The Group of Seven (G7) nations have launched a major effort to reduce their dependence on China for rare earth minerals. The move comes as Beijing tightens export controls on critical materials, raising concerns over global supply chains and national security.

At the G7 summit in France, the United States, Canada, France, Germany, Italy, Japan, and the United Kingdom pledged that no single country should account for more than 60% of their rare earth imports by 2030. The group also said it aims to lower that share to 50% as soon as possible.

The commitment reflects growing concerns that China’s dominance in the rare earth industry has become a major economic and geopolitical risk.

The Supply Chain Behind China’s Rare Earth Power

Rare earth elements are a group of 17 minerals that play a vital role in modern technologies. They are used to manufacture permanent magnets found in electric vehicles (EVs), wind turbines, semiconductors, smartphones, military aircraft, drones, and precision-guided weapons.

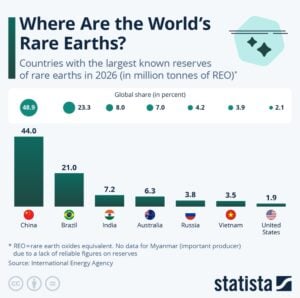

Although rare earths are mined in several countries, China dominates almost every stage of the supply chain—from mining and refining to magnet production.

According to the International Energy Agency (IEA), China currently produces around 60% of the world’s magnet rare earths. Its dominance becomes even stronger further down the value chain. The country controls more than 90% of global rare earth refining capacity and nearly 95% of permanent magnet production.

Two decades ago, China produced about half of the world’s permanent magnets. Since then, it has steadily expanded its control over the industry, making it extremely difficult for other countries to compete.

Export Controls Expose Global Vulnerabilities

China’s export controls introduced in 2025 exposed just how dependent global manufacturers remain on Chinese supplies.

Several companies outside China struggled to obtain essential rare earth materials. Some manufacturers even had to slow or reduce production because critical inputs became unavailable.

Although exports later recovered, the disruption served as a warning for governments and industries worldwide.

- The IEA estimates that if China fully implements its export restrictions, as much as $6.5 trillion worth of economic activity outside China could be affected every year. Industries at the greatest risk include automotive manufacturing, electronics, clean energy, and transportation.

The pressure could increase further as China plans to reinstate export controls on several defense-related rare earth products in November after a temporary trade truce with the United States expires.

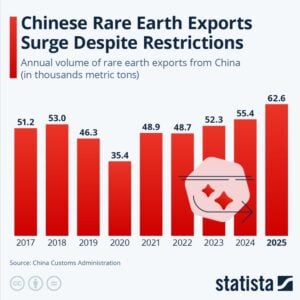

Exports Continue to Grow

Despite tighter regulations, China’s overall rare earth exports have continued to rise.

- According to Statista, citing data from China’s General Administration of Customs and Reuters, Chinese rare earth exports reached 62,600 metric tons in 2025. It was up from 55,400 metric tons in 2024.

The figure represents the country’s highest annual export volume in more than a decade.

Strong global demand from electric vehicle manufacturers, renewable energy developers, and electronics companies helped keep exports high despite export restrictions.

Analysts note that Beijing’s controls mainly target specific rare earth elements and advanced processing technologies rather than all exports. Because China remains the world’s dominant supplier, many international buyers have few immediate alternatives.

As a result, companies have started building inventories and adjusting supply chains to prepare for future trade disruptions.

Diversifying Supply Remains a Major Challenge

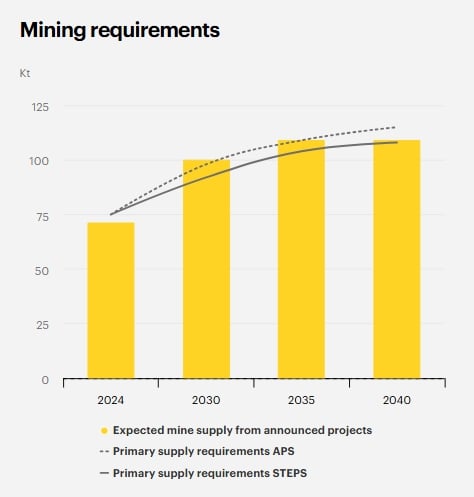

Although governments are investing in new mining projects, building an alternative supply chain will take years.

The IEA says current and announced projects outside China are far from enough to meet future demand.

By 2035:

- Existing mining projects are expected to supply only about half of the rare earth demand outside China.

- Planned refining capacity will cover only around one-quarter of future needs.

- Magnet manufacturing capacity will meet less than one-fifth of the expected demand.

The report also highlights a major imbalance. While more countries are investing in mining, far fewer are developing refining facilities and magnet manufacturing plants. Yet these downstream industries remain the biggest bottlenecks.

Without significant investment across the entire value chain, reducing dependence on China will remain difficult.

Billions Needed to Build New Supply Chains

The IEA estimates that approximately $60 billion will be needed over the next decade to develop diversified rare earth supply chains outside China.

Although this investment is substantial, it is relatively small compared with the trillions of dollars at risk if future supply disruptions occur.

Governments are therefore increasingly supporting domestic mining, refining, recycling, and advanced manufacturing to strengthen supply security.

Meanwhile, the United Nations reports that China has introduced 16 trade restrictions on critical energy transition materials since 2020. Japan, the European Union, and the United States together account for more than half of global rare earth magnet imports, making supply diversification a strategic priority.

Rare-Earth Production by Country 2026

Recycling Could Ease Future Supply Pressure

Mining alone will not solve the problem.

The IEA believes recycling could reduce demand for newly mined rare earth materials by up to 35% by 2050. At the same time, advances in alternative materials and more efficient manufacturing technologies could reduce dependence on the most constrained rare earth elements.

These innovations are expected to become increasingly important as demand for EVs, renewable energy systems, artificial intelligence infrastructure, and defense technologies continues to grow.

The Bottom Line

The G7’s new pledge marks one of the strongest international efforts yet to reduce dependence on China’s rare earth supply chain. However, achieving that goal will require far more than opening new mines.

Countries must also invest in refining, magnet manufacturing, recycling, and advanced technologies to build resilient supply chains. Until then, China is likely to remain the dominant force in the global rare earth market, leaving industries ranging from clean energy to defense exposed to future supply disruptions.