Companies operating in the European Union will have to deal with new non-financial and sustainability reporting requirements starting January 2024 with the EU’s Corporate Sustainability Reporting Directive (CSRD).

The CSRD advancement shows a change in how governments are regarding the reporting of Environmental, Social and Governance (ESG) data, which include a company’s carbon emissions.

ESG reporting is crucial in helping stakeholders, particularly investors, evaluate the risk of their investments by knowing the company’s impact on the people and the planet. It also helps them understand how climate change disasters can impact the business. Robust sustainability reporting is also vital in establishing trust and enhancing a company’s reputation.

In the U.S., the Securities and Exchange Commission is busy fine-tuning its own climate disclosure regulations. This new climate rule, which will get finalized this fall, requires companies to report climate risk for the first time.

What is the EU CSRD and Its Objectives?

The CSRD, which came into effect in January, is a significant expansion of the required sustainability or ESG reporting. In July this year, the European Commission adopted the first of the European Sustainability Reporting Standards (ESRS) for entities subject to the CSRD.

The ESRSs are now under a 2-month scrutiny period during which the EU Council and the EP will deliberate it for approval (or rejection). Once approved, it will replace the current Non-Financial Reporting Directive (NFRD) framework.

CSRD aims to improve the quality of sustainability reporting throughout the region, both for EU and non-EU businesses. It will replace the existing reporting framework and broaden the scope of companies covered, from 11,000 initially to now 50,000.

Businesses earning $166 million or €150 million a year and have listed securities on the bloc’s regulated market fall under the Corporate Sustainability Reporting Directive scope.

From 2024 onwards, the new directive will extend the scope of the EU taxonomy and mandate disclosure against ESG indicators.

Objectives of the CSRD:

The CSRD will help channel capital flows into sustainable businesses, playing a critical role in the region’s Sustainable Finance Strategy. This is essential to ensure that the European Green Deal goals are achievable, particularly:

- Reduce net GHG emissions by at least 55% by 2030 versus 1990 levels

- Reach climate neutrality by 2050 (net zero emissions)

Meeting these targets are possible only if financiers have access to sufficient information on the company’s sustainability data and performance. Only by having enough information that they can decide accordingly and invest in sustainable businesses, which the CSRD will provide.

The binding framework creates a comprehensive, transparent, and uniform reporting for the companies in the EU. Developing the directive has been informed by international references, such as the TCFD, CDP and the EU taxonomy.

The EU taxonomy is key in promoting investments in sustainable activities to enable the region to achieve net zero targets. It allows the sustainability assessment of economic activities that represent over 93% of GHG emissions in the bloc.

Failure to comply with the new reporting framework will lead to significant fines.

CSRD Focus and Key Principles

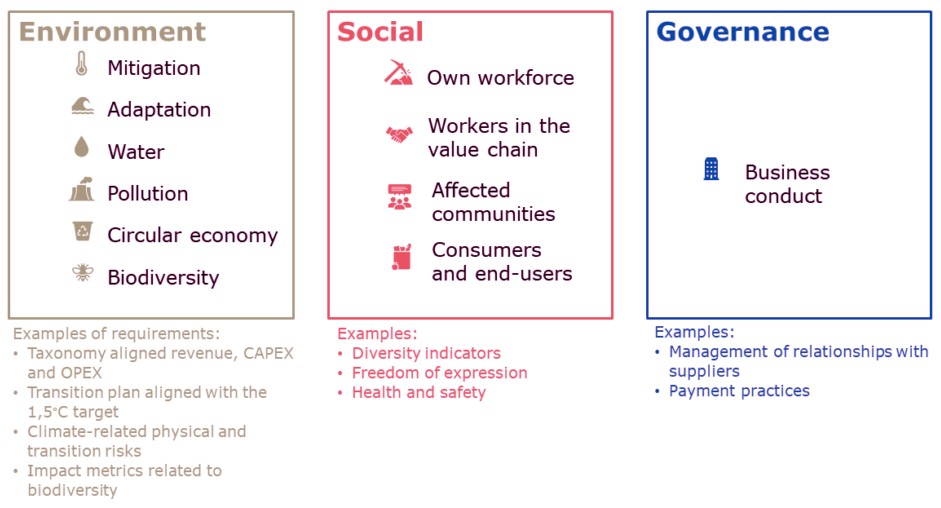

The ESRS are the ESG quantitative and qualitative indicators to report under the new directive. The reporting requirements are breakdown into three major ESG categories:

The major reporting guidelines and principles under the ESRS are the following:

Double materiality: Materiality assessment on topics relating to matters that are either significant for the business (financial) or from ESG (impact).

