Visa and Mastercard are two of the largest payment companies in the world. They process trillions of dollars in transactions each year. Their networks connect banks, merchants, and consumers across more than 200 countries.

Full year 2025 earnings show that both companies continue to grow, even as economic conditions remain uncertain. At the same time, investors and regulators are paying closer attention to sustainability and climate commitments. This article compares Visa and Mastercard with their latest earnings data, growth trends, and environmental strategies.

Earnings Show Strong Financial Performance

-

Earnings Check: Visa’s Momentum Continues

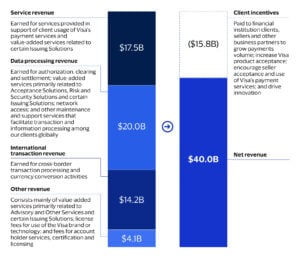

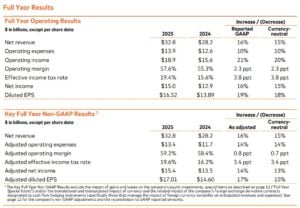

Visa reported strong financial results for its full fiscal year 2025. Net revenue reached $40.0 billion, an 11% increase from 2024. This growth was driven by higher payment volumes, stronger cross-border activity, and more transactions processed on its network.

Visa’s GAAP net income was about $20.06 billion, up from $19.74 billion in the prior year. Diluted earnings per share (EPS) grew to $10.20, compared with $9.73 a year earlier.

On a non-GAAP basis, net income was roughly $22.54 billion, and non-GAAP diluted EPS reached $11.47, both showing double-digit growth year over year. Total payments volume processed on Visa’s network was 257.5 billion transactions, up 10% from the prior year. Visa’s payment credentials also grew, reaching 4.9 billion by year-end.

-

Mastercard Delivers: Solid Results and Strategic Shifts

Mastercard also reported strong results for the full year 2025. GAAP net revenue increased to $32.8 billion, up 16% from 2024. On a currency-neutral basis, revenue also grew close to 15%.

The company’s GAAP net income was about $15.0 billion, a 16% increase from the previous year. Mastercard’s diluted EPS rose to $16.52, up from $13.89 in 2024.

On a non-GAAP basis, adjusted net income was $15.4 billion, and adjusted diluted EPS reached $17.01, reflecting 14–17% growth. Transaction activity stayed strong. Gross dollar volume rose by about 9%. Cross-border volume increased by 15%, and switched transactions were up by 10%.

Comparing Growth Drivers and Market Position

Visa and Mastercard share many growth drivers. Both benefit from rising digital payments, increased travel, and global e-commerce expansion. Cross-border transactions are especially important for revenue growth, as they generate higher fees.

Visa reported cross-border growth of about 13%, while Mastercard posted 15% growth in the same area. These figures show that international spending remains a key strength for both companies.

Visa’s larger network gives it higher total revenue. Mastercard, however, often reports higher EPS due to differences in cost structure and share count. Both companies continue to invest in technology, security, and new payment services.

Analysts expect Visa to maintain double-digit revenue growth, while Mastercard is expected to grow at high single-digit to low double-digit rates. These forecasts reflect confidence in long-term payment trends.

Why Emissions Matter for Payment Giants

Financial strength is only one part of the comparison. Sustainability has become a growing focus for payment companies, especially as investors demand clearer climate action.

Breaking Down the Carbon Numbers: 2024 Emissions

Both Visa and Mastercard publish actual greenhouse gas (GHG) emission numbers each year. These figures help show how much carbon each company produces from operations and its value chains.

-

Visa’s 2024 Emissions

In 2024, Visa shared detailed GHG emissions data. They used the GHG Protocol, which divides emissions into direct and indirect categories. Visa’s sustainability report shows its total operational emissions.

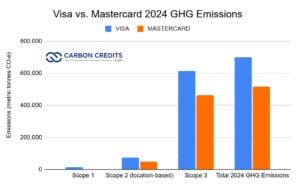

Scope 1 emissions were about 13,510 metric tonnes of CO₂e. For Scope 2, location-based emissions reached 73,448 metric tonnes of CO₂e.

