Offtake agreements became one of the strongest signals in the carbon credit market in 2025. While spot market activity slowed, long-term commitments surged. These deals revealed how buyers think about future supply, quality, and risk.

The contrast is striking. The spot market remains large in volume but low in value. The forward market is small in volume but very high in value. This gap tells an important story about where the carbon credit market is heading.

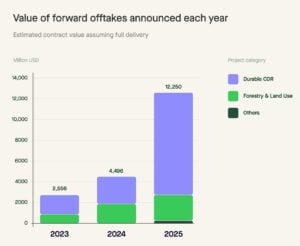

A Record Year for Offtake Value, Not Volume

In 2025, companies announced carbon credit offtake agreements worth about $12.25 billion, according to Sylvera’s report. This was a sharp increase from around $3.95 billion in 2024. It was also more than 12x the value of credits retired on the spot market during the same year.

This growth did not come from higher volumes. The total credits covered by these deals amount to roughly 78 million tonnes, spread across many years. On average, these agreements are expected to deliver only about 10 million credits per year through 2035.

To put this in context, the spot market retired about 168 million credits in 2025 alone. This means offtakes represent less than 10% of current annual retirements.

This mismatch matters. It shows that the forward market is not about scale today. It is about securing future supply that meets higher standards. Buyers are not chasing large volumes. They are targeting specific credit types with strong integrity signals.

The value growth reflects high carbon prices, not high quantities. The weighted average price implied by offtake deals in 2025 was around $160 per credit. This is far above the spot market average of roughly $6 per credit.

Why Buyers Are Willing to Pay a Premium Upfront

The forward market price premium reflects several structural factors.

-

Carbon removals dominate offtake deals:

Most credits covered by offtake agreements are carbon removal credits, not avoidance credits. These include direct air capture, biochar, BECCS, and mineralization. These technologies are costly and still scaling. -

Net-zero targets drive long-term planning:

Companies face growing pressure to meet net-zero goals. Many now acknowledge that emissions cuts alone will not eliminate all emissions. They expect to use removals to address residual emissions in the 2030s and beyond. -

Future supply remains uncertain:

Few carbon removal projects operate at a commercial scale today. Delivery risks remain high. Offtake agreements help buyers reduce exposure to future shortages and price spikes. -

Policy signals reinforce buyer behavior:

Updated guidance from standard setters and the expansion of compliance markets point to rising demand for high-integrity credits. Buyers anticipate stronger competition for a limited supply.

As a result, buyers accept high prices today to manage future risk. These prices reflect expected scarcity, not current market conditions.

A Highly Concentrated Landscape: Few Players, Big Moves

The offtake market in 2025 was not broad-based. It was highly concentrated.

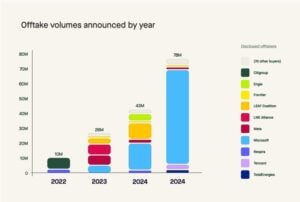

A small group of buyers accounted for most of the value and volume. Among them, Microsoft dominated the durable carbon removal market. The company accounted for about 85% of the total durable removal offtake volume announced in 2025.

Other large buyers included technology firms, energy companies, and buyer coalitions such as Frontier. However, the overall number of active offtakers remained limited. Estimates suggest only 100 to 200 buyers participated meaningfully in the forward market.

This concentration reflects both cost and complexity. Offtake agreements require long-term commitments, strong balance sheets, and the ability to manage delivery risk. Many companies are not ready to take on these challenges.

In contrast, the spot market remains much broader. It involves thousands of buyers and a wide range of project types. Prices are lower. Entry barriers are minimal.

This divide suggests that the forward market is not replacing the spot market. Instead, it operates alongside it, serving different needs and buyers.

What the Volume Gap Tells Us About Market Structure

The gap between offtake value and volume sends a clear signal about market structure.

The carbon credit market does not suffer from a lack of credits overall. Instead, it suffers from a lack of credits that buyers trust for future use.

Inventory data supports this view. Credits rated BBB or higher have been in deficit since 2023. In 2025, this deficit continued for a third year. Lower-rated and unrated credits, by contrast, remained heavily oversupplied.

Offtake buyers focus almost exclusively on the scarce segment. They prefer credits with strong durability, clear additionality, and future compliance potential. Many of these credits do not yet exist at scale.

This explains why high prices do not translate into high volumes. Project developers face long development timelines. New technologies require capital, permitting, and verification. Nature-based removal projects also take years to mature.

As a result, the forward market reflects future expectations, not current supply. It prices scarcity before it appears in the spot market.

What Offtakes Signal for 2026 and Beyond

Offtake agreements offer several insights into the near-term outlook.

- First, they suggest that quality premiums will persist. Even if spot prices remain low for lower-quality credits, prices for high-integrity projects are likely to rise. Buyers are already anchoring expectations at much higher levels.

- Second, they show that carbon removal credits will shape long-term demand, even if near-term retirements remain small. Investment and offtake activity indicate confidence that removals will play a central role after 2030.

- Third, they highlight growing competition between voluntary and compliance demand. As markets converge, credits eligible for compliance use may attract both types of buyers. This will further tighten supply for premium projects.

- Fourth, they suggest that the total market value could grow without higher volumes. If even a small share of spot market demand shifts toward higher-priced credits, overall spending could increase significantly.

However, risks remain. Delivery delays, policy uncertainty, and technology challenges could slow progress. The forward market remains narrow and exposed to concentration risk.

For now, offtakes function as a price and preference signal, not a volume driver. They show where the market wants to go, even if it cannot get there yet.

The offtake buyer behavior reflects bigger changes in how companies view carbon credits. Price alone no longer defines value. Credibility, durability, and future eligibility now matter most.

As the market moves into 2026, offtake agreements will continue to shape expectations. They do not replace the spot market, but they signal where demand, pricing, and strategy are heading in the years ahead.