CCUS aims to fight climate change by capturing emissions from known polluting processes. Captured emissions are then stored and moved to be reused or stored in areas where they will not pollute the environment.

The major problem with CCUS lies with the reliance on fossil fuels to maintain the industry. To fight climate change, the amount of carbon emissions being released must be decreased. CCUS relies on carbon emissions being continually produced to trap and store it. Rather than encouraging alternative methods of fuel, CCUS maintains fossil fuels as a primary source of fuel.

The global capacity for CCUS is about 0.1% of annual carbon emissions. Climate experts believe this number is not high enough for CCUS to be a viable strategy to combat climate change. However, one method cannot fight climate change alone. Every strategy available is needed to achieve the goals of the Paris Agreements.

US forests providing carbon credits are burning as wildfires rage across the west coast and throughout North America. Forests purchased by companies like Microsoft are feeling the brunt of the destruction.

Microsoft, Apple, and Amazon have all pledged to be net-zero emitters. As such, these companies rely on forests that create carbon credits to remain net-zero emitters. Wildfires are huge threats to major companies’ emissions. A single wildfire often burns and destroys over 100,000 acres of forest. 1 tonne of carbon removed from the atmosphere equals to 1 carbon credit meaning there are also financial costs associated with wildfires from a corporate standpoint.

Many of the tech companies which purchase carbon forests, are often located on the west coast where most wildfires happen. In Oregon, a fire near Klamath Falls has occurred in an area where Microsoft purchases carbon credits.

Companies using carbon credits from forests do use a buffer pool in case of wildfires. However, the buffer pool is not enough. 10-20% of the total credits produced from forests are used to fill the buffer pool. As well, the buffer pool is not able to keep up with the amount wildfires in North America currently.

This year is set to be the worst year on record for wildfires in the US. Last year, a new record was set. Solutions to wildfires will need to be found if forests remain the primary way companies create carbon credits.

Climate change will not stop because of a singular method. New laws, protocols and mandates are effecting that carbon emissions need to be reduced. The means include tariffs, reduced emissions and planting more trees.

To meet the goal of limiting the global temperature to 1.5 degrees Celsius above pre-industrial levels, all possible methods must be explored.

A new method has emerged that could be a leading method to limiting temperature increases called direct air capture.

A company called Climeworks is operating a plant in Switzerland to remove carbon emissions from the atmosphere. According to Climeworks, they remove 900 tons of carbon dioxide annually. Switzerland produces 40 million tons of C02 every year. This may seem small at first glance, but the technology is in its infancy and has ample room to grow.

Climeworks has attracted many investors to its cause. Notable investors include names such as Microsoft and Shopify. This has allowed to Climeworks to begin construction on a new plant in Iceland.

A positive of direct air capture is ability to reuse carbon dioxide in industrial processes. Coca-Cola purchases carbon dioxide from Climeworks. Large oil companies as well use the extracted gases to obtain oil from the ground.

Not only can Climeworks sell actual carbon dioxide, but they are also able to sell carbon credits they gain from removing greenhouse gases from the atmosphere. This is a huge factor in attracting investors.

While it would require significant investment to reach a point where direct air capture would make a dent in climate change, it does offer a solution.

China’s plan is very similar to the concept of carbon credits. First, emission limits are given to companies based on data from the previous year. Buying or selling allowed emission amounts from other companies increases or decreases the max pollution limit.

As well, Companies involved in the plan are to submit emissions data annually. Then, the Ministry of Ecology and Environment checks the results. Exceeding the emission limits will result in fines or decreasing the allowable emission limit.

Initially, the program will include companies in the coal and gas sectors. The end goal is to cover 10,000 companies from all high-emission industries such as aviation, iron and steel, chemicals, and building materials.

China aims to be a net-zero emitter by 2060. Currently, China is responsible for 27% of the global carbon emissions. This could mark a huge shift in global carbon markets. As emissions decrease, the amount of credits available will also decrease.

President of China Xi Jinping said in a speech to the UN last September that China is on track to produce peak emissions before 2030. The new carbon plan is a step in the right direction that shows China’s willingness to fight in the battle against climate change.

More and more firms are pledging to contribute to climate change mitigation by reducing their own greenhouse-gas emissions as much as possible. Many businesses, however, realize that they are unable to entirely eliminate or even reduce their emissions as quickly as they would want.

The job is more challenging for businesses striving for net-zero emissions, which means eliminating the same amount of greenhouse gas from the environment as they put into it. Many people will be forced to use carbon credits to offset emissions that they cannot reduce via other means.

