The voluntary carbon market (VCM) has been a significant tool for companies to achieve net zero, with carbon credits playing a key role.

To fully appreciate the implications of the sudden downturn in prices, particularly in NGEO (Nature-Based Global Emissions Offsets) prices, it’s essential to understand the differences between the various types of carbon offsets available in the voluntary market.

In this market, three primary types of offsets are traded – NGEO, GEO (General Emissions Offsets), and CGEO (Certified Global Emissions Offsets).

- NGEOs are carbon credits generated by projects that reduce, remove, or prevent carbon emissions through nature-based solutions. Examples include forest conservation or restoration projects that sequester carbon in trees and soil, or agricultural practices that reduce emissions or enhance carbon storage.

- GEOs, on the other hand, represent a broader category of offsets that might include nature-based solutions. But they also include renewable energy projects, methane capture from landfills, or energy efficiency initiatives.

- Lastly, CGEOs are a type of carbon offset that is third-party verified to certain standards. This verification offers an extra layer of assurance to buyers about the quality and legitimacy of the emission reductions.

Note: You can find up-to-date carbon prices right here.

The Never-Ending Cliff: Voluntary Market Carbon Prices in 2023

In the voluntary carbon market, nature-based solutions such as those represented by NGEOs have been highly valued. They often trade at a premium due to the additional co-benefits they bring, like biodiversity protection and local community development.

While the prices of all voluntary market carbon offsets – NGEO, GEO, and CGEO – have taken a beating, the decline in NGEO prices stands out due to the premium they were trading at over the other offsets last year.

While the prices of all voluntary market carbon offsets – NGEO, GEO, and CGEO – have taken a beating, the decline in NGEO prices stands out due to the premium they were trading at over the other offsets last year.

Nature-based carbon and biodiversity credits offer significant benefits that technology-based or other carbon credits can’t provide.

There’s a reason why nature-based solutions are the largest segment of the voluntary carbon markets, accounting for 45% of all credits last year.

Reasons Behind Carbon Price Drops This Year

There were several reasons behind this sudden drop in carbon offset prices.

One of the main catalysts behind this downward trend was the tough macroeconomic environment, which led to stagnation on the demand side in late 2022.

According to the latest Google Sustainability Survey of 1,476 top-level executives at global organizations, 33% of executives reported cuts in their sustainability initiatives due to economic conditions.

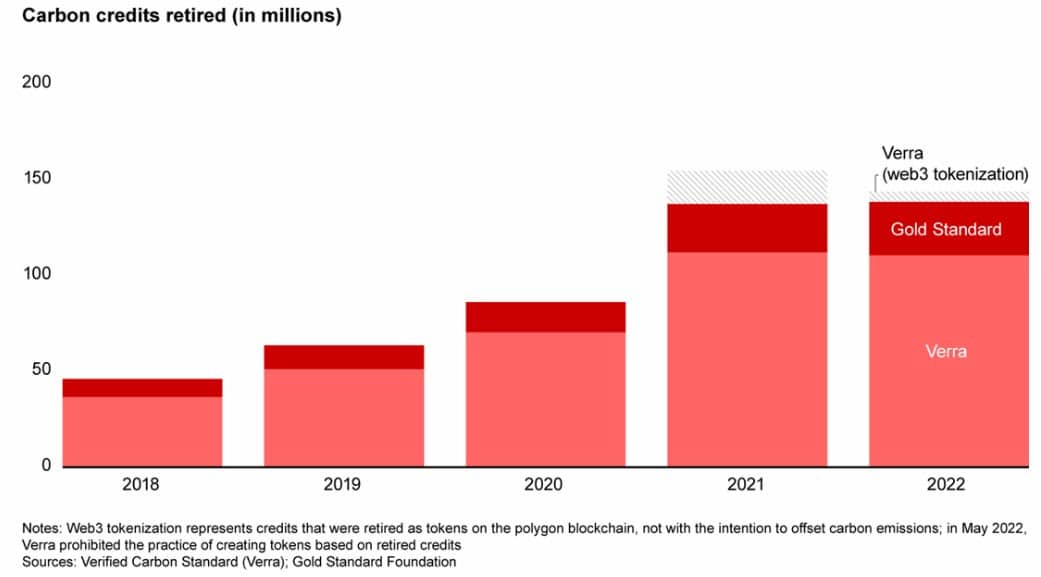

As a result, credit retirements were flat for the first time in five years:

Another source of downward pressure on carbon prices was the poor outcome for the voluntary carbon markets at COP27.

While there’s some progress on Article 6, the conference failed to fully iron out the details of the intergovernmental carbon credit trading system that the Paris Agreement sets out.

This lack of progress has led to some uncertainty from corporations regarding the quality and integrity of credits on the markets. It also brought doubts on the acceptable proportion of carbon offset credits in their net zero plans.

Finally, increased public and media scrutiny – particularly, claims of “greenwashing” and the growing countertrend of “greenhushing” – continue to discourage corporations from decisive action on their decarbonization initiatives.

Combined, all these factors together have led to sustained downward price pressure on carbon credit prices well into 2023.

