Global aluminum markets have entered a sharp upward cycle in 2026 as geopolitical tensions in the Middle East disrupt supply chains and push energy-linked costs higher.

On May 27, 2026, Reuters reported a sharp rise in aluminum prices, which followed disruptions due to conflict in the Gulf region. These issues raised worries about tighter supply and higher production costs. Energy-intensive industries, like solar manufacturing, felt the impact the most.

The scale of the move is significant. LME aluminum prices have risen from the low-$3,000s per ton earlier this year to about $3,600–$3,650 per ton in May 2026.

Over a broader horizon, prices are now roughly 40–48% higher year-on-year, reflecting sustained tightness rather than a short-term spike. Analysts now describe the market as being driven more by supply shock than demand strength.

Gulf Supply Shock Sends the Global Aluminum Trade Into Deficit

The biggest driver behind the rally is a sudden loss of production capacity in the Middle East. Disruptions linked to the Iran conflict have impacted key Gulf smelters, including facilities in Qatar, Bahrain, and the UAE. These operations make up about 9% of the world’s aluminum smelting capacity, excluding China.

Industry estimates suggest:

- Around 2 million tons of annual production capacity have been disrupted in early 2026.

- Gulf supply equals roughly 7–9% of global output capacity.

- Some facilities may take up to one year to fully recover.

This is not just a temporary logistics issue. It is a direct production shock.

A Reuters analysis called this one of the worst aluminum supply disruptions in decades. It noted that physical shortages are tightening inventories worldwide.

The Strait of Hormuz, a critical energy and metals shipping route, has also seen reduced traffic, increasing freight uncertainty, and insurance costs.

Tight Inventories and Record Premiums Push Prices Higher

Beyond geopolitics, market structure is amplifying the price move. LME data shows aluminum prices recently reaching around $3,655 per ton, the highest level in nearly four years.

This is the second-highest level in over a decade now, after the highest price recorded in March 2022.

Aluminum Price

At the same time, physical market indicators show deeper stress:

- Global LME inventories are falling quickly.

- Some estimates suggest stock coverage has dropped to near 2–3 days of global production in extreme tightness scenarios.

- Cash premiums in major markets (Europe, Japan, U.S.) have surged sharply, reflecting the scarcity of physical metal.

In Europe, premiums are up over 70%, as reported by Reuters. In the U.S., some contracts have hit record highs, exceeding $2,550 per ton. This shows a key shift: the problem is not just futures pricing but is a real physical shortage in key regions.

Solar and EV Industries Feel the Aluminum Cost Squeeze

The aluminum price spike is quickly moving into downstream industries.

One of the most exposed sectors is solar energy manufacturing. Aluminum is used in panel frames, mounting systems, and structural components. According to analysts, aluminum accounts for roughly 9–10% of total solar project costs in utility-scale installations.

As a result, the recent price surge is translating directly into higher project costs. Rising aluminum prices might add billions in costs to U.S. solar projects planned for 2026, according to industry estimates.

Some supply contracts for racking systems have already seen price increases of around 20%, depending on sourcing and fabrication regions.

Electric vehicles are also affected, since aluminum is beneficial in reducing vehicle weight and improving battery efficiency. The construction and infrastructure sectors face similar pressures. This is especially true for large transport and grid expansion projects where demand for aluminum is both structural and non-discretionary.

This creates a paradox: aluminum is essential for decarbonization technologies, yet its price is increasingly shaped by fossil fuel-driven energy volatility and geopolitical risks.

The Market Narrative Flips From Oversupply to Structural Tightness

Just a year ago, many analysts expected aluminum markets to remain balanced or even oversupplied. That view has now shifted sharply.

Recent market estimates point to a global aluminum deficit of around 365,000 tons in 2026, depending on demand assumptions and disruption scenarios. Some forecasts suggest that deficits could widen further if energy constraints and geopolitical risks persist.

Meanwhile, structural constraints remain:

- China operates near its production cap of ~45.5 million tons.

- New smelting projects face high energy and regulatory barriers.

- Western capacity expansion is slow due to environmental constraints.

A key shift is happening: the market is moving from “flexible oversupply” to “structural tightness.”

Energy Transition Pressure and ESG Targets Add Another Layer of Cost

The aluminum industry faces geopolitical and supply pressures. It is also experiencing a big change due to decarbonization needs.

Primary aluminum production uses a lot of electricity. This means emissions rely on the energy mix used in smelting. This has placed major producers under pressure to reduce carbon intensity while maintaining output.

Several leading companies have set long-term net-zero targets.

Rio Tinto aims for net-zero operational emissions by 2050. They are investing in low-carbon smelting technologies and renewable energy for their operations.

Alcoa targets net zero emissions by 2050. They are working on an inert anode technology with their ELYSIS project. This technology could remove direct smelting emissions.

Norsk Hydro aims for net zero by 2050. It already uses a lot of hydropower in production, which greatly cuts its carbon footprint.

While these transitions improve long-term sustainability, they also increase short-term capital costs. Upgrading smelters, getting renewable energy, and following carbon pricing rules put more financial strain on a tight market.

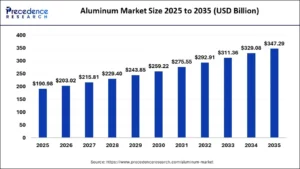

Industry projections suggest global aluminum demand could grow steadily through the next decade. Some estimates even predict long-term market value above $300 billion by the early 2030s.

However, supply growth is constrained by one key factor: energy.

Primary aluminum production is electricity-intensive. In many regions, electricity accounts for a large share of total production cost. This means:

- Higher power prices directly raise aluminum prices.

- Decarbonization of electricity systems adds short-term cost pressure.

- Smelters increasingly depend on renewable energy availability.

This creates a paradox: aluminum is essential for clean energy systems, but its production is highly exposed to energy market volatility.

A Structural Shift in a Critical Metal Market

The 2026 aluminum price surge is not just a commodity cycle. It reflects a deeper structural shift.

Geopolitical conflict has removed a meaningful share of global supply. Energy markets remain unstable. Demand continues to grow for clean energy and electrification. At the same time, production is constrained by both physical limits and environmental pressure.

Prices above $3,600 per ton, rising premiums, and tightening inventories all point to one reality: aluminum is no longer in a comfortable surplus phase. Instead, it is entering a period where shocks, whether political, energy-related, or logistical, can quickly reshape global pricing.

For industries from solar to transport, aluminum is becoming both essential and increasingly expensive.