Compliance carbon markets in Asia are entering a new stage. They are expanding in size and changing in design. At the same time, new finance tools are being tested for coal transition and nature-based projects.

Two recent developments show this shift clearly.

First, the International Energy Agency (IEA) says compliance carbon markets could become the largest source of demand for transition credits linked to coal phaseout in Southeast Asia. But this only works if developers can prove that early coal closures are truly additional. This is harder now because renewable energy costs are falling fast.

Second, Shanghai is planning to expand its emissions trading scheme (ETS) by lowering the entry threshold for industries. This change is part of a reform plan that runs toward 2030.

Meanwhile, new nature finance platforms are starting in Southeast Asia. One example is the soft launch of the Nature Catalyst investment platform. Together, these moves show that carbon markets in Asia are growing. But they are also becoming more complex.

IEA Sees Transition Credits as a Coal Exit Tool—With Strict Conditions

The IEA report, Financing the Modernisation of Power Systems Beyond Coal, focuses on Southeast Asia. This region still relies heavily on coal power.

Electricity demand in Southeast Asia is growing fast. The IEA says it rises by around 3–4% per year through 2040. Over the past decade, electricity demand in the region has grown by more than 60%.

Coal power is still a large part of the system. Southeast Asia has more than 121 GW of coal capacity. It also has about US$130 billion in remaining unamortized coal assets.

This creates a challenge. Many coal plants cannot close easily without financial support.

The IEA says transition credits may help solve this problem. These credits would pay for early coal plant closures and help replace them with clean energy. But there is a strict condition:

- Projects must prove additionality. This means the coal plant would not have closed without carbon finance.

This is becoming harder because renewable energy is now cheaper in many markets. Some coal plants may close anyway due to market forces.

The IEA warns that compliance carbon markets could become the biggest source of demand for transition credits, but only if the rules are strict. The key rules must include:

- Clear emissions baselines,

- Proof of early coal retirement,

- Tracking of replacement clean energy, and

- No double-counting with other policies.

Without these rules, credits may not reflect real emissions cuts. Currently, here are the existing credit methodologies as of April 2026.

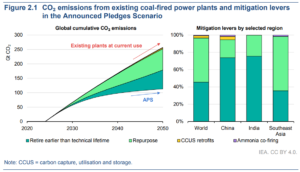

Moreover, to cut emissions and keep the grid reliable, the report suggests several paths. These include replacing energy with renewables, modernizing the grid, using flexible coal operations, and implementing carbon capture, utilization, and storage (CCUS).

The IEA states that CCUS can help newer coal plants operate with lower emissions. This is important in systems where coal is still a key source of baseload power.

In wider Southeast Asia, the agency estimates that CCUS deployment may need to capture 200 million tonnes of CO₂ each year by 2050. Also, investment could reach nearly US$1 billion annually from 2025 to 2030.

Shanghai ETS Reform Expands China’s Carbon Market Coverage

China’s carbon market is also changing. Shanghai is planning to expand its emissions trading scheme. It will do this by lowering the entry threshold for industries. This means more companies will join the system. This reform is part of a wider ETS plan that runs through 2030.

China already has the largest ETS in the world by emissions covered. It regulates more than 4 billion tonnes of CO₂ (CO₂e basis) each year.

Lowering entry thresholds usually leads to:

- More companies covered,

- Higher total emissions under regulation, and

- Stronger carbon price signals.

This change is important because it increases market reach. It also strengthens carbon pricing across more industries. It also shows a wider trend in Asia.

Many ETS systems in the region are still growing. Shanghai’s reform may guide future ETS changes in other countries.

Nature-Based Solutions Finance Expands in Southeast Asia

Nature finance is also growing in the region. The Nature Catalyst investment platform has now soft-launched in Southeast Asia. It has signed agreements with four companies. These companies will help scale nature-based solutions (NbS).

Nature-based solutions include:

- Forest protection and reforestation,

- Mangrove restoration,

- Sustainable land management, and

- Biodiversity protection projects.

These projects can also generate carbon credits in many cases. Southeast Asia is an important region for this type of work. It has large forests and high biodiversity. It also has strong potential for carbon removal and avoided deforestation projects.

But nature finance alone is not enough. The IEA report shows that clean energy systems must also grow at the same time. Otherwise, emissions from coal power will remain high.

The Additionality Problem Is Becoming a Core Market Risk

A key issue runs through all these developments. Renewable energy costs are falling. Solar and wind are now cheaper in many places. This means coal plants may close without carbon credits.

At the same time, transition credits depend on proving that closures would not happen without financial support. This creates a problem called the “additionality gap.”

If a coal plant were to close anyway, then issuing credits does not reduce emissions. If it does not close, then credits are needed to speed up the transition.

The IEA warns that this balance is now harder to manage. It also means carbon markets must improve how they measure real impact. Otherwise, trust in the system could weaken.

Carbon Markets in Asia Are Growing, But Trust Will Decide Their Future

Carbon markets in Asia are expanding quickly. The IEA says compliance carbon markets could become the biggest demand source for transition credits in coal-heavy regions like Southeast Asia. Electricity demand in the region is rising by 3–4% per year, which keeps pressure on power systems.

Meanwhile, Shanghai is expanding its ETS by lowering entry thresholds and adding more companies to its carbon pricing system. This strengthens China’s already large market, which covers more than 4 billion tonnes of CO₂ each year.

Nature finance is also growing through platforms like Nature Catalyst, which is scaling investment into ecosystem-based projects. However, all these systems face the same challenge.

They must prove real emissions cuts. Without strong rules on additionality, measurement, and verification, carbon credits and transition credits may not reflect real climate progress.

Asia is becoming a key region for carbon market innovation. But its future will depend on one thing above all: credibility.