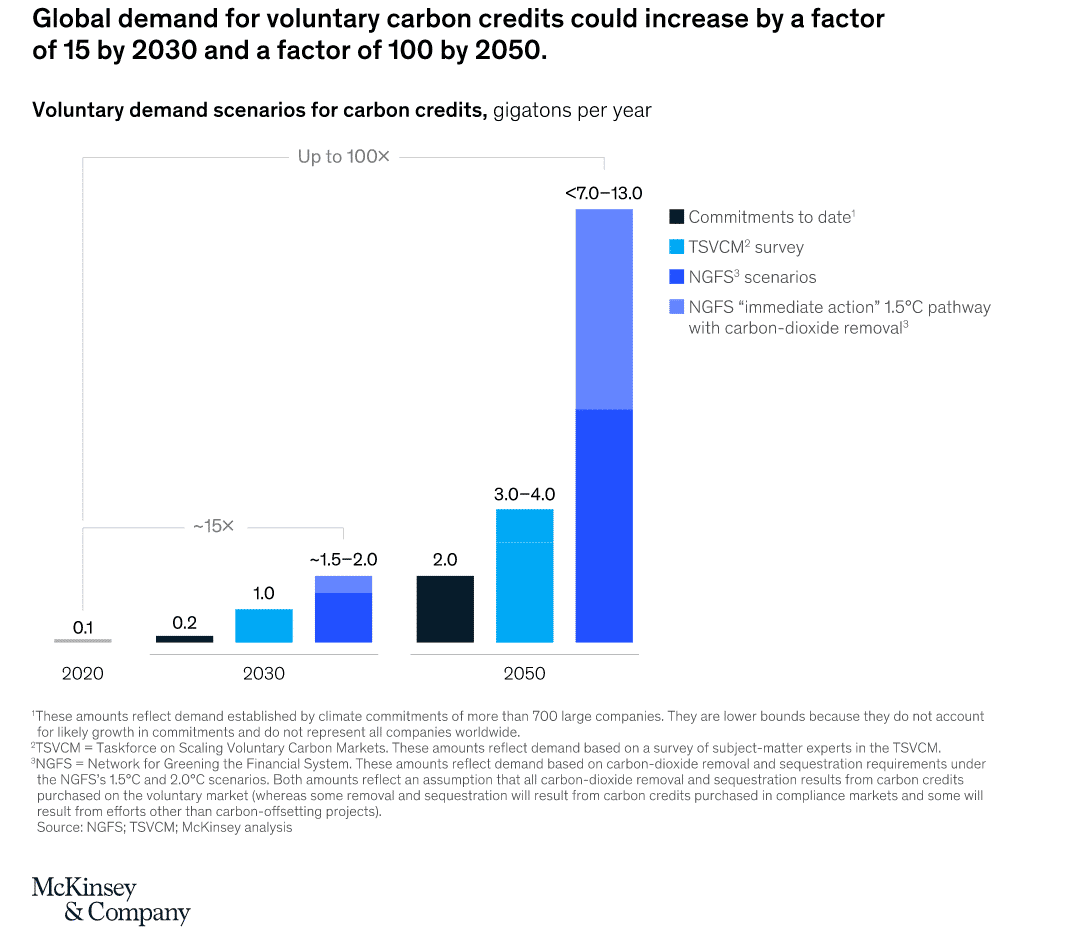

The Taskforce on Scaling Voluntary Carbon Markets (TSVCM) of the Institute of International Finance (IIF) predicts that demand for carbon credits would increase by a factor of 15 or more by 2030, and by a factor of up to 100 by 2050.

By 2030, the carbon credit market may be worth more than $50 billion.

The market for freely obtained carbon credits (rather than for compliance purposes) is significant for a variety of reasons. Voluntary carbon credits redirect private financing to climate-action projects that would not be possible otherwise.

These activities might include biodiversity conservation, pollution avoidance, public-health improvements, and job development. Carbon credits also stimulate investment in the required innovation to bring the cost of new climate technologies down.

Furthermore, larger voluntary carbon markets would allow money to be mobilized to the Global South (Latin America, Asia, Africa, and Oceania) where the most cost-effective nature-based emissions-reduction efforts exist.

Given the anticipated demand for carbon credits from global attempts to reduce greenhouse-gas emissions, the world will require a large, transparent, verifiable, and environmentally sound voluntary carbon market.

However, the market today is fragmented and complex. Some credits were discovered to indicate emissions reductions that were, at best, questionable. Consumers are unsure if they are paying a fair price, and suppliers are unsure how to handle the risk of investing and working on carbon-reduction efforts without knowing how much consumers would eventually pay for carbon credits.

