The lithium sector took center stage this week when Lithium Americas (NYSE: LAC) stock soared nearly 95% on reports that the Trump administration is considering taking an equity stake in the company’s Thacker Pass mine in Nevada. If it happens, this move would be one of the biggest government actions in U.S. mining in years. It shows how important lithium is to national policy now.

Behind the headlines lies a deeper story: America’s ambition to lead the clean energy transition risks colliding with a stark supply shortage. We highlight below, with the two charts, both the opportunity and the vulnerability facing the United States in this lithium quest.

A Lithium Crisis in the Making

The United States faces a lithium crisis that makes its clean energy ambitions look more like an aspiration than an execution. Current domestic production is only 2,700 metric tons a year. That’s too small compared to the 500,000 tons needed by 2030 to hit electric vehicle (EV) goals.

To put this in perspective:

- The lithium in an iPhone weighs about the same as a penny.

- A Tesla Model 3 battery pack requires around 12 kilograms.

- A Ford F-150 Lightning demands closer to 17 kilograms.

At present mining levels, the U.S. produces enough lithium for only about 158,000 Tesla Model 3s annually. That’s in a market where Americans bought 1.4 million EVs in 2024 alone, with demand expected to climb sharply in the coming years.

This gap reveals a harsh reality: America’s lithium supply chain is ill-prepared for its electrification goals.

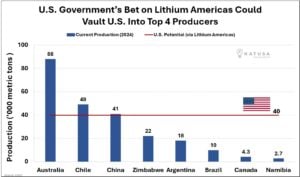

From Marginal Producer to Top Four — If Thacker Pass Delivers

The government’s solution to this issue is projects like Lithium Americas’ Thacker Pass. It’s one of the largest lithium deposits in North America. If fully developed, it could boost U.S. production to around 40,000 tons each year. This would place the country among the top four producers, following Australia, Chile, and China.

That would mark a tenfold increase in output, but it is still far from enough. Even under the most optimistic forecasts, Thacker Pass would meet just 8% of projected U.S. demand by 2030, and a mere 3% of the 1.2 million tons expected by 2035.

Meanwhile, China has spent more than a decade locking up supply chains, securing lithium assets in Africa, South America, and Australia. It is also building refining infrastructure that now processes nearly 80% of the world’s lithium.

The comparison is striking: Zimbabwe produces eight times more lithium than the U.S. Even smaller producers, like Argentina, surpass American output. In this context, Washington’s sudden push for equity stakes is less about profits and more about survival in a high-stakes race for supply.

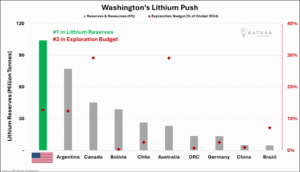

Reserves Rich, Supply Poor: The Untapped U.S. Advantage

The second chart points to America’s hidden strength: the U.S. ranks first globally in lithium reserves, with more than 100 million tonnes identified. Despite this geological advantage, those resources remain largely untapped.

Encouragingly, the U.S. now ranks third in global exploration budgets, reflecting a deliberate policy pivot. Billions of dollars are going to exploration and project development, from Nevada to North Carolina. If even a fraction of these reserves is unlocked, the U.S. could rival today’s top producers and reduce dependence on foreign supply chains.

However, converting reserves into production requires more than exploration. Projects can hit delays with permits, face environmental lawsuits, struggle with financing, and deal with local opposition. All these issues can stretch timelines into decades. This is why federal involvement is becoming more important. This includes equity stakes, subsidies, and fast-tracking permits.

Why the LAC Surge Matters

The near-doubling of Lithium Americas’ stock was not just a speculative rally. It was a market signal that U.S. lithium policy is entering a new phase.

- Government backing reduces financing risk, making it easier to attract institutional investors.

- Aligning policies with EV makers like General Motors, which has a big stake in Thacker Pass, ensures supply security and offtake agreements.

- National security framing places lithium on the same level as oil and gas. This makes lithium a strategic commodity and allows for more state intervention.

For automakers and battery manufacturers, this could mark the start of a more stable domestic supply base. For investors, it highlights how policy can rapidly change the outlook for mining equities.

