The World Economic Forum, together with Accenture, released the 1st edition of its report that tracks the current state of the net zero transition in 6 key industries.

WEF calls it the Net-Zero Industry Tracker 2022. The report highlights the importance to understand the challenge for the heavy industries towards net zero. It also identifies the gaps to fill to achieve net zero goals to limit global warming to 1.5 degrees by 2050.

High energy prices and supply chain concerns drive the urgency of decarbonizing the industries.

Hence, the framework offers a holistic perspective and standard metrics to measure progress of the industrial sector.

Plus, it provides seven cross-sectoral recommendations for industrial firms, consumers, and other stakeholders.

The WEF Net Zero Industry Tracker 2022

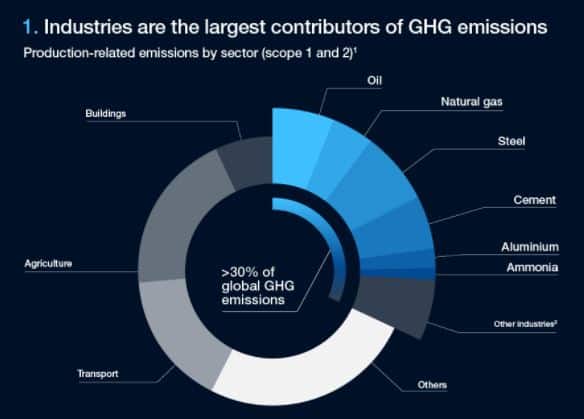

Industry accounts for around 40% of global energy consumption and over 30% of global GHG emissions.

As the largest emitter, the industries decarbonization will be critical to tackling climate change.

This is where the WEF’s net zero industry tracker framework comes in. Roberto Bocca from WEF said that:

“Several industrial sectors and individual companies have set up targets with the aim of reaching net zero emissions. We believe that bringing transparency to closing net-zero gaps and reporting on this progress is critical to achieve these ambitious goals…”

The report will track the “net zero performance” of the heavy industries and their “net zero readiness“. The six key industries include:

- Steel

- Cement

- Aluminium

- Ammonia

- Oil and

- Natural gas

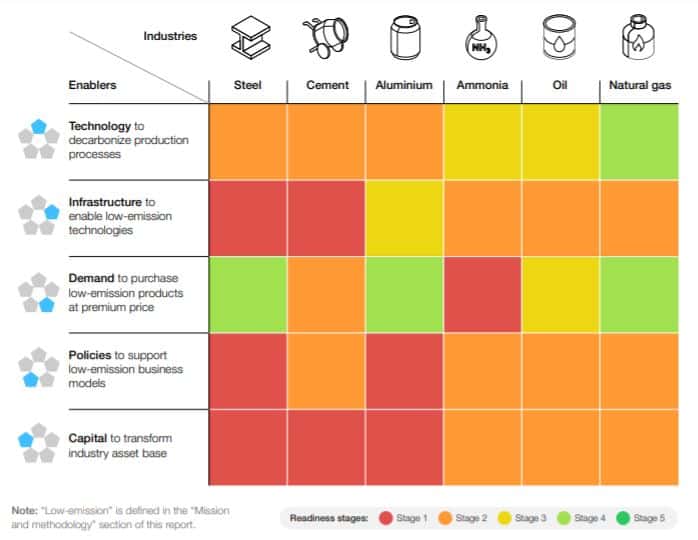

Together, these industries account for 80% of industrial emissions as per Accenture analysis. Monitoring their readiness involves measuring 5 major enablers:

technology, infrastructure, policies, demand, and capital.

Here’s the cross-industry findings of the report for net zero readiness of each sector per enabler:

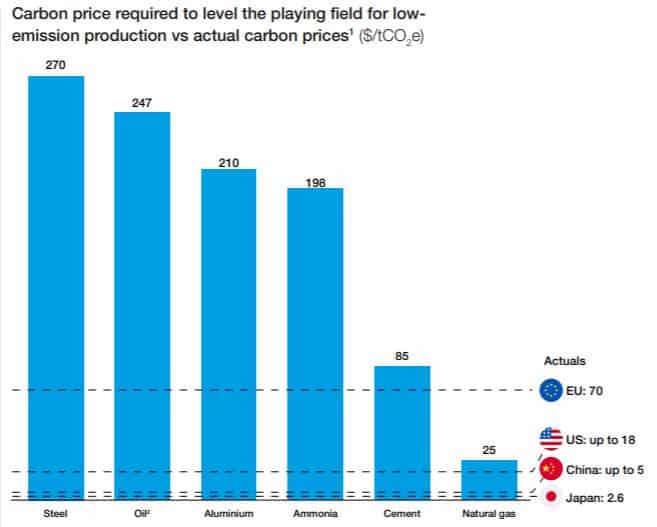

The report also points out that ~$2 trillion is necessary to make low-emission industries a reality. This calls for huge policy incentives to level the playing field for low-emission production.

