The upcoming 2024 US election will have significant implications for the country’s climate and energy policies. While the federal government’s stance on clean energy might see changes depending on who takes office, state-level elections could also influence how much progress is made toward the country’s climate goals.

As both Democrats and Republicans gear up for the election, their different approaches to clean energy and climate initiatives highlight how the nation’s renewable energy future could unfold.

Federal Climate Policy: The Role of the Inflation Reduction Act (IRA)

President Joe Biden’s administration made a significant impact on US climate policy by introducing the Inflation Reduction Act (IRA). It is a $1.2 trillion law aimed at bolstering clean energy and reducing carbon emissions. The future of this policy could vary significantly depending on the results of the presidential election in November 2024.

If Vice President Kamala Harris takes the White House, experts predict a continuation of the Biden administration’s focus on implementing and defending the IRA. This would include further efforts to:

- promote clean energy incentives,

- support infrastructure projects, and

- ensure that businesses and communities benefit from the law’s financial provisions.

However, if Donald Trump wins the presidency, the IRA could face significant challenges. A Trump-led administration might attempt to reduce or eliminate some of the IRA’s key climate provisions. It may potentially reallocate funds to other priorities, such as extending Trump-era tax cuts.

However, experts believe a full repeal of the IRA is highly unlikely, even if Republicans gain control of both the House and Senate. The GOP may instead focus on modifying parts of the IRA, such as the $7,500 electric vehicle tax credit, which has been a target for criticism by Republican lawmakers.

Experts predict that, regardless of who wins the presidency, there will be efforts to address critical issues such as mineral supply chains. These are essential for the production of clean energy technologies like batteries and electric vehicles.

A narrowly divided Congress, coupled with slim majorities, would make it difficult for either party to implement sweeping changes to energy policy. Instead, smaller legislative actions, such as incentives for critical mineral production or investments in infrastructure for clean energy, are more likely to gain bipartisan support.

What a Harris Administration Could Mean for Clean Energy

If Kamala Harris wins the presidency, her administration will likely continue Biden’s focus on implementing the IRA’s provisions while addressing broader fiscal issues such as the national debt and tax policy. In this scenario, there would be a strong emphasis on capital formation, community engagement, and workforce development in clean energy sectors.

The Department of Energy (DOE), which has transitioned from a primarily research-focused agency to one responsible for deploying clean energy technologies, would play a critical role in Harris’ energy policy.

However, a Harris administration would likely face challenges in advancing new energy legislation, even if the Democrats secure slim majorities in Congress. As Mary Anne Sullivan, senior regulatory counsel at Hogan Lovells, suggests, sweeping new climate policies are unlikely to be Harris’ top priority. Instead, Democrats would likely concentrate on defending and optimizing the IRA rather than pursuing significant new initiatives.

Trump Administration’s Potential Approach to Energy Policy

If Donald Trump returns to the White House, his administration would likely target the IRA for modifications. This is especially true in the case of provisions related to clean energy tax incentives and electric vehicles.

However, wholesale repeal of the law remains improbable due to political and economic constraints. Republican lawmakers have already expressed caution about dismantling the IRA too aggressively, given the law’s role in spurring private sector investment in energy projects.

Additionally, a second Trump administration could adopt a more aggressive stance on mineral extraction, particularly for resources critical to clean energy technologies like lithium, cobalt, and rare earth elements. This focus on domestic resource extraction aligns with the GOP’s broader strategy to boost energy independence and reduce reliance on foreign minerals.

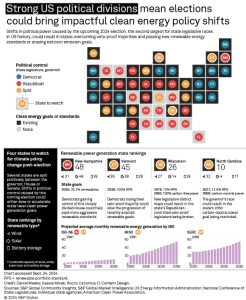

State-Level Elections: A Key Driver for Clean Energy Progress

While much attention is focused on the federal election, state-level elections will play an equally crucial role in determining the trajectory of US climate policy. The 2024 election is expected to be one of the largest in US history for state legislative races. It will have over 6,000 seats up for grabs.

Many of these states have renewable portfolio standards (RPS) or net-zero emission goals, which are often closely tied to which party controls the state legislature and governorship.

States with Democratic trifectas—where the party controls both legislative chambers and the governorship—are more likely to advance clean energy initiatives. These include raising renewable energy targets and passing new climate legislation.

However, states controlled by Republican trifectas tend to leave decisions about energy generation to utility companies and market forces, often leading to slower progress on clean energy goals.

Key States to Watch

Several states are expected to see potential shifts in political control, which could significantly impact their clean energy policies. These include New Hampshire, North Carolina, Vermont, and Wisconsin.

New Hampshire’s Republican-controlled legislature has slowed clean energy development, but a political shift could push for stronger renewable targets. In North Carolina, the governor’s race could impact the state’s 2050 carbon-neutral goal. Vermont’s 100% RPS by 2035 might face challenges if its Democratic supermajority weakens, while Wisconsin’s redistricting could reduce Republican dominance over energy policies.