Demand, Prices, and the Rollercoaster Market

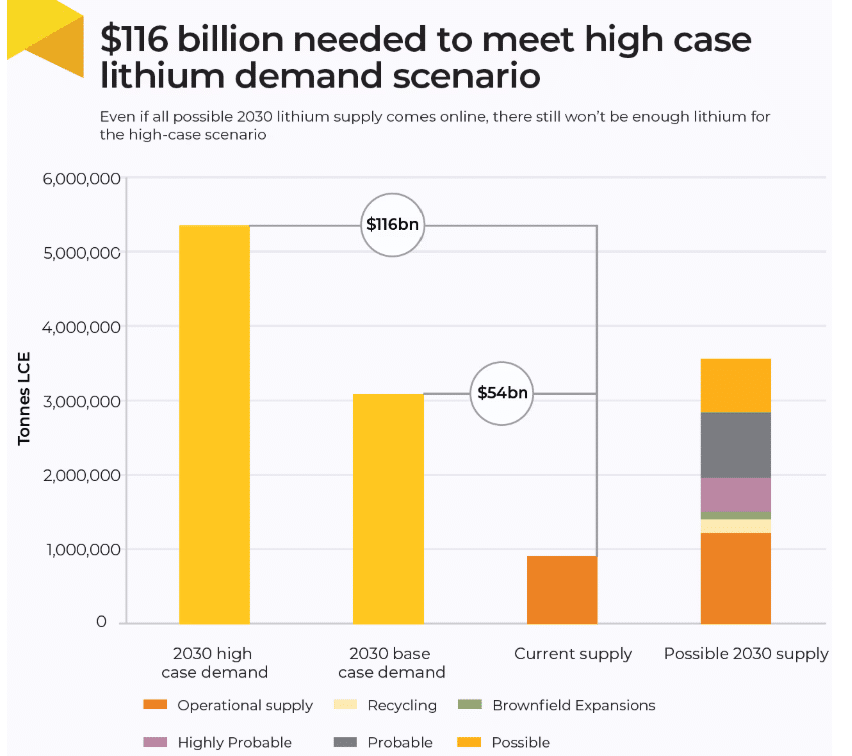

Lithium demand will rise quickly. Benchmark Mineral Intelligence (BMI) predicts that consumption of lithium carbonate equivalent (LCE) will surpass 2.4 million tonnes by 2030. That’s almost four times what we use now. By 2035, demand could climb past 5 million tonnes, fueled by electric vehicles and large-scale battery storage.

The industry needs hundreds of new projects to meet this surge. However, BMI points out that permitting delays, financing issues, and tech challenges are slowing supply growth.

Battery demand adds another layer of urgency. Analysts predict global battery capacity will reach nearly 4 terawatt-hours by 2030. This highlights lithium’s vital role in the clean energy shift.

The U.S. is still a minor player. Most refining and conversion happens in China, which holds about 80% of processing capacity. This imbalance shows why Washington supports projects like Lithium Americas. They want to secure a local supply.

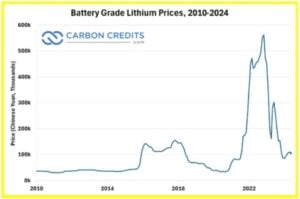

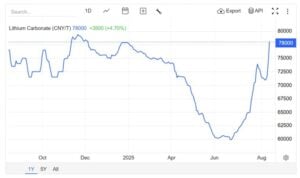

Litium prices, meanwhile, have been highly volatile. After lithium carbonate reached over $80,000 per tonne in late 2022, prices dropped sharply. In 2023–2024, they fell by more than 80%, going below $10,000 earlier this year. BMI attributes the crash to oversupply from South America and weaker near-term EV sales in China, which created a temporary glut.

However, the consultancy stresses that volatility is cyclical, not structural. Demand is strong, and prices should bounce back. In fact, last August, prices climbed when China’s major battery player closed its major mine.

New supply can’t keep up with long-term consumption. BMI warns that without steady investment and diversification of supply, future shortages could push prices sharply higher again by the late 2020s.

For the U.S., this shows why public investment matters. It helps create a strong domestic lithium industry. This will support electrification goals and better handle global changes.

Government in the Game: Stabilizing Supply Chains

U.S. government equity in Lithium Americas offers help in these areas:

- Provide a floor for project financing — Government backing reduces the risk premium for lenders or institutional partners.

- Stabilize supply — A guaranteed domestic source reduces reliance on external shocks.

- Mitigate short-term volatility — If Thacker Pass operates under a model combining private and public capital, it could offer a more stable supply corridor insulated from market swings.

- Signal future project structures — The U.S. may increasingly demand “state-option carve-outs” or partial equity as a condition for major critical mineral projects.

In a market where excess supply can drive prices into unprofitable territory, having a strategic anchor on flagship projects becomes a competitive edge.

Lithium as a Strategic Commodity

Lithium is no longer just a commodity for battery makers — it is now a strategic asset shaping national policy. The U.S. has the reserves, capital, and political will to be a major producer. But it will take years of teamwork to turn potential into production.

The Trump administration’s willingness to consider a government equity stake in Lithium Americas suggests a broader trend: future large-scale projects may require some form of state participation to succeed.

For the U.S., the stakes could not be higher. Without a reliable domestic lithium supply, the country risks falling behind in the global EV race, remaining dependent on supply chains controlled by rivals. With it, America could not only meet its clean energy goals but also secure a critical pillar of its industrial future.