Using carbon credits to achieve climate change goals

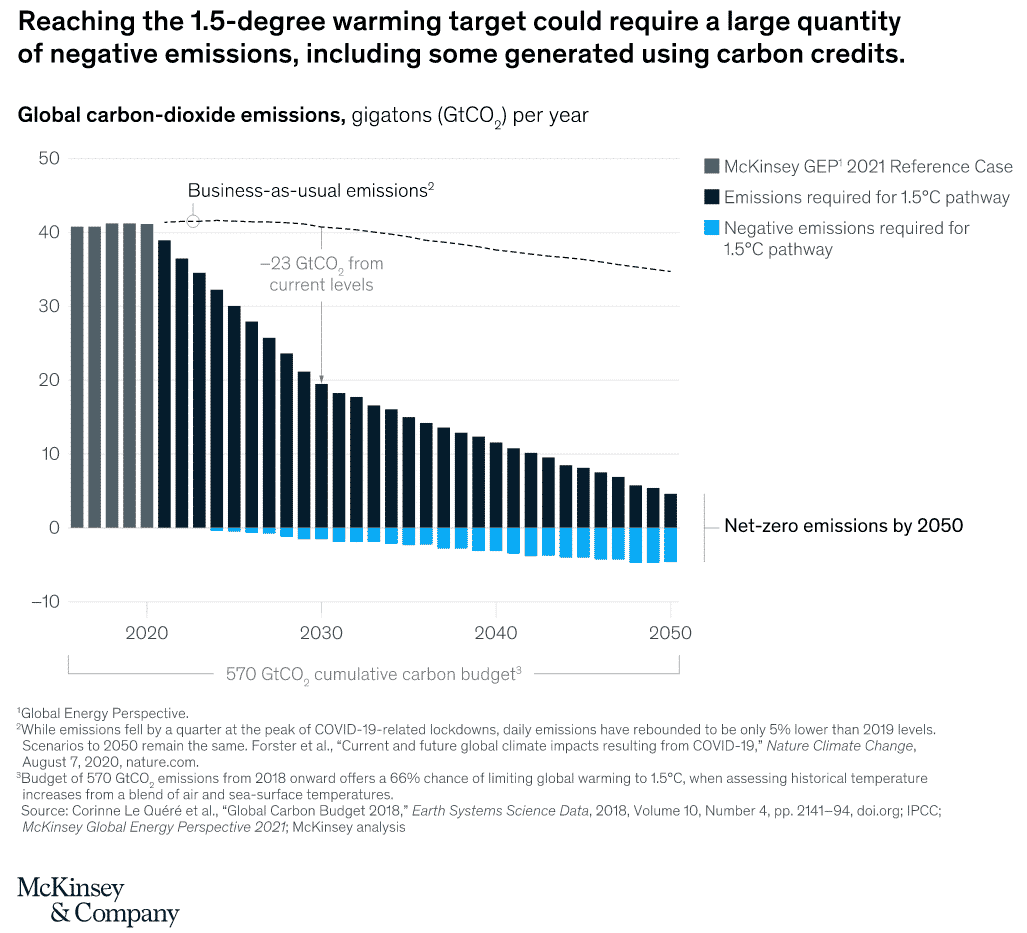

The 2015 Paris Agreement, ratified by almost 200 countries, established a global aim of limiting average temperature rises to 2.0 degrees Celsius over preindustrial levels, ideally 1.5 degrees.

To reach the 1.5-degree target, global greenhouse-gas emissions must be reduced by half by 2030 and to zero by 2050.

More companies are embracing this movement: in less than a year, the number of organizations with net-zero pledges has more than quadrupled, from 500 in 2019 to over 1,000 in 2020.

To reach the global net-zero goal, companies must reduce their own emissions as much as feasible (while also measuring and reporting on their progress, to achieve the transparency and accountability that investors and other stakeholders increasingly want).

However, lowering emissions using today’s technology is too expensive for certain firms, even though the costs of those technologies may reduce over time. Furthermore, many causes of pollution cannot be eliminated at all businesses.

For example, large-scale cement production often necessitates a chemical process known as calcination, which accounts for a sizable percentage of the cement sector’s carbon emissions. Because of these restrictions, the emissions-reduction strategy for achieving a 1.5-degree target essentially requires “negative emissions,” which are achieved by removing greenhouse gases from the atmosphere.

The chart below shows what needs to be done going forward to meet that target.

Purchasing carbon credits is one way for a company to deal with emissions that it cannot eliminate. Carbon credits are certificates that represent the quantity of greenhouse emissions kept out of or removed from the atmosphere.

While carbon credits have been around for a while, the voluntary carbon credit market has grown significantly in recent years. According to McKinsey, buyers will retire carbon credits totaling about 95 million tonnes of carbon-dioxide equivalent (MtCO2e) in 2020, more than double the quantity retired in 2017.

As attempts to decarbonize the global economy ratchet up, voluntary carbon credits may become increasingly popular.

Based on stated demand for carbon credits, demand projections and the volume of negative emissions required to meet the 1.5-degree warming goal, McKinsey estimates that annual global demand for carbon credits could reach 1.5 to 2.0 gigatonnes of carbon dioxide (GtCO2) by 2030 and 7 to 13 gigatonnes of carbon dioxide (GtCO2) by 2050.

The market size in 2030 might vary from $5 billion to $30 billion at the low end to more than $50 billion at the high end, depending on pricing assumptions and underlying variables.