The chart below shows how much carbon pricing should be for each industry sector compared with the current price.

With that said, investments in low-emission assets can be riskier for firms due to their dependencies on new technologies and infrastructure.

This needs collaboration across the sectors to make the key enablers come together in the same direction to speed up progress towards net zero.

Net Zero Tracker Key Highlights Per Industry

Here are the major findings of the WEF’s net zero tracker report for each industrial sector.

Steel industry

![]()

- Steel is the largest emitter, generating 7% of all man-made emissions.

- Steel demand can increase up to 30% by 2050.

- Needs over $2 billion investments in low-carbon power, clean hydrogen and CO2 handling infrastructure.

- Green premium of 25-50% for buyers due to high costs of clean technologies.

There are 3 main pathways to decarbonize steelmaking: carbon capture, hydrogen and electrochemistry.

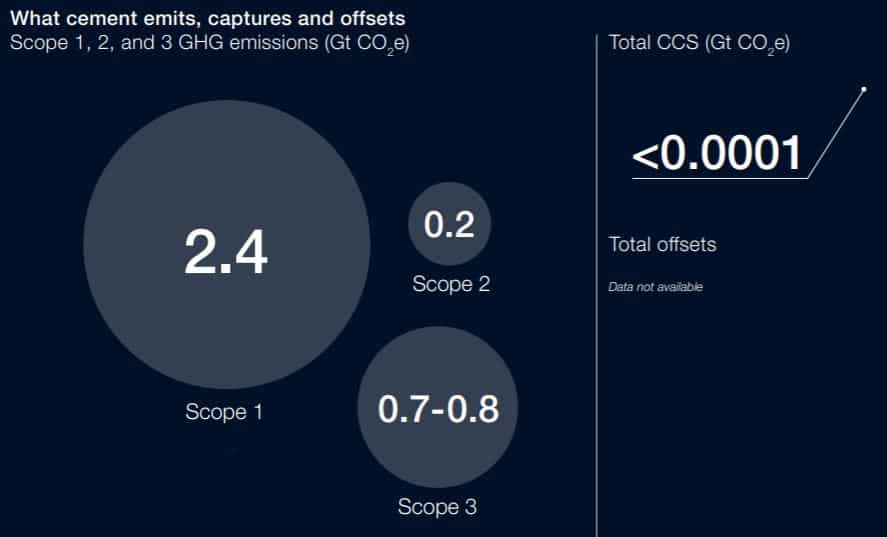

Cement industry

- Cement is the second largest emitter, generating 6% of total emissions.

- Demand for cement can go up to 45% by 2050.

- Requires ~$185 billion for CO2 handling infrastructure and clean hydrogen production in cement plants.

- Green premium above 50% for low-emission cement.

Carbon capture is key to cement’s net zero pathway, but electrification and hydrogen also have roles.

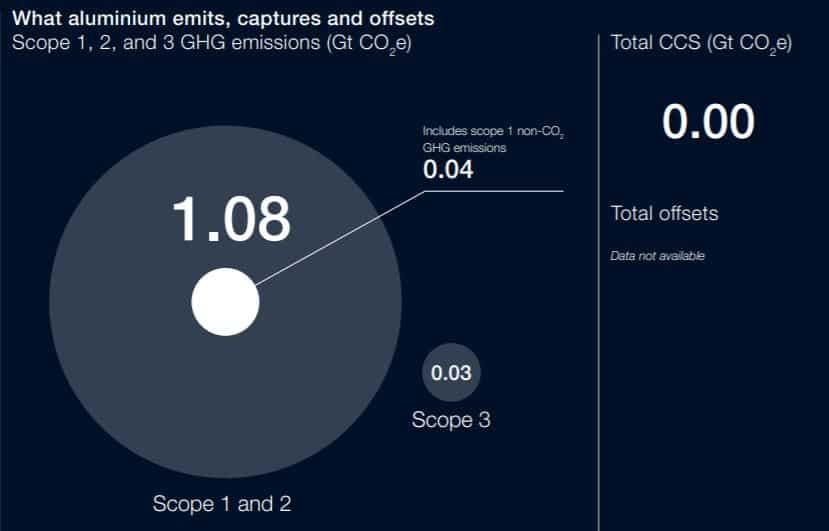

Aluminium industry

- Aluminium accounts for 2% of all industry emissions.

- Aluminium demand will jump by up to 80% by 2050.

- Calls for ~$510 billion investments to enable clean technologies and production.

- Green premium up to 40% to wholesale buyers and 1-2% to end consumers.

The major pathway for aluminium production to achieve net zero is a mix of electrification, transition to hydrogen, and inert anodes. Yet, carbon capture is also under exploration.