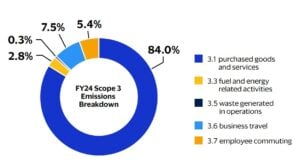

Visa also reported 613,162 metric tonnes of Scope 3 emissions. These are indirect emissions from its value chain. They come from things like purchased goods, services, business travel, and employee commuting. This brings Visa’s total GHG emissions across Scope 1, 2, and 3 to roughly 700,120 metric tonnes of CO₂e in 2024. Scope 3 made up the largest share of these emissions, around 87.6% of the total footprint.

Visa continues to work toward decoupling its business growth from emissions, even as its operations expand. It measures its footprint each year and includes renewable energy and carbon offsets as part of its strategy to manage impact.

-

Mastercard’s 2024 Emissions

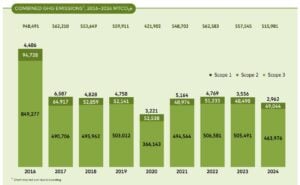

Mastercard also publishes verified GHG data. In 2024, the company’s total Scope 1, 2, and 3 emissions were 515,981 metric tonnes of CO₂e. This represents a 7% drop from 2023 and a 46% cut from the 2016 baseline.

Mastercard’s Scope 1 and Scope 2 emissions made up about 10% of the total. The other 90% came from Scope 3 indirect emissions throughout its value chain. The company has cut emissions in several categories. It is also on track to meet interim targets approved by the Science-Based Targets initiative.

Mastercard’s environmental strategy focuses on cutting operational emissions. It also aims for 100% renewable energy in its offices and data centers. The company also uses tools and programs to help partners and consumers understand and reduce their own emissions.

These emissions figures help illustrate each company’s current footprint and progress. They provide concrete benchmarks as Visa and Mastercard work toward their long-term climate goals.

Visa’s Path to Net Zero

Visa has committed to reaching net-zero emissions by 2040. This target aligns with the Science-Based Targets initiative (SBTi) and a 1.5°C climate pathway.

Visa achieved operational carbon neutrality in 2020. It maintains this status by using 100% renewable electricity across its global offices and data centers. This covers Scope 1 and Scope 2 emissions, as well as parts of Scope 3, such as business travel and employee commuting.

Visa also works to include sustainability in its products. It offers tools that help partners track the carbon footprint of transactions. The company supports initiatives related to greener transport and digital efficiency.

Visa’s approach focuses on reducing its own operational impact while enabling partners and customers to make more informed choices.

Mastercard’s Climate Playbook

Mastercard has also committed to net-zero emissions by 2040. Its target covers the entire value chain, including Scope 1, Scope 2, and Scope 3 emissions.

As of 2024, Mastercard reported a 46% reduction in greenhouse gas emissions from its 2016 baseline. Like Visa, Mastercard uses 100% renewable electricity for its operations.

One of Mastercard’s most visible initiatives is the Priceless Planet Coalition. The program aims to restore 100 million trees by 2025. As of 2024, the coalition had supported the planting of about 26 million trees.

Mastercard also provides tools that help consumers understand the carbon impact of their purchases. The company integrates sustainability standards into its supplier and partner programs.

Side-by-Side: How Their Climate Strategies Compare

Both companies share several similarities in their climate strategies. Each uses renewable electricity and has committed to long-term net-zero targets. Both also work with partners to extend sustainability beyond their own operations.

There are also differences in focus. Visa emphasizes operational neutrality and payment-based tools that support sustainable choices. Mastercard places more emphasis on measurable emissions reductions and large-scale environmental programs, such as reforestation.

Mastercard’s 46% emissions reduction since 2016 provides a clear progress metric. Visa’s early move to carbon neutrality in 2020 shows leadership in operational emissions.

Neither company directly controls most consumer emissions linked to card use. However, both aim to influence behavior through data, tools, and partnerships.

Looking Ahead: Profits, Payments, and Climate Pressure

Visa and Mastercard remain financially strong. Rising digital payments, global travel, and cross-border commerce continue to support earnings growth. Recent results show that both companies are well-positioned for the years ahead.

At the same time, sustainability expectations continue to rise. Regulators, investors, and consumers want clearer climate action from large financial companies. Both Visa and Mastercard have responded with net-zero commitments and measurable steps.

Challenges remain. Most emissions linked to payments sit outside direct operations. Reducing value-chain emissions will require broader collaboration with banks, merchants, and consumers.

Still, both companies have made climate strategy a core part of their long-term plans. Their progress shows how financial performance and sustainability goals are increasingly linked in the global payments industry.