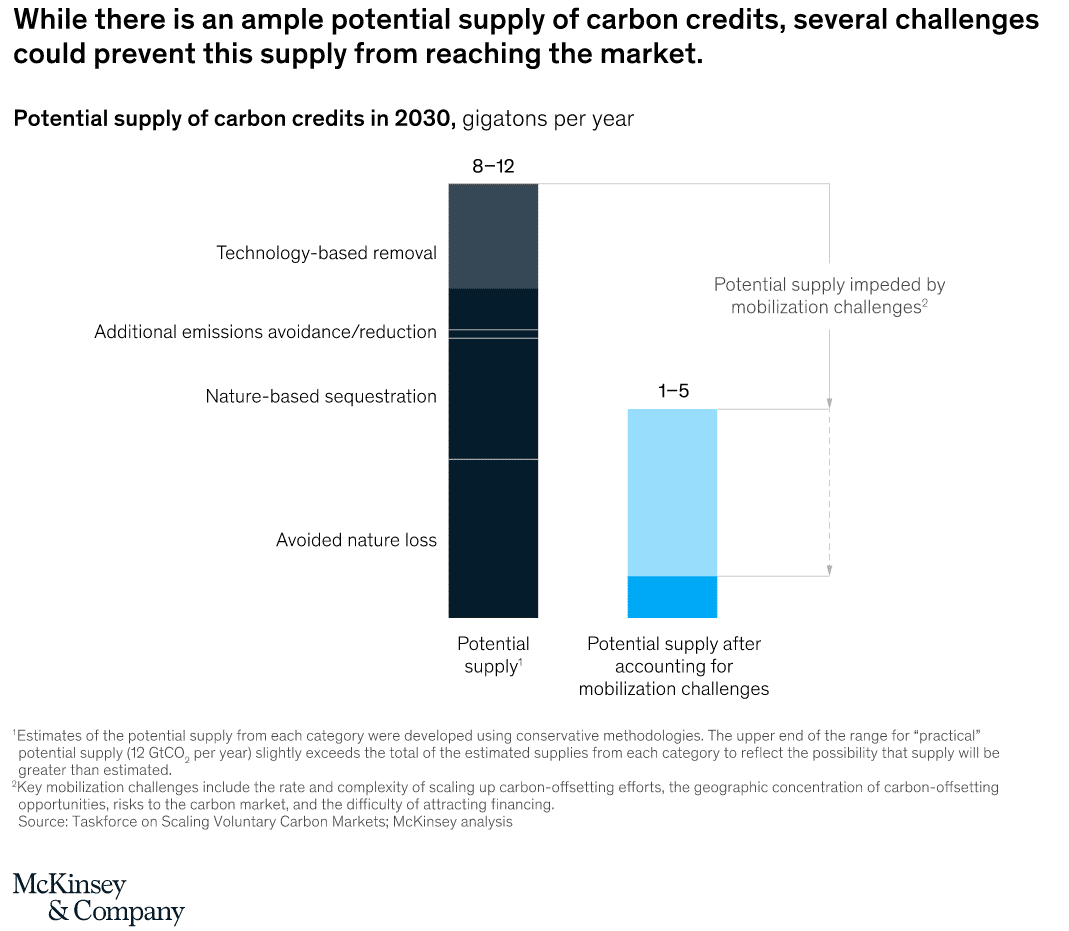

Despite the fact that demand for carbon credits has grown substantially, McKinsey predicts that demand in 2030 may be fulfilled by the potential annual supply of carbon credits: 8 to 12 GtCO2 per year.

These carbon credits would come from four sources: avoided nature loss (including deforestation); nature-based sequestration, such as reforestation; avoidance or reduction of landfill emissions, such as methane; and technology-based removal of CO2 from the atmosphere.

A variety of factors, however, may make mobilizing and bringing the entire potential supply to market challenging. The development of the project would have to be accelerated at an unprecedented rate.

The majority of the potential supply of avoided environmental degradation and natural-based sequestration is concentrated in a few countries. Many sorts of projects may fail to acquire finance due to the large lag times between the initial investment and the ultimate sale of credits.

When these restrictions are considered, the expected supply of carbon credits by 2030 decreases to 1 to 5 GtCO2 per year.

These aren’t the only problems that carbon credit buyers and sellers confront. Due to variations in accounting and verification procedures, as well as co-benefits of credits (such as community economic development and biodiversity protection) that are rarely fully specified, high-quality carbon credits are scarce.

When it comes to evaluating the quality of new credits, suppliers have considerable lead times, which is a critical step in maintaining the market’s integrity. When it comes to selling such credits, suppliers face unpredictable demand and rarely receive competitive price.

Overall, the market is marked by a lack of liquidity, inadequate financing, poor risk-management services, and limited data availability.

These challenges are significant, but they are not insurmountable. Verification techniques may be improved, and verification procedures can be made simpler.

Clearer demand signals would instill greater confidence in suppliers’ project plans and encourage investors and lenders to provide funds. All of these requirements can be met if a large-scale voluntary carbon market is carefully developed.

A fresh action plan is required to scale up voluntary carbon markets and a multi-pronged strategy would be required to establish a viable voluntary carbon market.

In its analysis, the TSVCM identified six areas along the carbon-credit value chain where action may help the voluntary carbon market scale up.

1. Creating standardized criteria for finding and verifying carbon credits

Because carbon credits are so varied, the voluntary carbon market presently lacks the liquidity needed for effective exchange. Each credit is related to the underlying project in some way, such as the type of project or the area in which it was completed.

Because buyers assess additional features differently, these variables influence the credit’s cost. Overall, credit irregularity indicates that linking a single buyer with a corresponding provider is a time-consuming, inefficient over-the-counter procedure.

If all credits could be established using identical qualities, buyer-supplier matching would be more efficient. The first set of qualities is concerned with quality. The quality criteria specified in the “core carbon principles” would serve as the framework for assessing whether carbon credits represent genuine emissions reductions.

The second set of attributes would cover the additional properties of the carbon credit. Standardizing such characteristics in a unified taxonomy will aid suppliers in marketing credits and consumers in identifying credits that meet their needs.

2. Getting contract with Standardized terms

Because of the diversity of carbon credits available in the voluntary carbon market, particular types of credits are exchanged in quantities too small to provide meaningful daily price signals. Making carbon credits more consistent would concentrate trade activity on a few types of credits while also boosting market liquidity.

Following the establishment of the aforementioned fundamental carbon principles and standard features, exchanges may create “reference contracts” for carbon trading. A core contract based on fundamental carbon ideas would be included, with further features specified and paid individually according to a standard taxonomy. Core contracts would make it easier for corporations to purchase large quantities of carbon credits at once: they could bid on credits that met certain criteria, and the market would aggregate smaller quantities of credits to meet their bids.

Another advantage of reference contracts is the ability to maintain a constant daily market price. Even if reference contracts are developed, many parties will continue to deal over the counter (OTC). Prices for credits traded via reference contracts might serve as a starting point for OTC trade talks, with other characteristics priced separately.

3. Setting up trading and post-trade infrastructure

A strong, adaptable infrastructure would enable the voluntary carbon market to function smoothly, allowing for high-volume listing and trading of reference contracts as well as contracts with a limited, regularly stated set of additional characteristics. As a consequence, project developers would benefit from the creation of structured finance solutions.

