Disseminated on behalf of Li-FT Power Ltd.

Lithium has recently experienced a rollercoaster ride, particularly with concerns about the potentially dwindling EV industry. This year, prices hit their lowest point in three years due to growing fears of excessive supply. With shifting trade rules and increased production, the lithium market faces new challenges.

Lithium Price Plunges Amid Oversupply

As of early September, lithium carbonate and lithium hydroxide prices fell below $11,000 per metric ton for the first time since June 2021. Trading Economics reported Lithium carbonate prices remained stable at 10,552.50 per ton in September, marking the lowest level in over three years. Experts predict that global supply could increase by almost 50% this year, adding to the existing oversupply.

A MESSAGE FROM Li-FT POWER LTD.

This content was reviewed and approved by Li-FT Power Ltd. and is being disseminated on behalf of CarbonCredits.com.

Lithium Deposits That Can Be Seen From The Sky

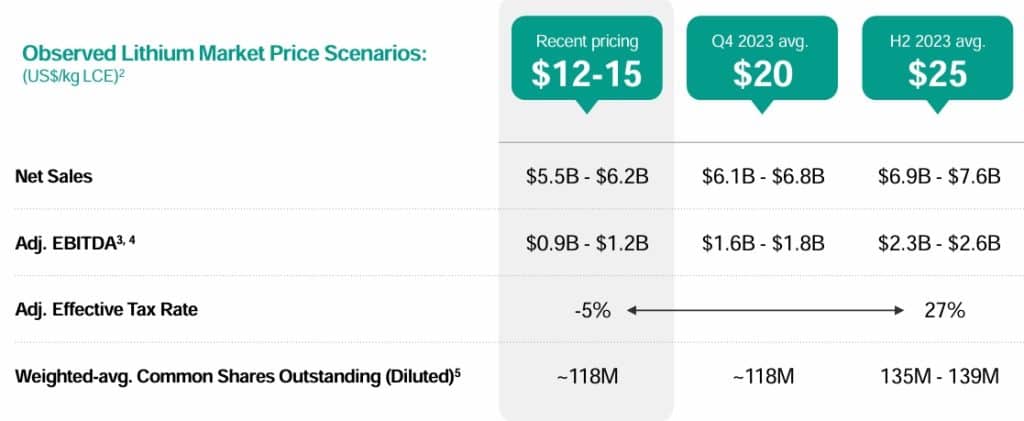

Why Li-FT Power? One of the fastest developing North American lithium juniors is Li-FT Power Ltd (TXSV: LIFT | OTCQX: LIFFF | FRA: WS0) with a flagship Yellowknife Lithium project located in the Northwest Territories. Three reasons to consider Li-FT Power:

RESOURCE POTENTIAL | EXPEDITED STRATEGY | INFRASTRUCTURE

Market Concerns: Oversupply and Low EV Sales

Lithium prices fell after peaking at over $79,637 per ton in December 2022, driven by surging demand for EVs. Despite starting the year near record highs, prices dropped as overcapacity in battery production, particularly lithium iron phosphate (LFP) batteries, began to impact the market. Slowing EV sales, especially in China (accounting for 60% of global EV registrations), added to the downward pressure.

China’s uncertain economic recovery and the phase-out of EV subsidies further dampened demand. According to the IEA, new electric car registrations grew by 35% in 2023, a notable slowdown compared to the 82% growth in 2022. Despite this, experts believe the EV sector will remain a significant driver of lithium, with projections showing it will account for over half of global lithium consumption by 2024.

The IEA forecasts global electric car sales could hit 17 million units by the end of 2024, up from 14 million in 2023. While growth continues to be concentrated in China, Europe, and the US, emerging markets like Vietnam and Thailand are seeing increased EV adoption, with electric cars making up 15% and 10% of sales, respectively.

Market Uncertainty Forces Lithium Giants to Rethink Strategies

Lithium producers are feeling the pinch as oversupply drives prices down. Major players like Albemarle Corp. and Arcadium Lithium PLC have paused expansion plans, while SQM and Ganfeng Lithium Group continue to ramp up production, hoping for a price rebound once the market stabilizes.

Albemarle Adapts to Lithium Market Flux

In July, Albemarle halted expansion plans at its Kemerton lithium hydroxide refinery in Australia to manage costs more effectively. CEO Kent Masters emphasized the need for adaptability in the changing industry landscape. Despite many producers struggling to cover cash costs, the timing for a price recovery remains uncertain.

Albemarle, which reported a $1.96 per share net loss for the second quarter, may shift towards lithium carbonate batteries, potentially influencing future expansion strategies. The company maintains its full-year outlook, reflecting anticipated lithium market price trends.

Source: Albemarle

Source: Albemarle

Ganfeng’s Bold Lithium Move

Ganfeng Lithium Group plans to splash in 2024 with expanded lithium production and increased market presence. The $500 million joint venture with Turkish lead-acid producer Yiğit Akü for lithium batteries adds a significant boost.