A Pivotal Moment for US Climate Policy

Regardless of the election outcome, the transition to clean energy is likely to continue, driven by market forces, private sector investments, and bipartisan support for critical mineral production. However, the pace and scale of that transition will be heavily influenced by the results of federal and state elections. Thus, this election will be a pivotal moment for US climate policy.

")

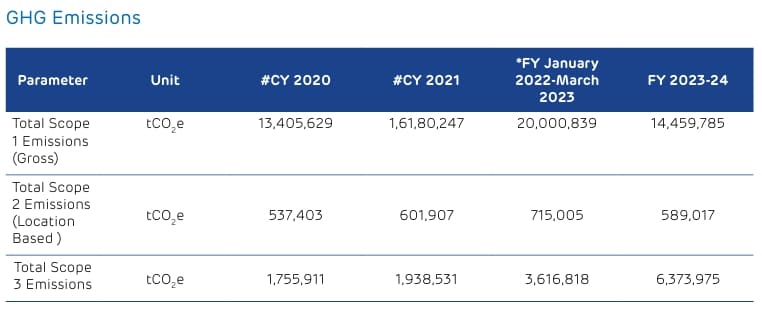

Source: Ambuja Cements

Source: Ambuja Cements Source: Ambuja Cements

Source: Ambuja Cements

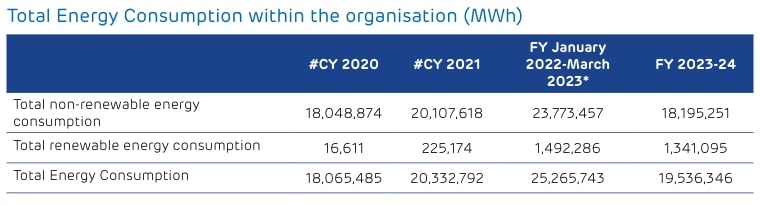

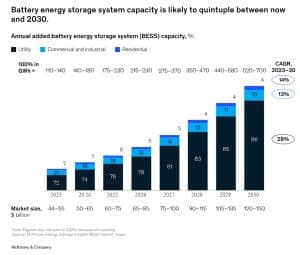

Source: McKinsey

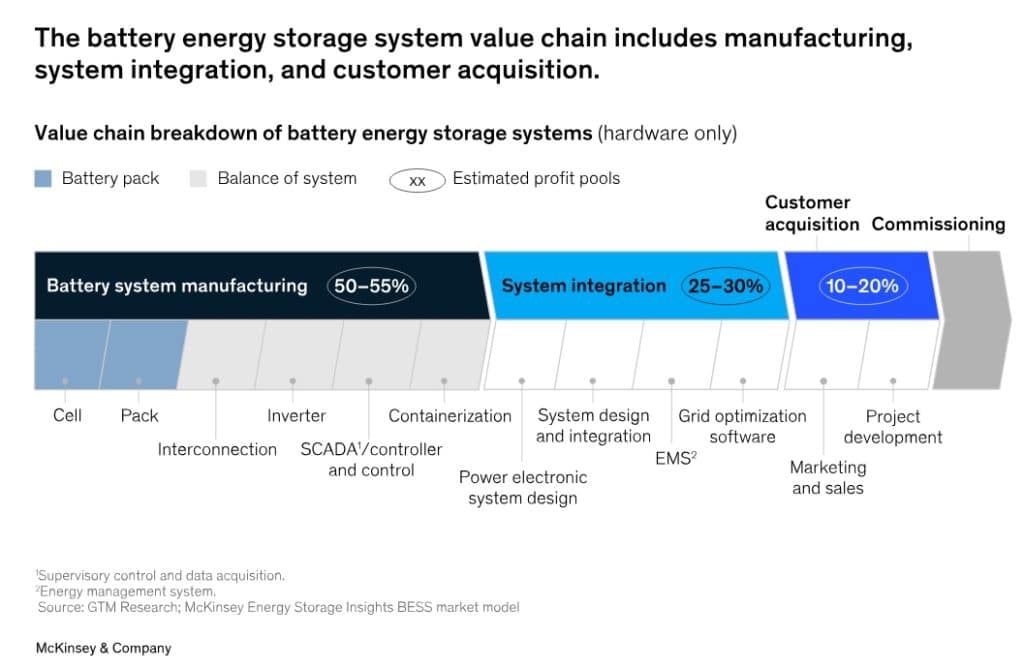

Source: McKinsey

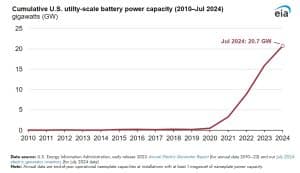

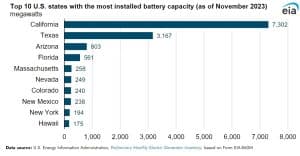

Source: EIA

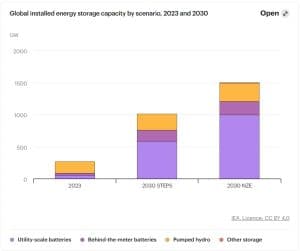

Source: EIA