It is also necessary to have post-trade infrastructure such as clearinghouses and meta-registries. Clearinghouses would aid in the development of a futures market while also protecting against counterparty default. Meta-registries would provide buyers and suppliers with custodial services and enable the creation of consistent issue numbers for specific projects (similar to the International Securities Identification Number, or ISIN, in capital markets).

A robust data infrastructure would also increase the transparency of reference and market data. All environmental and financial markets need sophisticated and up-to-date information. Due to restricted data availability and the difficulties of following the OTC market, transparent reference and market statistics are currently unavailable. Buyers and suppliers would benefit from new reporting and analytics services that combine freely accessible reference data from multiple registries via APIs.

4. Getting a common consensus on Carbon Credits

Credits are viewed with skepticism in the context of decarbonization. Some experts are skeptical that businesses will reduce their own emissions much if they had the option of offsetting emissions instead. As part of a wider effort to attain net-zero emissions, businesses would benefit from clear guidance on what constitutes an environmentally efficient offsetting plan. Carbon credit principles would help to ensure that carbon offsetting does not preclude other efforts to decrease emissions and resulting in greater carbon reductions than would otherwise occur.

In accordance with such rules, a company would first calculate its need for carbon credits by disclosing its overall greenhouse-gas emissions, as well as its goals and methods for reducing emissions over time. To compensate for emissions from sources that it can eventually eliminate, the company may purchase and “retire” carbon credits (claiming the reductions as their own and withdrawing the credits from the market, so that another organization cannot claim the same reductions). It may also use carbon credits to offset “remaining emissions” that it will be unable to eliminate in the future.

5. Ensuring Market Integrity

Concerns regarding the integrity of the voluntary carbon market stymie its spread in a number of ways. For starters, the varied nature of credit increases the likelihood of errors and fraud. Money laundering is also a possibility due to the market’s lack of pricing transparency.

One corrective measure would be to implement a computerized system for project registration, credit verification, and issue. Verification organizations should be able to track a project’s impact on a regular basis, not only at the end. A digital approach may minimize issuance costs, shorten payment times, accelerate credit issuance and cash flow for project developers, allow credits to be traced, and boost the credibility of corporate offset claims.

Other upgrades would include the implementation of anti-money-laundering and know-your-customer regulations to prevent fraud, as well as the formation of a regulatory body to check market participants’ eligibility, regulate their behavior, and oversee the market’s operation.

6. Building Demand

Finding an effective way for carbon credit buyers to express their future needs will help incentivize project developers to increase carbon credit supply. Long-term demand signals might include promises to reduce greenhouse gas emissions or upfront agreements with project developers to acquire carbon credits from future developments. To measure medium-term demand, a registry of commitments to purchase carbon credits may be utilized.

Consistent, widely accepted guidelines for companies on acceptable uses of carbon credits to offset emissions; increased industry-wide collaboration, in which consortiums of companies align their emissions-reduction goals or establish shared goals; and improved standards and infrastructure for the development and sale of consumer-oriented carbon credits are all possible ways to promote demand signals.

To keep global warming to 1.5 degrees Celsius, net greenhouse-gas emissions must be reduced quickly and significantly. While companies and other organizations may achieve the majority of the needed reductions by implementing new technologies, energy sources, and operating techniques, many will need to supplement their own abatement efforts with carbon credits in order to achieve net-zero emissions. A strong, well-functioning voluntary carbon credit market would make it easier for companies to locate reputable carbon credit suppliers and execute transactions on their behalf.

Furthermore, such a market would be capable of communicating signs of buyer interest, motivating suppliers to increase credit supply. A voluntary carbon market would speed up the transition to a low-carbon future by allowing for more carbon offsetting.

The EU is proposing a new carbon pricing plan that will impact the price of carbon emissions, specifically in the transport sector.

Legislation in the EU is being drafted to accomplish the goal of being carbon neutral by 2050. To accomplish this goal, the EU is seeking a 90% reduction in transport emissions by 2050.

Solutions for Shipping

Alternative methods of transport and fuels will be provided to member states to reduce emissions. The EU mentions multimodal transport as a solution. This results in multiple transport avenues such as railways or waterborne transport for goods to move within the union.

As a result, these trade routes can be simplified and optimized in a way that keeps pollution to a minimum.

There is staunch opposition from shipping companies, as green alternatives to current fuels such as renewable hydrogen or ammonia are not incentivized in the deal. Rather, the EU is incentivizing using natural gas as a fuel source, which can be considered toxic if fuel spills are to occur.

Inland Waterways – the Future?

According to the EU, inland waterways account for 17% of the emissions that road transport uses and 50% of the emissions railways use. Inland Waterways would decrease carbon pollution, while also decongesting many high traffic land routes.

Noise pollution is also a factor that would decrease with increased shipping through inland waterways.

The federal government has rejected a request from Saskatchewan to use a provincial carbon pricing plan.

Saskatchewan premier Scott Moe has opposed the federal carbon price, feeling it puts a strain on an uncompetitive economy in Saskatchewan. In a statement released by the premier, Moe states “The rejection of Saskatchewan’s submission can only be viewed as an arbitrary and political decision from the federal government.”

Moe also indicated that the federal government will not accept any further submissions of a carbon pricing plan until 2023.

The Saskatchewan rejection contrasts with the carbon pricing plan approved in New Brunswick, which provides reduced fuel prices in exchange for a carbon tax.

The move shows the Canadian governments commitment to uniting carbon taxes across the whole country, rather than letting provinces decide how they should implement carbon measures. The federal government mentioned a benchmark carbon price is in the works and could be implemented as early as January 2023.