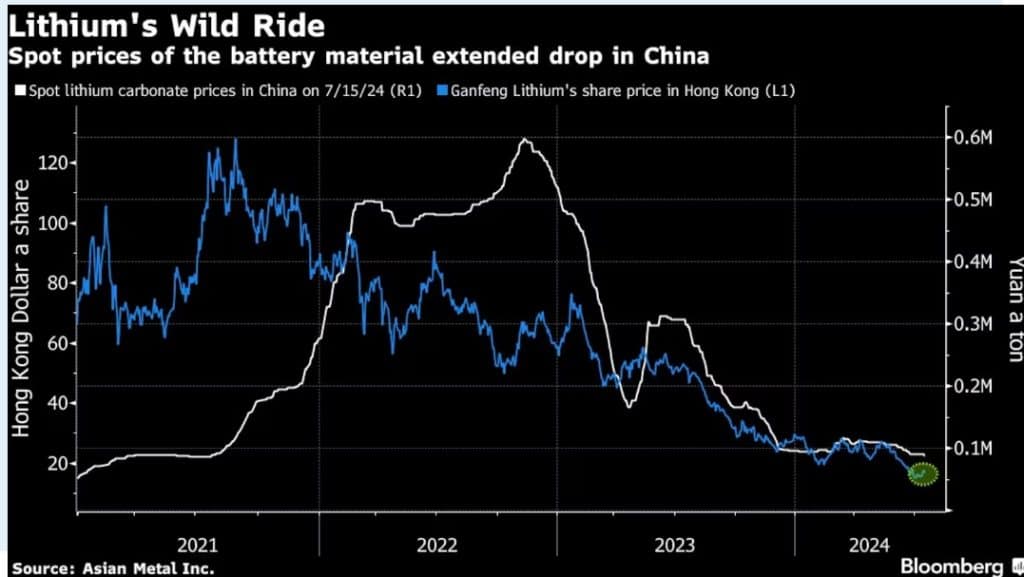

Despite recent stock declines from a peak of HK$132 in 2021 to HK$17.10, Ganfeng continues to expand globally, securing resources in Argentina, Australia, Mali, and Mexico. The company plans to issue five-year overseas bonds worth up to $200 million to fund a project in Argentina. Look out Bloomberg’s chart:

Some More Industry Adjustments

- CATL’s Strategy Shift: UBS analysts predict an 8% drop in China’s lithium carbonate production, potentially balancing supply and boosting prices.

- Arcadium’s Cutbacks: Slowing sales and reduced earnings prompted the pause of its 40K ton spodumene Galaxy project in Canada and scaled-back expansion in Argentina.

- Global Market Tensions: Trade barriers and slow EV demand contribute to price declines, while Chile and China push for increased lithium output to balance the future market.

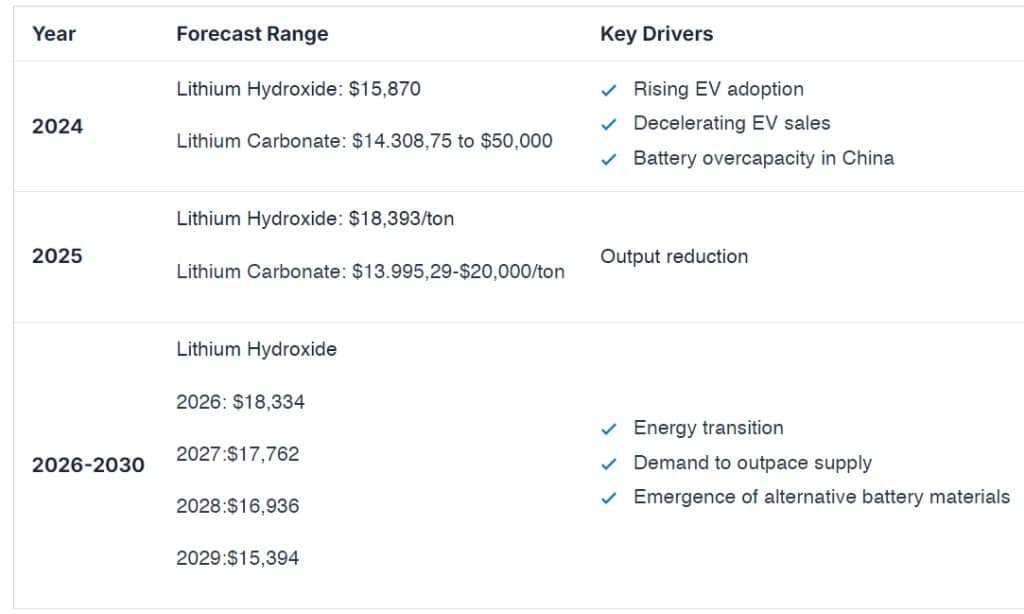

Lithium Price Forecast 2024-2030

Source: Techopedia

Source: Techopedia