Ammonia industry

- Ammonia is the chemical sector’s largest emitting product, releasing 1.3% of all emissions.

- Ammonia demand for fertilizer and industrial use will go up to 37% by 2050.

- Needs ~ $850 billion investments to enable green and blue hydrogen production.

- Green premium of up to 100%.

The best way to decarbonize ammonia production is to develop blue or green hydrogen technologies.

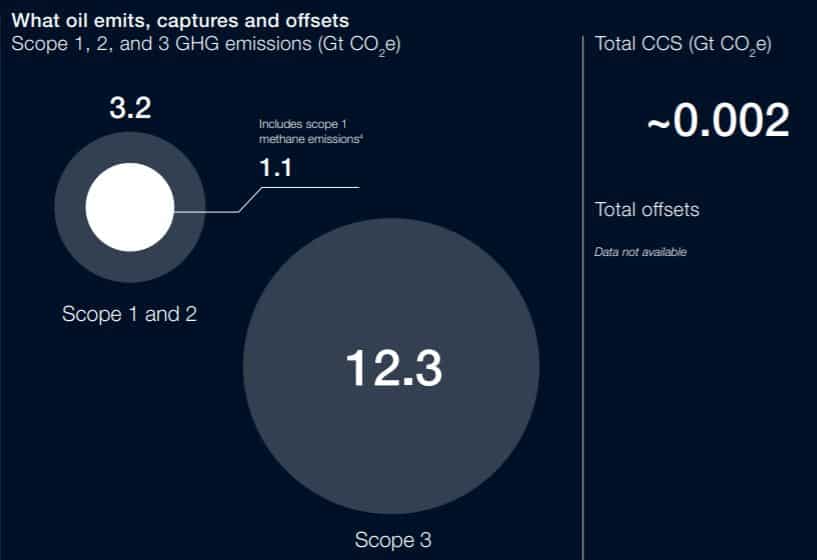

Oil industry

- The oil sector consumes so much fossil fuels and releases methane, producing 6% of total GHG emissions.

- Demand for oil will increase by 17% by 2050 but should go down by 73% for the world to reach net-zero.

- 35% of oil sector emissions are methane (70% of which can be abated at zero or minimal costs today).

Decarbonizing the oil sector means cutting methane and flaring emissions. The same goes for energy and process related emissions in refining oil. This requires carbon capture, use and storage, hydrogen, and electrification pathways.

Though substitutes for oil products are available, their availability and affordability remain a concern.

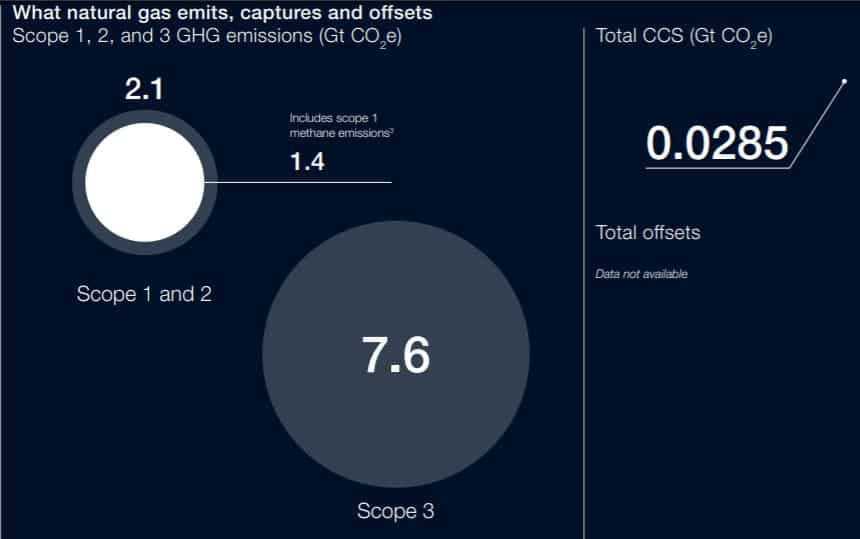

Natural gas industry

- The gas sector also uses a lot of fossil fuels and emits methane, releasing 4% of all GHG emissions.

- Demand for gas will go up by 30% by 2050 but need to drop by 55% to reach net zero scenario.

- 65% of the gas sector emissions are methane (70% of which can be abated at zero or minimal costs today).

- As low as 1-3% as a green premium to end consumers.

Mature technologies exist to abate 80% of gas sector emissions. This will result in a 7% increase in production cost.

For all industrial sectors, they all need stronger demand signals from buyers and policies to incentivize investments.

The net zero industry tracker further suggests that concerted efforts should include lawmakers, financial entities, and consumers.

And of course, the biggest effort must come from the heavy industrial firms themselves.