Minister of Environment and Climate Change Jonathan Wilkinson did mention previously that the new benchmark would eliminate any rebates or cuts offsetting the carbon tax.

Canada aims to be carbon neutral by 2050, they have also been tasked by the UN to reduce emissions from 40-45% by 2030. A change in carbon pricing methods could eliminate any discrepancies and help Canada reach their Net-Zero goals.

So what is a Carbon Offset and why do entities buy them?

In recent years, global climate change has driven interest in carbon offsetting as a way to reduce greenhouse gas emissions.

A carbon offset is a way to balance out the carbon emissions you produce by investing in projects that reduce emissions elsewhere.

But what exactly is a carbon offset, and how does it work? In this article, we’ll explore the basics of carbon offsets, how they are created, the types of projects they support, and how investors can get involved.

Buying a carbon offset or credit is the right thing to do for the planet. Offsets do not simply kick the global warming can down the road: They create a way to buy their way into the problem, not out of it.

Offsets can trade in the compliance markets (like those from the Clean Development Mechanism or Joint Implementation projects). However, the majority are traded in the voluntary markets.

Carbon offsets can also have co-benefits such as job creation, water conservation, flood prevention and preservation of biodiversity.

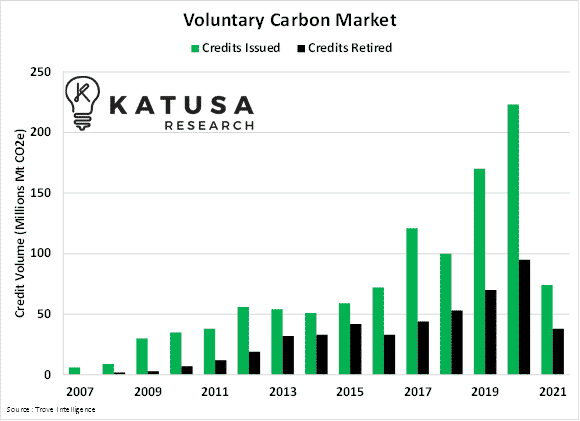

Below is a chart which shows the annual credit generation from carbon offset projects in the voluntary carbon market. In 2020, annual credit production in the voluntary carbon market was a record 223 million.

Courtesy of: Katusa Research

How Offsets are Created

Carbon offsets are created through the development of projects that reduce greenhouse gas emissions or remove carbon from the atmosphere.

One of the most common ways to create carbon offsets is to support renewable energy projects such as wind or solar power.

When you invest in these projects, you are helping to reduce the amount of greenhouse gases released into the atmosphere, which in turn can help to mitigate climate change.

Other carbon offset projects might include reforestation efforts, methane capture from landfills, or energy efficiency improvements.

A portion of offset spending also goes toward investing in futuristic technology for carbon sequestration and emissions mitigation. Many methods of carbon offset creation, like direct air capture, are in the very incipient stages of development. Increasing demand for those novel offset types enables large-scale deployment, rapidly making them more economical.

Eventually, new technologies will reach a tipping point. For example, Prometheus’s forges are expected to remove 11 GT of CO2 from the air each year by 2050.

That’s the equivalent of 20% of current emissions, all from a single company.

And it’s only possible with heavy, ongoing investment in carbon credits and offsets—even “risky” ones.

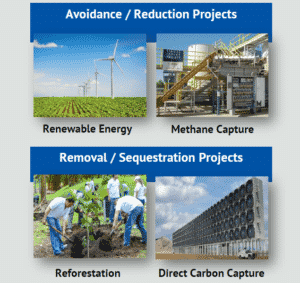

Types of Carbon Offset Projects

Carbon offset projects are grouped into 2 categories:

Avoidance/Reduction projects like renewable energy (wind, solar) and methane capture

Removal/Sequestration Projects like reforestation and direct carbon capture

The physical cost of offsetting incentivizes the companies to identify operational “leaks”—areas where emissions can be reduced or eliminated—then begins to force the company to eliminate emissions throughout their entire value chain.

Companies that use offsets at least in part to manage their emissions implement emissions reductions at a higher rate, spend almost five times as much on reductions, and mitigate or eliminate a greater proportion of their emissions as those that do not use offsets.

Investing in offsets also helps the earth through the offsets themselves. Reforestation increases biodiversity, and the installation of solar panels and wind turbines pulls energy demand away from coal and fossil fuel supplies.

A carbon offset can be resold multiple times but once retired, it can no longer be resold. To ensure there is no double-sale, a carbon offset must be kept on a registry. This registry keeps track of the issuance and retirement of offsets.

Carbon Offsets Investing

Investing in carbon offsets can be a way to both reduce your carbon footprint and support sustainable development around the world.

When you invest in a carbon offset project, you are essentially purchasing a credit that represents the amount of greenhouse gas emissions that have been reduced or removed.

These credits can then be sold or traded on carbon markets, or used to offset the emissions of a particular activity (like air travel or shipping). The price of carbon offsets can vary depending on the type of project and the structure of the market, but in general, they are a cost-effective way to support climate action.

Investing in carbon offsets—whether for better financing terms or to help prevent further climate change—encourages competitors in the marketplace to do the same.

Etsy, the online market for handcrafted goods, purchased high-quality carbon offsets for all of its competitors for a single day, and committed to offsetting its own carbon footprint in the future. It calculated the total cost of doing so at just a penny per package, proving that it’s an expense every other retailer can afford to bear.

Demonstrating the economic feasibility of emissions mitigation encourages other companies to do it, even if it’s for a reason other than saving the planet.

