The United States’ goal to break China’s grip on the global supply of rare earth minerals faces numerous hurdles. In a remote field outside Houston, Texas, plans are in place for a rare earth processing plant by Lynas Rare Earths, an Australian company.

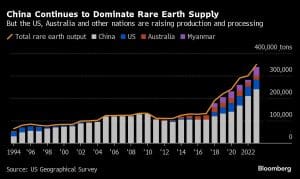

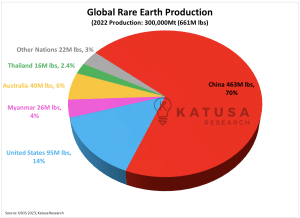

Despite its potential significance, this plant is just one step in the US’s larger, multibillion-dollar effort to challenge China’s monopoly, which controls roughly 70% of the world’s rare earth output and over 90% of its refining capacity.

US Investment: Slow Progress in a High-Stakes Race

Rare earth elements are essential components in various high-tech applications like smartphones, wind turbines, and military equipment.

The Texas plant, set to be built by Lynas, is part of a growing US initiative to reduce reliance on China for rare earths. For the 149-acre (60 hectares) site, Lynas has secured more than $300 million in contracts from the Pentagon. If all goes according to plan, this facility will be operational within 2 years, contributing significantly to the US’s rare earth processing capacity.

This plant represents just a fraction of the billions of dollars in subsidies and loans pledged by the US and its allies to foster domestic rare earth production. The American government has increasingly viewed the development of a domestic rare earths supply chain as a matter of national security. It aims to break China’s near-total control over refining and production.

- RELATED STORY: China’s Grip On Rare Earth Elements Loosens

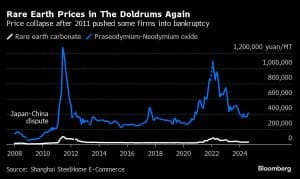

However, while the intention is clear, market conditions present a significant challenge. Since 2022, the global prices for rare earth elements have slumped. This is primarily due to an increase in supply from China and a slowdown in its domestic economy.

This decline has raised doubts about the long-term financial viability of many new projects outside China. Thus, the prospect of establishing a robust, independent supply chain remains uncertain.

Market Volatility Threatens New Rare Earth Ventures

Despite global demand for rare earth elements, their extraction and processing remain fraught with economic and environmental challenges. Rare earths are not truly “rare” but are seldom found in concentrations high enough to justify environmentally intensive mining operations.

There are 17 chemically related elements in this category, each with properties critical to manufacturing electronics, renewable energy components, and defense technology.

Current market conditions pose a threat to new entrants. According to MP Materials Corp., which operates the only rare earth mine in the US and is building a factory to manufacture magnets in Texas, CEO James Litinsky:

“These market conditions have now destroyed most of the hoped-for projects from just a couple of years back.”

However, even with domestic mining in place, refining and processing are still predominantly under Chinese control, underscoring the dominance of China’s supply chain.

In the face of these market challenges, Laura Taylor-Kale, the US Assistant Secretary of Defense for Industrial Base Policy, promised earlier this year that the US would establish a “sustainable mine-to-magnet supply chain capable of supporting all US defense requirements by 2027.”

- She further highlighted that the Lynas project in Texas could produce around 25% of the world’s supply of rare earth oxides once operational.

China’s Dominance: Strategic Price Manipulation at Play

China’s control over the rare earth market stems from its aggressive mining and refining activities, supported by government policies. Per Katusa Research report, the country merged its 5 largest producers into a single entity, further tightening its grip on the world’s rare earth supply.

The Chinese Ministry of Natural Resources, along with its industry ministry, raised mining quotas for rare earths in 2023 and 2024, driving down global prices and applying further pressure on competing projects. The result has been a market environment in which many rare earth mines struggle to break even, forcing early-stage projects into delays and funding shortfalls.

The current situation has echoes of past geopolitical maneuvers. In 2011, China temporarily cut off rare earth supplies to Japan over a territorial dispute. This move pushed Japan to seek diversification in its rare earths supply chain, eventually investing in Lynas. The event shows how geopolitics and market control can intersect in ways that significantly impact global supply chains.

Despite securing substantial investments, some rare earth projects outside China are already encountering setbacks. Arafura Rare Earths is one such company. It received an A$840 million (approximately $560 million) loan from the Australian government and signed agreements with two Korean auto firms in 2022 to supply rare earths from its Nolans project in Australia.

However, construction has yet to begin, largely due to funding gaps. CEO Darryl Cuzzubbo mentioned that while debt and approvals are in place, the “one missing piece is the equity.” The company aims to secure half of the required equity from cornerstone investors before turning to the broader market for the remaining funds. Cuzzubbo hopes to finalize the equity by the end of the year to start construction in early 2025.

The Key to Rare Earth Supply Chain Independence

Japan’s experience offers critical insights into the complexities of establishing an independent rare earth supply chain. Following China’s 2011 export restrictions, Japan invested $250 million in Lynas, allowing the company to start trial production two years later.

However, it took Lynas until 2018 to become profitable, highlighting the extended timeline and considerable financial backing required for such projects.

Lynas CEO Amanda Lacaze emphasized the need for “patient capital” when venturing into the rare earths market. This is particularly true for projects breaking new ground. Recent delays with the Texas facility due to issues with wastewater permits highlights the obstacles facing new rare earth projects in the West.

The US’s push to build a competitive rare earths supply chain faces headwinds in both market conditions and geopolitical maneuvering. As the global rare earth prices slump and China’s strategic control persist, the development of a robust, independent supply chain remains an uncertain endeavor. The Western world’s goal of building a competitive supply chain will require not just investment but strategic patience and international cooperation.

source: LiFT –

source: LiFT –  source: LiFT

source: LiFT