Asian lithium prices are expected to stay weak in the first half of Q3 2024 due to oversupply and new import tariffs on Chinese electric vehicles (EVs) by the US and the EU. Lithium prices in China are projected to range between Yuan 80,000-90,000/mt ($11,022-$12,799), while prices in North Asia are likely to remain soft due to a seasonal summer lull and ample supply.

A potential turnaround may occur in the latter half of Q3, a peak season for lithium demand.

Oversupply and Seasonal Lull Pressure Lithium Prices

Supply pressure intensified as more lithium projects became operational and salt lake production levels rose in China, resulting in a 30% increase in lithium salt output and significant increases in lithium carbonate and hydroxide imports.

Platts assessed lithium carbonate at Yuan 85,500/mt and hydroxide at Yuan 79,000/mt on July 19, down over 20% from the start of Q2.

Upstream, spodumene prices began Q2 at $1,100/mt, peaking at $1,200/mt before falling below $1,000/mt by quarter’s end. The cost of producing spodumene exceeded the lithium carbonate price, resulting in negative margins and limited interest among lithium converters.

Spodumene prices need to fall below $800/mt for favorable margins in Q3. Platts last assessed spodumene at $920/mt FOB Australia on July 19, down 20% since the start of Q2.

- INTERESTING READ: The Ultimate Guide to Lithium and Lithium Prices

How Do Lithium Miners Respond?

With lithium prices at three-year lows and no signs of recovery, the focus is shifting to whether miners will cut back on the battery metal’s supply.

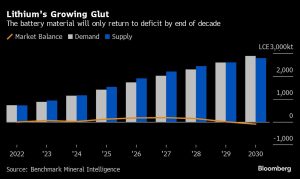

Benchmark Mineral Intelligence predicts a 32% supply growth in 2025, surpassing the expected 23% demand increase, with the surplus peaking in 2027 before a deficit returns later in the decade.

While some smaller producers have already reduced output, the larger firms may soon consider shutting mines and delaying projects in regions like Australia and Chile.

Some smaller players have already responded to the price slump. Australia’s Core Lithium halted operations at its Finniss project.

Core Lithium, which opened its mine near Darwin in October 2022, experienced rapid growth but was hit hard by the subsequent market downturn. CEO Paul Brown noted the severe commodity cycle’s impact, with the company halting production six months later and laying off over 300 employees.

Core Lithium is now in “care and maintenance” mode, awaiting a market recovery with a $15 million stockpile of processed lithium products yet to be sold and a cash balance of $87 million.

Similarly, Zhicun Lithium Group in China is putting two carbonate units into maintenance.

-

Lithium Company Spotlight: The Fastest Developing North American Lithium Junior

Experts say that sustained low prices could trigger further mine supply cuts and project delays. Recent data from Platts shows spodumene prices nearing levels that previously led to production cuts.

Chinese lithium giants Ganfeng and Tianqi reported preliminary net losses in the first half. On the other hand, Pilbara Minerals plans to expand output after reporting it has “achieved or exceeded” its full-year guidance across production volume, unit operating cost, and capital expenditure. The Australian miner recorded record production in the June quarter.

The Perth-based group produced 725,000 tonnes, surpassing Pilbara’s FY24 guidance range of 660,000 to 690,000 tonnes. This production level reflects a 17% increase compared to the previous year.

When is The Turning Point?

Despite minimal profit margins, some producers maintain output to keep skilled workforces, avoid restarting costs, and preserve buyer relationships. Other lithium miners face growing pressure to reduce production.

Linda Zhang of CRU Group noted diminished profit margins in Brazil, Chile, Argentina, and Australia. Curtailments and project deferments are expected to peak next year, potentially tightening the market balance in the medium term, according to Zhang.

With hopes fading for a significant demand rebound this year, BloombergNEF recently lowered its EV sales estimates, indicating the auto industry is falling behind in decarbonization efforts.

With supply still exceeding demand and slow EV sales growth, analysts do not foresee a near-term price recovery. They predict that while EV adoption will eventually increase lithium demand, yet the record prices of 2022 are unlikely to return. The industry must now adapt to a more sustainable operating environment, favoring low-cost producers.