Carbon credit transaction network “Carbonplace” formed by nine global banks including UBS Group AG and Canadian Imperial Bank of Commerce will launch early 2023 after going through pilot trades.

The new platform, Carbonplace, is a global carbon credit transaction network that will enable the simple, secure, and transparent transfer of certified carbon credits. It has settled pilot trades of environmental credits in Australia, Brazil, Singapore, and the UK.

Carbon credits can help channel large-scale investments needed to fund carbon reduction and removal projects.

- As per BloombergNEF, demand for carbon credits can grow ~40x in the next three decades. This is due to companies’ use of credits as part of their 2050 net zero emissions strategy.

Unfortunately, the business of trading the credits has been criticized because of some firms using low-quality carbon credits to offset their emissions. Plus, the voluntary carbon market (VCM) relies on bilateral trading that’s often slow, opaque, and risky. These reduce trust in the market.

This is where Carbonplace comes in. The platform will only settle trades of credits that are verified by top carbon registries, such as Verra and American Carbon Registry.

Carbonplace and How it Works

Carbonplace’s unique blockchain-enabled technology will significantly change how carbon credits are bought and sold. It works similarly to Xpansiv CBL carbon market platform, the most dominant player today.

The trading process of Carbonplace includes procedures dealing with money-laundering and anti-fraud regulations.

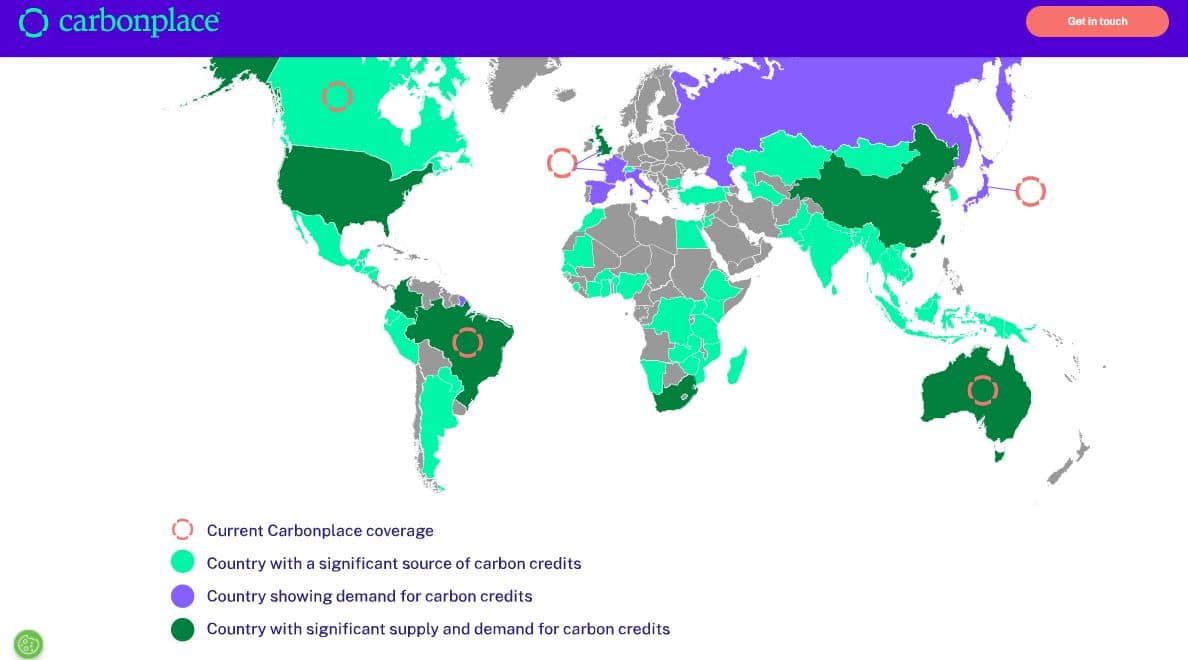

Backed by large banks with a global client base, Carbonplace will have the ability to connect the markets, registries and exchanges of the VCM directly to millions of customers in various markets as shown in the map.

The carbon credit network’s member banks or founding partners include:

- National Australia Bank

- CIBC

- UBS

- Natwest Group Plc

- Itaú Unibanco

- Standard Chartered

- BNP Paribas

- Sumitomo Mitsui Banking Corporation (SMBC)

- BBVA

They all share a common ambition to support urgent, large-scale climate action. They recognize the need for strong collaboration between the financial sector and other carbon market participants to bring trust, transparency, and accessibility to the VCM.

As to how Carbonplace works, the product’s chief officer Robin Green said:

“Think of it like eBay… We are just broadening the access to the market by providing transparency and trust. It’s not that you can’t buy credits right now, but we are really simplifying the process.”

The network will deliver those essential elements of a growing VCM with these three values:

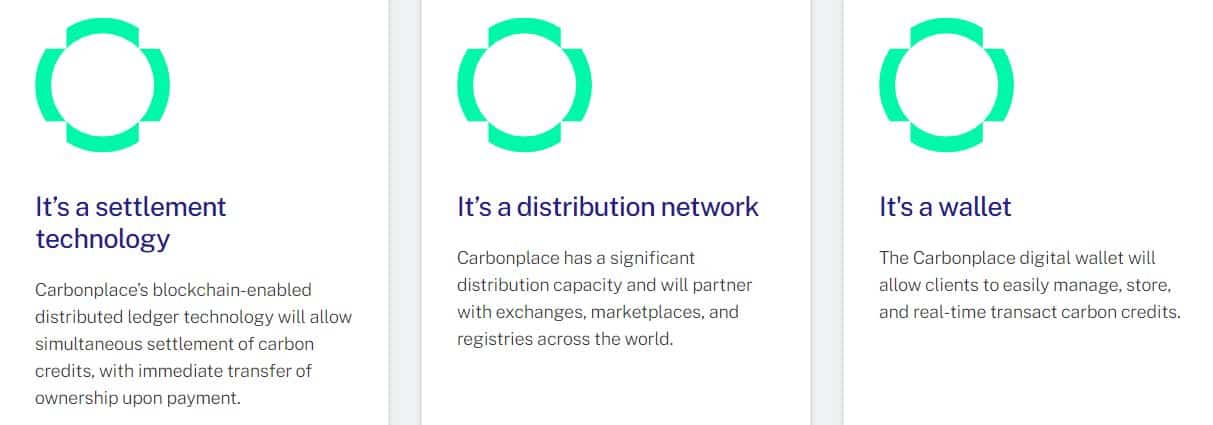

It’s simple. The Carbonplace Rulebook will see to it that all members of the platform follow a single set of prudential rules, which removes the need for bilateral contracts between buyers and sellers. This makes it possible to retire credits within minutes and reduce the burden of individual transactions.

It’s secure. The network’s robust KYC will deliver another level of security. It enables customers to rely on the banks they already trust for settlement purposes.

It’s transparent. Carbonplace’s full ledger, audit, and reporting functionality will manage the carbon credit lifecycle from inception until retirement. This provides reliable records of ownership of carbon credits and reduces the risks of double counting.

Where Two Worlds Meet: Carbon Markets and Banking

Carbonplace is a place where the emerging world of carbon markets meets the established world of banking. How that looks is like this.

The instant, secure, and traceable settlement of carbon credit transactions via a secure, distribution network is critical in scaling the VCM.

The pilot trades on the Carbonplace network involved selling carbon credits from Carbon Growth Partners in Melbourne and Sustainable Carbon in Sao Paulo to banks.