In fact, it may be a combination of all of these reasons and more: creating a more resilient supply chain, improving supplier relationships, and increasing employee retention are all co-benefits of purchasing carbon credits and carbon offsets, ensuring your company can thrive forever.

At their core, both carbon credits and carbon offsets are accounting mechanisms. They provide a way to balance the scales of pollution. The big idea behind credits and offsets is that since CO2 is the same gas anywhere in the world, it doesn’t matter where emissions reduction happen.

For both consumers and companies, it makes financial sense to reduce emissions where it is cheapest and easiest to do so, even if that does not involve their own operations.

Offset and Credit Similarities

At the simplest level, a carbon credit or offset represents a reduction in or removal of greenhouse gas (GHG) emissions that compensates for CO2 emitted somewhere else. The instruments do have two major attributes in common:

One carbon credit or offset equals one tonne of carbon emissions.

Once a carbon credit or offset is purchased and the CO2 is emitted, that credit is “retired” and cannot be sold or used again.

Carbon Offsets and Carbon Credits Defined

While the terms “carbon credits” and “carbon offsets” are often used interchangeably, they refer to two distinct products that serve two different purposes. Before you begin purchasing either, it’s important to understand the difference between the two and which one will help you meet your goals. Here is a broad definition of the terms:

Carbon offset: A removal of GHGs from the atmosphere.

Carbon credit: A reduction in GHGs released into the atmosphere.

To help visualize the difference, imagine a water supply polluted by a nearby chemical plant. A “chemical offset” would mean pulling chemicals out of the water to help purify it. A “chemical credit” would mean paying another chemical company to release fewer chemicals into the water, so the overall level of pollution stays the same. Clear as mud? Great.

A Carbon Offset and Carbon Credit Primer*

Let’s dive a bit deeper into these products one at a time. Creating a carbon offset involves a fancy term we call “carbon sequestration.” Recall how a judge can order a jury to be sequestered—meaning they have to be sealed off from the outside world.

It works the same way with carbon: offsets involves CO2 emissions pulled out of the atmosphere and locked away for a period of time.

There is a growing list of ways to do this, including planting forests, blasting rock into tiny pieces, storing carbon in manufactured devices, capturing methane gas at a landfill, and the holy grail of carbon sequestration: using sophisticated technology to turn CO2 emissions into a usable product.

Carbon offsets are produced by independent companies that pull CO2 emissions from the atmosphere. The offsets are then sold to companies that emit (or have emitted) CO2. In a sense, offset-producing companies are directly funded by those companies that emit GHGs.

Carbon credits, on the other hand, are generally “created” by the government. Governments limit the amount of GHGs organizations can emit by placing a cap on them—a specific number of tons of CO2 the company can emit. Each of those tons are referred to as a carbon credit.

Companies comply with that cap by reducing the emissions produced in their operations through improving energy efficiency or switching to renewable energy sources. An organization that brings its overall emissions below what is required by law can sell the excess credits to businesses that are unable or unwilling to cut their own emissions to become compliant.

There are a few other ways to produce carbon credits. For more detail, see our article on carbon credits.

The Two Carbon Markets

There’s one more important distinction between carbon credits and carbon offsets:

Mandatory schemes limiting the amount of GHG emissions grew in number. And with them, a fragmented carbon compliance market is developing. For example, the EU has an Emissions Trading System(ETS) that enables companies to buy carbon credits from other companies.

California runs its own cap-and-trade program. Nine other states on the eastern seaboard have formed their own cap-and-trade conglomerate, the Regional Greenhouse Gas Initiative.

The voluntary carbon market (think: offsets) is much smaller than the compliance market, but expected to grow much bigger in the coming years. It is open to individuals, companies, and other organizations that want to reduce or eliminate their carbon footprint, but are not necessarily required to by law.

Consumers can purchase offsets for emissions from a specific high-emission activity. An example would be a long flight. Or they can buy offsets on a regular basis to eliminate their ongoing carbon footprint.

Do I Need Carbon Offsets or Carbon Credits?

Now that you know their differences and what they have in common, here’s how carbon credits and carbon offsets work in the grand, global scheme of emissions reduction.

The government is putting heavy caps on GHG emissions, meaning that companies will have to reconfigure operations to reduce emissions as much as possible. Those that cannot be eliminated will have to be accounted for through the purchase of carbon credits. Ambitious organizations, corporations, and people can purchase carbon offsets to nullify previous emissions or to reach net zero.

So which do you need? If you’re a corporation, the answer is likely “both”—but it all depends on your business goals. If you’re a consumer, carbon credits are likely unavailable to you. But you can do your part by purchasing carbon offsets.

Returning to the illustration from earlier, our vital, global goal is to both stop dumping chemicals into the metaphorical water supply, and to purify the existing water supply over time. In other words, we need to both drastically reduce CO2 emissions. And then we work to remove the CO2 currently in the atmosphere if we want to materially reduce pollution.