Scope: Company’s entire value chain.

Time horizon: Qualitative and quantitative information that covers short-term, medium-term, and long-term periods, when necessary.

Due diligence: Procedures for identifying, preventing, mitigating, and accounting for the impacts on the planet and people.

Verification: Must be verified annually by third-party, independent audit firm accredited by each member state.

Who Is Impacted by the CSRD?

The directive will apply to large EU companies, listed or not, and non-EU large companies listed on EU regulated markets. These businesses often have 250+ employees and have a total balance sheet of >€20 million.

EU and non-EU small and medium enterprises (SMEs) listed on the region’s regulated markets are also affected. Micro-enterprises are exempted but small and non-complex credit providers and captive insurance companies are not.

Lastly, the CSRD mandate will also impact large non-EU entities with significant activity in the bloc, with turnover of >€150 million, and have a large branch or subsidiary in the region.

When, Where, And How to Report?

Same with the existing framework, the new directive requires reporting for non-financial information in companies’ annual reports.

The report can be in single consolidated format or in 4 separate sections – general information, Environmental, Social, and Governance. Or companies may also use references from the ESRS guide, for example ESRS E2-5, par. 22.

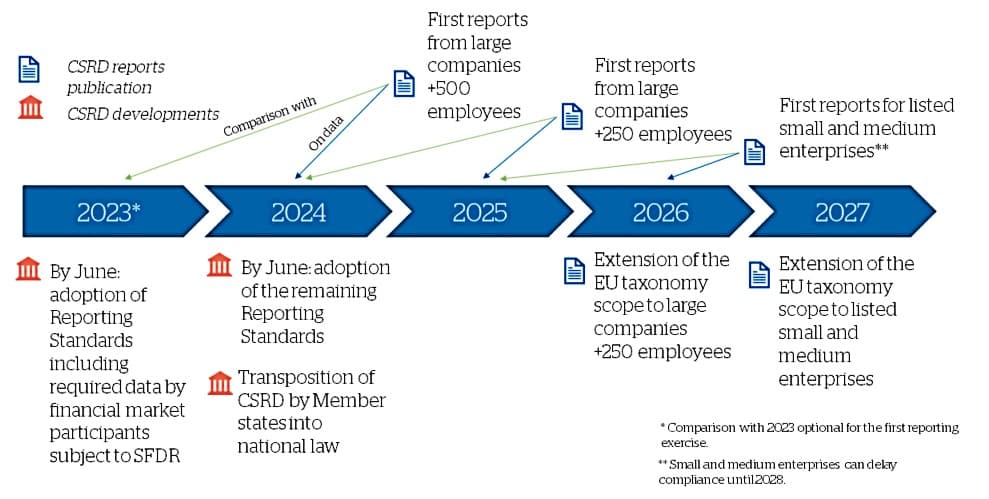

So, the ESG reporting is annual, adhering to the following timeline:

Moreover, a major difference between the existing reporting framework and CSRD is how the information is shared. There are certain digital formats in which CSRD mandates that companies must use to share their reports.

They must also use digital tags so it’s machine-readable under the European Single Access Point (ESAP). Digitalization is important to enhance access to and reuse of the data. ESAP will handle information accessibility, analysis and comparability of these reports.

Finally, companies that have been following the CDP may find it easier to align their reporting with the Corporate Sustainability Reporting Directive. That’s because of the 140 indicators in the new climate change reporting standard, up to 90% align with the CDP Climate Change 2023 Questionnaire.

IN summary, the EU’s Corporate Sustainability Reporting Directive represents a significant shift in ESG reporting, expanding the scope and depth of sustainability disclosures. By providing comprehensive and transparent reporting guidelines, the CSRD aims to channel investments into sustainable businesses, contributing to Europe’s ambitious net zero goals.