How Carbon Pricing Affected Stocks and Companies

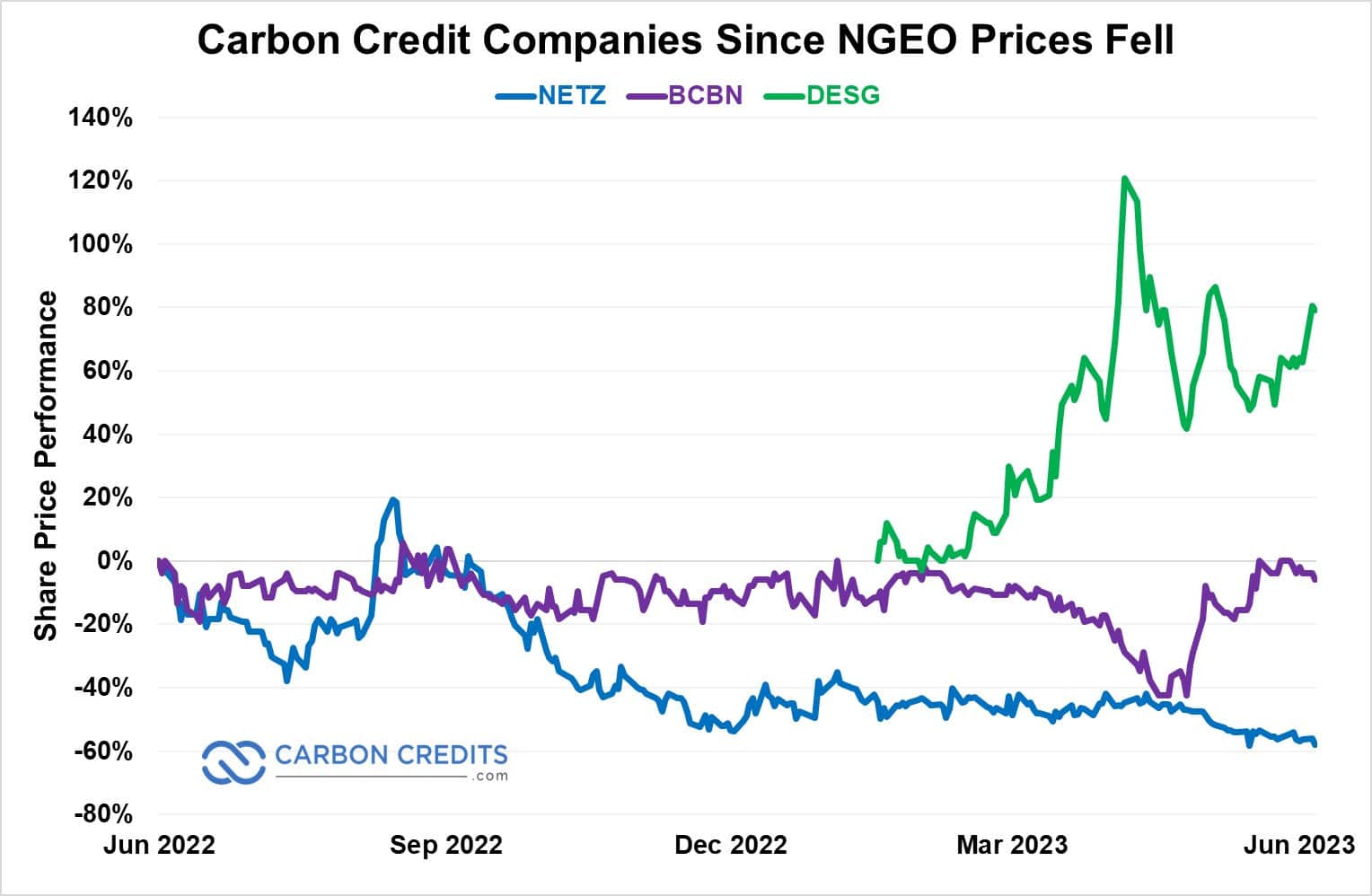

This unexpected downturn has sent ripples throughout the carbon market, affecting companies such as Carbon Streaming and Base Carbon.

Carbon Streaming Corporation, an early mover in the carbon credit space, was hit particularly hard. Its stock prices were declining in the wake of the NGEO price drop.

The firm’s diverse portfolio of 21 projects in 12 different countries. These include the Rimba Raya Biodiversity Project in Indonesia, couldn’t shield it from the market-wide effects.

Similarly, Base Carbon, a firm involved in financing carbon projects, has experienced setbacks due to the price collapse.

The company had committed USD $29.6 million for projects in Rwanda and Vietnam. They, too, now face uncertainty in the wake of falling carbon prices.

On the other hand, DevvStream, a more recently listed company providing funds for green projects in exchange for carbon credit rights, hasn’t felt the repercussions as hard.

Its innovative use of a blockchain-based ESG platform and ambitious plans to manage and track carbon credits has allowed it to combat falling carbon credit prices on a better footing.

This unforeseen collapse in NGEO prices underscores the volatility of the carbon market and the inherent risks involved. However, it also highlights the need for sustainable practices in carbon credit production to prevent future oversupply.

As the world grapples with the urgent need to reduce GHG emissions, the role of the VCM remains crucial.

Yet, this market upheaval reminds us that achieving a sustainable, low-carbon economy involves navigating a complex landscape.

Moving forward, much more work needs to be done to fully scale up the VCMs. This is a crucial topic for the upcoming COP28 conference in Dubai in November.

Some organizations such as SBTI, ICVCM, and VCI are all helping to shore up the foundation for the voluntary markets. Yet, reconciling the current VCMs with the Paris Agreement will go a long way towards stabilizing the market for carbon offset credits.

In the meantime, it’s likely that we’ll continue to see headwinds for NGEO prices.