USA Rare Earth is making a big move in the critical minerals space. The company plans to acquire Brazil’s Serra Verde for $2.8 billion. This deal includes $300 million in cash and 126.9 million new shares. This values Serra Verde at about $2.8 billion based on USA Rare Earth’s share price from April 17. The acquisition is expected to close in the third quarter of 2026.

This purchase connects one of the few heavy rare earth producers outside China with USA Rare Earth’s growing mine-to-magnet platform. It aims to create an integrated supply chain for mining, processing, and magnet manufacturing. This is key as governments and industries want to reduce their reliance on Chinese supplies.

Barbara Humpton, Chief Executive Officer of USA Rare Earth, stated:

“The acquisition of Serra Verde represents a transformational step in delivering on our ambition to build a global champion and the partner of choice in rare earth elements, oxides, metals and magnets. Serra Verde’s Pela Ema mine is a one-of-a-kind asset and the only producer outside Asia capable of supplying all four magnetic rare earths at scale, together with other vital REEs, such as Yttrium. Serra Verde’s global importance is evidenced by its 15-year offtake agreement with a special purpose vehicle capitalized by various U.S. Government entities, as well as private capital sources, for 100% of its Phase 1 Nd, Pr, Dy and Tb production.

By combining Serra Verde’s world-class operations and team with our processing, separation, metallization and magnet-making capabilities, we are advancing our goal of creating a fully integrated platform that will serve as a cornerstone of global rare earth supply security for decades to come.”

Serra Verde Adds Heavy Rare Earth Supply the West Has Been Missing

Serra Verde provides access to heavy rare earths like dysprosium, terbium, and yttrium. These materials are essential for permanent magnets in electric vehicles, wind turbines, robotics, and defense tech. Sourcing them outside China is challenging. Supply concerns are rising as demand grows.

Many Western projects focus on light rare earths, but Serra Verde offers valuable heavy elements. Its Pela Ema mine in Goiás began production in 2024 after over $1.1 billion in investments. It became the first operational ionic clay deposit in the West.

REEs from clay deposits at Pela Ema

- By 2027, Phase 1 is projected to produce about 6,400 metric tons of total rare earth oxide annually. The mine aims to supply over 50% of non-China heavy rare earths by 2027. These figures boost the asset’s strategic value, with growth potential beyond current operations.

- A Phase 2 expansion could double production.

This growth aligns with USA Rare Earth’s goal of building a complete rare earth supply chain. Serra Verde adds feedstock production, while Round Top in Texas offers another source of heavy rare earths. Together, these assets strengthen the upstream supply base. But the story goes beyond mining.

Building a Vertically Integrated Rare Earth Platform

USA Rare Earth has spent years creating a vertically integrated platform. They acquired Less Common Metals in the UK, adding rare earth metal, alloy, and strip-casting capabilities. An Oklahoma magnet plant, launching later this year, will enhance downstream manufacturing.

With Serra Verde, these assets connect Brazilian feedstock, U.S. project development, European metallization, and U.S. magnet production.

- ALSO SEE: MP Materials (MP Stock): The Rare Earth Magnet Powering America’s Clean Energy and Climate Goals

Closing the Weak Links in the Supply Chain

According to the U.S. Geological Survey’s Mineral Commodity Summaries 2025, rare earth supply remains highly concentrated, with China continuing to dominate both mining and, more importantly, processing and magnet production.

Thus, this integration is crucial. Supply chain gaps have hindered Western rare earth ambitions. Mines without processing capacity face bottlenecks. Processing without secure feedstock risks supply. Magnet manufacturing without reliable materials can leave operations vulnerable.

This deal addresses these issues by combining multiple stages of the value chain. Strategic highlights from the acquisition show expansion opportunities across nearly every part of the platform.

- Upstream Supply Base: Upstream, Serra Verde’s Phase 2 growth paves the way for larger production volumes, while Round Top adds long-term potential. On the processing side, USA Rare Earth gains separation expertise through its partnership with Carester and plans to develop a rare earth carbonate separation line.

- Processing and Metallization Capacity: In metallization, the company aims to expand Less Common Metals’ reach in France, the U.S., and other markets to increase non-China metal, alloy, and strip-cast output.

- Downstream Magnet Manufacturing: Downstream, management sees potential to grow magnet manufacturing capacity for industrial customers focused on supply security. Together, these initiatives create a strategy that scales the entire supply chain rather than adding isolated assets.

Financial Structure Designed to Reduce Risk and Support Growth

The deal includes financial features aimed at reducing risk while supporting growth. Serra Verde secured a $565 million financing package from the U.S. International Development Finance Corporation to fund expansion through positive cash flow.

This eases financing pressure and supports scaling. It also has a 15-year, 100% offtake agreement for neodymium, praseodymium, dysprosium, and terbium, with minimum price floors, improving revenue stability and limiting commodity price risk.

Serra Verde expects $550–650 million in annualized EBITDA by 2027, with the combined company targeting about $1.8 billion by 2030 and roughly 80% cash flow conversion. The projections underline the deal’s transformational nature, focused on earnings growth and supply chain resilience.

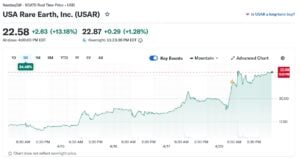

USA Rare Earth (USAR) Stock Jumps 15%

Meanwhile, USA Rare Earth secured a separate $1.6 billion funding package from the U.S. government earlier this year. The company expects more than $3.2 billion in pro forma liquidity, which includes around $1.2 billion in cash and $1.8 billion from milestone-based funding. This funding comes from DFC and the U.S. Department of Commerce loan facilities.

This government support shows that rare earth supply connects to industrial strategy and national security. Governments see critical mineral supply chains as essential for energy, advanced manufacturing, and defense. The deal’s financing reflects this change and improves the company’s financial outlook.

Significantly, USA Rare Earth (USAR stock) shares rose over 15% after the announcement, boosting the company’s market value to about $4.9 billion.

Overall, this acquisition marked a shift in how the Western rare earth industry approached supply security. Instead of relying on isolated mining projects, USA Rare Earth moved toward a fully integrated platform that connected mining, processing, metallization, and magnet manufacturing across multiple regions.

The deal strengthened access to heavy rare earths, improved supply chain control, and aligned closely with government-backed industrial strategy. While execution risks remained, the overall direction pointed clearly toward building a more secure and independent rare earth supply chain outside China.