The United States’ push to lead in green hydrogen, once a centerpiece of its clean energy strategy, is slowing down. Recent policy changes by the Trump administration cut funding for hydrogen hubs. They also reduced tax credits for large-scale projects. Analysts say this slowdown could open the door for China to dominate the emerging market for low-carbon hydrogen technology.

The cuts mark a major shift from the previous administration’s investment-heavy approach. Under the Biden-era Inflation Reduction Act (IRA), the U.S. planned to spend billions to make hydrogen from renewable electricity. The goal was to decarbonize industries such as steel, cement, and chemicals, which are hard to electrify.

Now, with federal incentives being reduced or delayed, several projects are being reassessed. Developers worry that without consistent support, production costs will remain too high to compete globally.

Funding Cuts Stall the Hydrogen Hub Dream

In mid-2025, the U.S. Department of Energy began reviewing funding for several regional hydrogen hubs. These hubs were meant to create networks linking producers, users, and transport systems. Seven hubs were approved in 2023, backed by more than $7 billion in federal funding, but four are now facing cuts or slowdowns.

Industry groups warn that this could affect projects worth tens of billions of dollars. “Policy certainty is crucial for investors,” said one energy analyst cited in the Bloomberg report. “Every delay or rollback increases the cost of capital and slows deployment.”

The U.S. also faces uncertainty about the Section 45V hydrogen tax credit. This credit offers up to $3 per kilogram for hydrogen produced with near-zero emissions. The credit helped close the gap between costly green hydrogen and cheaper fossil-based hydrogen. Without it, the cost of producing green hydrogen in the U.S. could rise from $3 to $5 per kilogram to over $7, according to BloombergNEF estimates.

China Powers Ahead in the Hydrogen Race

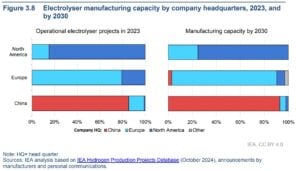

While U.S. funding stalls, China is moving fast. The country already leads the world in electrolyzer manufacturing — the core technology used to make hydrogen from water. In 2024, Chinese companies supplied more than 65% of global electrolyzer capacity, up from just 40% in 2022.

China’s domestic market is also growing. The government has set a goal to produce 200,000 tonnes of green hydrogen per year by 2025 and up to 5 million tonnes by 2030. To support this, provinces such as Inner Mongolia and Hebei have started big solar-powered hydrogen plants.

China’s advantage lies in scale and cost. Electrolyser units made in China cost $600–$1,200 per kilowatt, far lower than the $2,000–$2,600 range typical in the U.S. and Europe. If current trends continue, the price difference might make Chinese-made equipment the top choice for global projects.

Rising Costs and Shrinking Margins

Hydrogen production costs remain the biggest obstacle to global growth. The International Energy Agency (IEA) estimates that low-carbon hydrogen made with renewables costs two to four times more than conventional hydrogen from natural gas.

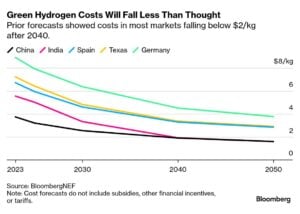

Producing one kilogram of green hydrogen costs between $4 and $12. This varies based on electricity prices and how efficient the electrolyzer is. Grey hydrogen, made from natural gas, costs $1–3 per kilogram. Analysts say costs must fall below $2 per kilogram to compete in most industries.

Scaling up manufacturing and securing cheap renewable power are key. The IEA projects that with large-scale deployment, electrolyzer costs could fall by 60% by 2030. But this requires steady investment and policy support — something the U.S. may now struggle to sustain.

According to BloombergNEF, global investment in hydrogen production and infrastructure reached $24 billion in 2024, up 50% from 2023. China accounted for nearly half of that total, while U.S. spending slowed after federal policy reviews.

Companies Pivot Amid Uncertainty

Despite the funding cuts, some U.S. companies are pressing ahead. Plug Power, a leading hydrogen firm, recently secured a $1.7 billion loan guarantee to expand production. The company plans to build several U.S. facilities that will supply green hydrogen to logistics and industrial customers.

Meanwhile, developers are adjusting strategies to reduce costs. Some plan to co-locate hydrogen plants near wind or solar farms to secure cheap power. Others are exploring blending hydrogen with natural gas in pipelines to reduce emissions without full conversion.

Industry leaders also call for cooperation with allies. The European Union, for example, continues to fund green hydrogen projects through its Hydrogen Bank initiative. They argue that closer cooperation across the Atlantic could help Western producers compete with China’s growing supply chain.

The Global Hydrogen Race

The race for leadership in green hydrogen is as much about geopolitics as it is about technology. Countries view hydrogen as a way to cut oil imports, boost industry, and ensure energy independence.

In 2024, global hydrogen demand reached about 97 million tonnes, according to the IEA. Only a small share — less than 1% — came from low-carbon production. To meet the world’s climate targets, that share must grow to at least 20% by 2030.

BloombergNEF expects the global hydrogen market to surpass $500 billion each year by 2050. This includes production, storage, and transport. But success depends on which countries can bring down costs first and scale up faster.

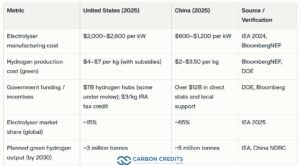

If the U.S. loses momentum now, analysts warn, it may have to rely on imported technology later — particularly from China. The following table compares the costs, market share, and 2030 planned output between the two nations.

Can America Catch Up?

Green hydrogen is central to decarbonizing heavy industry and transport. It also supports renewable integration by storing excess power from wind and solar. Without continued investment, the U.S. risks missing key climate targets.

According to the Department of Energy’s earlier projections, hydrogen could cut up to 10% of U.S. greenhouse gas emissions by 2050 if widely adopted. That potential could shrink if projects slow or shift overseas.

At the same time, China’s expansion means more global supply, which could help reduce costs worldwide. Some analysts see this as an opportunity for global cooperation — if the U.S. can focus on innovation, efficiency, and regulation rather than pure scale.

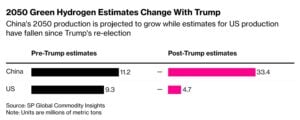

The chart from Bloomberg below shows the potential changes under Trump’s current policy moves.

Experts say the U.S. can still recover its position with the right mix of policy and private investment. Restoring tax credits, simplifying permits, and investing in electrolyzer manufacturing can help create a fairer market.

For now, China appears to have the upper hand. Its rapid manufacturing growth and strong state support have created momentum that the U.S. may struggle to match. However, as clean energy technologies mature, global demand will likely outstrip any single country’s supply.

The coming years will decide whether the U.S. remains a key player or becomes a buyer in the green hydrogen market it once hoped to lead.