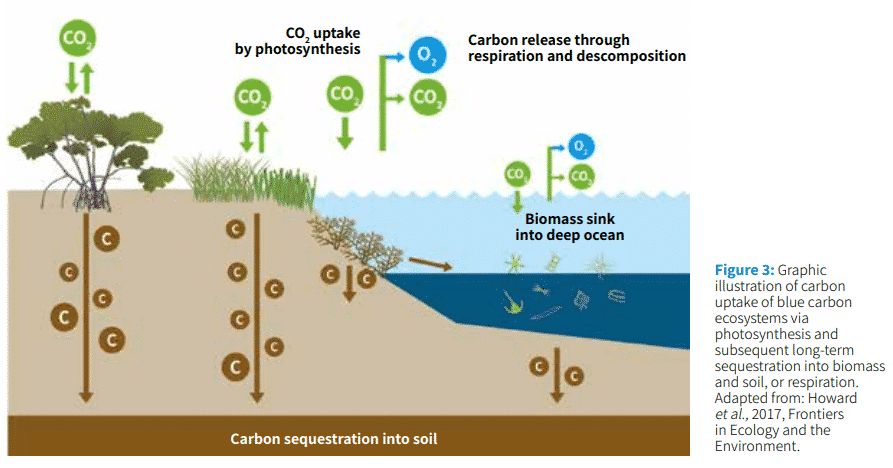

Blue carbon credits are created by the growth and conservation of carbon-absorbing plants, such as mangrove forests and their associated marine habitat.

Blue Carbon refers to the carbon stored in coastal ecosystems like mangroves, seagrasses, and salt marshes.

These ecosystems cover just 1% of the ocean floor but can store up to 10 times more carbon per unit area than terrestrial forests.

Blue Carbon is so-called because it is stored in marine or coastal living organisms and the sediments beneath them.

Blue Carbon ecosystems are vital for the health of our planet. They not only store carbon but also provide essential services such as water purification, coastal protection, and habitat for marine life.

Over the past decade scientists have discovered that seagrass meadows, tidal marshes and mangrove forests are among the most intensive carbon sinks in the world. This means blue carbon offsets can remove enormous amounts of greenhouse gases.

A blue carbon offset project should have its carbon credits trade at a premium.

This is because of the large positive second-order effects such as the positive effects on corals, algae, and marine biodiversity (e.g. sharks, whales, sea turtles) that have been so negatively impacted by activities such as over-fishing and farming.

Mangroves Store 10x more carbon than terrestrial forests (Source: Kauffman et al, 2018)

Yes, forests can grow in the ocean. Examples include the mangrove forests in sea bays, such as Magdalena Bay in Baja California Sur, Mexico.

Image: MarVivo Magdalena Bay Project

Mangroves are trees (about 70 percent underwater, 30 percent above water) that have evolved to be able to survive in flooded coastal environments where sea water meets fresh water and the resulting lack of oxygen makes life impossible for other plants.

Mangroves cover just 0.1% of earth’s surface (Source: FAO, 2003)

Mangrove trees create shelter and food for numerous species such as sharks, whales, and sea turtles. Mangrove forests are a valuable marine ecosytem.

Second Order Effects of Blue Carbon Credits

Other positive second-order effects of mangrove forests include their importance as a pollution filter, reducing coastal wave energy and reducing the impacts from coastal storms and extreme events. Blue carbon systems trap sediment which support root systems for plants. This accumulation of sediment over time can enable coastal habitats to keep pace with rising sea levels.

All this can be calculated into insurance premiums, and lower-cost premiums are good for business and residents. These are all free second-order effects. To put it in perspective, natural disasters and extreme weather events created over $270 billion worth of economic losses in 2020. It is absolutely in the best interest of citizens and insurance companies to mitigate the effects of climate change.

Coastal wetlands and mangrove forests will become an ever-increasing sector for carbon credit generation. That is because mangrove forests and coastal wetlands sequester carbon at a rate that is up to ten times greater than mature tropical forests.

Because the carbon is sequestered and stored below water in aquatic forests and wetlands, it is stored for more than ten times longer than in tropical forests.

The significant positive second-order effects attributed to each blue carbon credit are why many investors believe it will trade at a premium to other carbon credits.

Blue Carbon and the Food Footprint

There is a land-use carbon footprint of 1440 kg CO2e for every kilogram of beef and 1603 kg CO2e for every kilogram of shrimp produced on lands formerly occupied by mangroves. A typical steak and shrimp cocktail dinner would burden the atmosphere with 816 kg CO2e.

It is estimated that over 1 billion tons of carbon dioxide is released annually from degraded coast ecosystems.

There are around fourteen million hectares of mangrove aquaforests on earth today and they’re under attack by the deforestation practices caused by intense shrimp farming

Are the shrimp you eat part of the problem? Soon, these shrimp will be labeled, and consumers will know and be required to cover the offset costs for the environmental damage.

To put things into perspective, 14 million acres of wetlands will absorb as much carbon out of the atmosphere as if all of California and New York State were covered in Tropical Rainforest.

Think of Blue Carbon as the “high grade” gold mine at the surface.

With the economic value of Blue Carbon credits and the technology that will enable Carbon Rangers to preserve forests and wildlife, expect entrepreneurs to expand the Carbon Ranger program to mangrove forests across the globe. This will be a step forward and a small part of solving the climate emergency.

These are just a few of the examples of how carbon credits will be created to enhance stakeholder capitalism.

Oceanic Blue Carbon

In addition to coastal blue carbon mentioned above, Oceanic blue carbon is stored deep in the ocean within phytoplankton and other open ocean biota.

The infographic below shows the typical blue carbon ecosystem

Source: Natural Carbon Sinks: Blue Carbon ecosystems in climate change mitigation, 2021

There are many factors that influence carbon capture by blue carbon ecosystems. These include:

Location

Depth of water

Plant species

Supply of nutrients

Improving blue carbon ecosystems can significantly improve the livelihoods and cultural practices of local and traditional communities. In addition, restoring blue carbon regions provides enormous biodiversity benefits to both marine and terrestrial species.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy