tax net present value of about $9.2 billion. It also indicates an internal rate of return of 22.8%, based on a lithium price assumption of $24,000 per tonne. The estimated operating cost is around $5,243 per tonne LCE, supporting its positioning as a potential low-cost producer.

Additional factors reinforcing NNLP’s relevance in the market:

- Large-scale footprint, with mineralization extending over more than 4 km of strike length

- Open-pit design, targeting shallow, high-grade zones in early production phases

- Two-phase development plan, allowing production to scale over time

- Domestic processing pathway, supporting U.S. supply chain goals

Together, these characteristics position NNLP as a long-duration, scalable lithium source. It aligns with the needs of various demand drivers, including EVs, grid storage, and industrial applications.

In a market increasingly shaped by geopolitical risk, projects like NNLP represent more than just supply. They offer jurisdictional stability, long-term visibility, and alignment with domestic sourcing strategies.

These attributes are key to evaluating lithium assets as supply disruptions continue to emerge globally.

The New Reality: Volatility, Policy, and Power

The lithium market is entering a new phase. Demand is expanding, driven by EVs, grid storage, and data center infrastructure. At the same time, supply is becoming more complex and more sensitive to policy decisions.

The recent actions in China and Zimbabwe show how quickly the balance can shift. They also highlight the importance of diversification, transparency, and long-term planning in lithium supply chains.

For investors and industry participants, the takeaway is clear: The lithium deficit narrative is returning, not just because of demand growth, but because of real-world supply constraints.

In this environment, projects that offer scale, longevity, and jurisdictional stability are likely to play a larger role in meeting future demand.

- READ MORE: Surge Battery Metals Strengthens Nevada North With High-Grade Expansion and Infill Success

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.