Google has taken a bold step in the fight against climate change, signing a groundbreaking deal to purchase 100,000 tons of carbon removal from Tennessee-based startup Holocene. The $10Mn direct air capture (DAC) offtake agreement, set for delivery by 2030, establishes a record-low price of $100 per ton for carbon removal credits. This deal is expected to play a pivotal role in reducing the cost of DAC technology which has gained significant attention in global net zero goals.

Big Value, Small Price: What’s Inside Google’s $100 Price Tag

Achieving a price of $100 per ton for DAC removal is no small feat. Google made this possible by committing to an upfront payment, which provides Holocene with the necessary capital to scale its operations. But that’s not the only factor driving down costs.

The U.S. government’s 45Q tax credit, resulting from the Inflation Reduction Act, has been instrumental. This tax credit offers up to $180 per ton of carbon removed, providing a crucial financial incentive for companies like Holocene to invest in carbon capture technology.

Despite the optimism, Holocene has yet to deliver carbon removal on a large scale. The company only recently launched its first pilot plant in May 2024, which captures 10 tons of CO2 annually. Still, Holocene is confident that its innovative approach, coupled with Google’s financial backing, will enable it to meet the ambitious 100,000-ton target by the early 2030s.

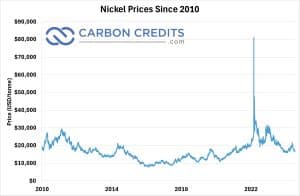

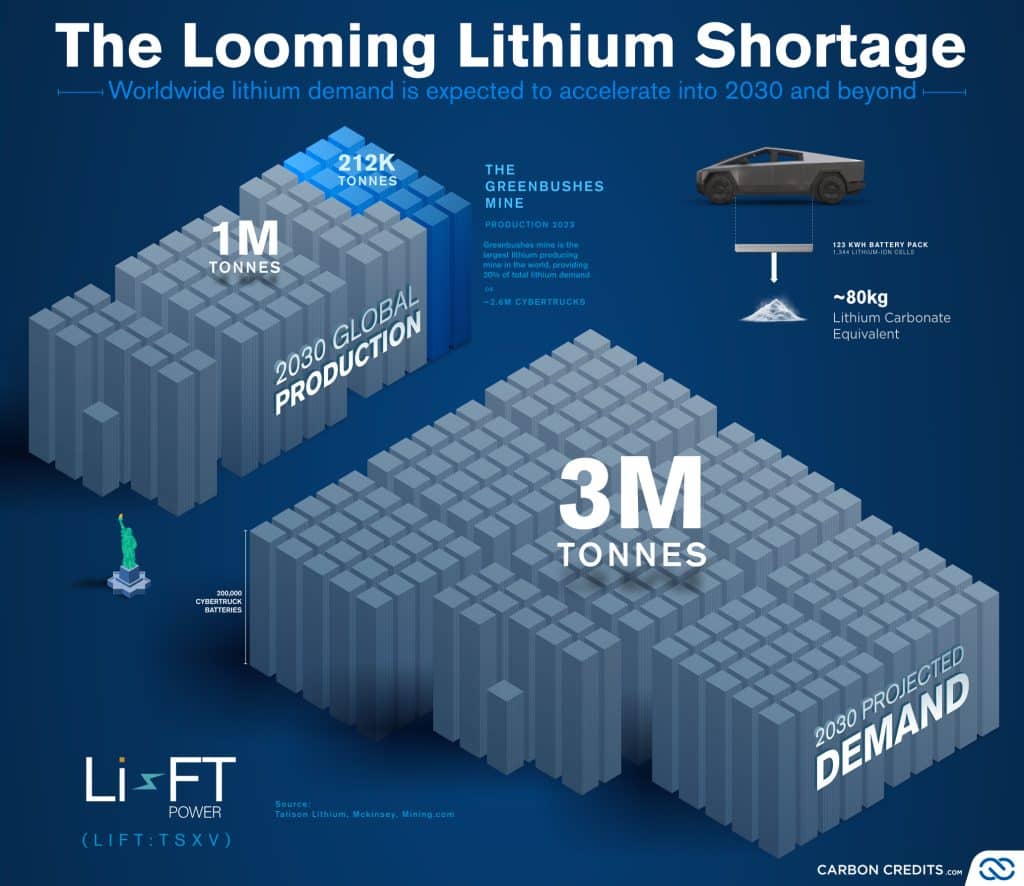

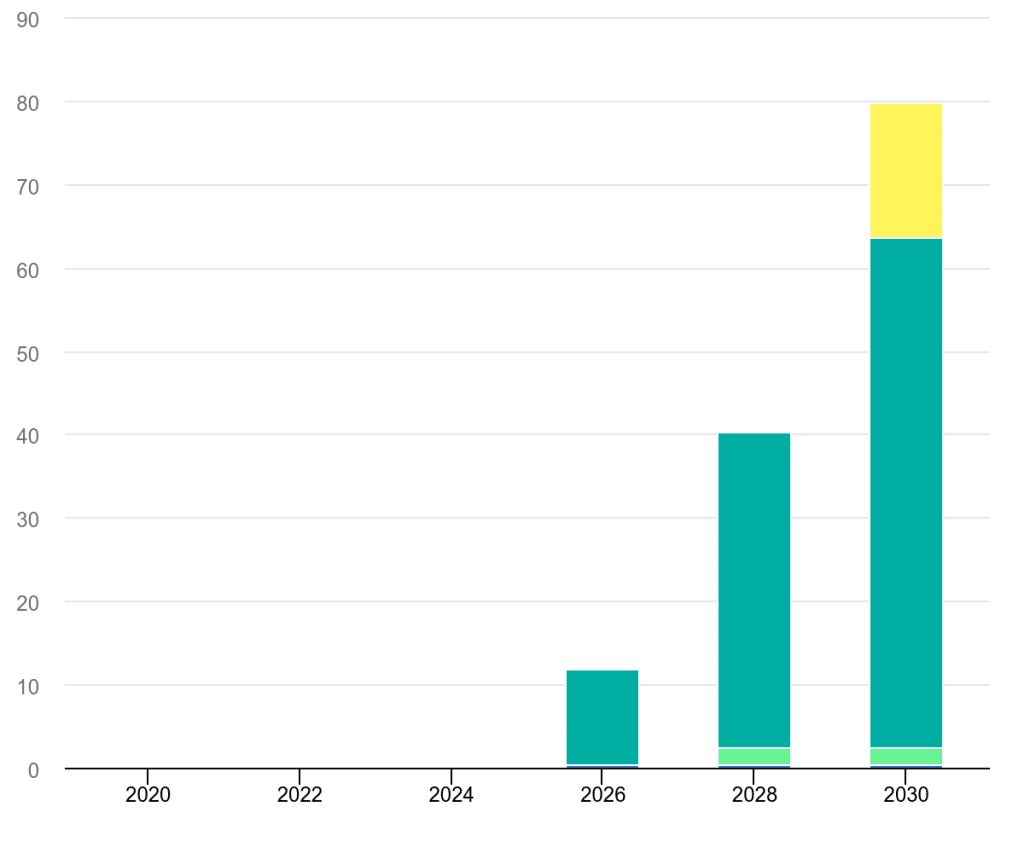

The Looming Lithium Shortage

Worldwide lithium demand is expected to accelerate into 2024 and beyond.

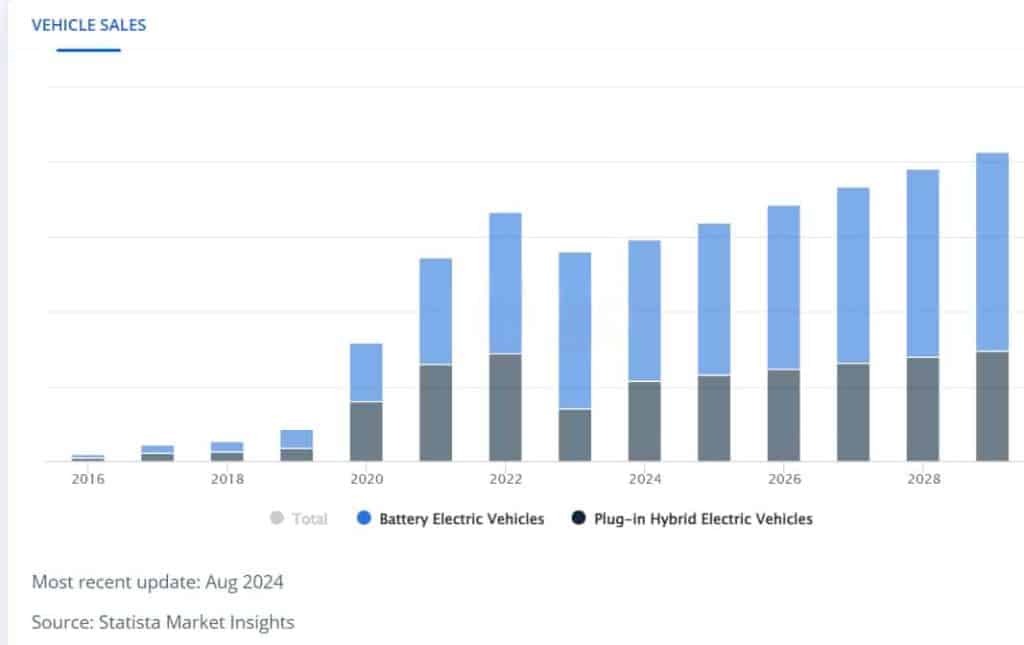

EV sales are still growing every year. Automobile manufacturers have sold more EVs in 2024 than ever. And to power these electric vehicles, you need lithium for batteries that provide consistent, long range. Lithium production is starting to pick up again, and that has contributed to lower prices. The energy transition is happening. And no one can stop it.

Learn why investing in lithium explorers and producers looks promising >>

Betting on Holocene’s Innovate DAC Technology

Holocene’s approach to carbon removal is based on technology developed at the Department of Energy’s Oak Ridge National Laboratory. Unlike many other DAC systems, which rely on energy-intensive processes, Holocene’s solution is designed to be more cost-effective and scalable.

The press release revealed that Holocene uses a combination of liquid and solid-based systems that trap CO2 from the air. This is achieved by passing air through a waterfall mixed with an amino acid, which binds the CO2 molecules. The CO2 is then combined with guanidine to form a solid crystal, which is lightly heated to release pure CO2 for storage.

The company claims its technology stands out using lower temperatures, enabling it to harness waste heat or carbon-free sources. This further reduces energy costs and makes it sustainable.

Most importantly, Google and other tech giants are betting on this kind of DAC technology to slash costs dramatically to meet their carbon reduction goals.

Roadblocks To Commercial Viability

However, this means of cutting emissions still has a long way to go before it becomes commercially viable and scalable. Currently, direct air capture can potentially remove ~ 2,000 tons of CO2 annually and needs to expand massively to create a huge dent in global emissions.

While the deal between Google and Holocene seems promising, the broader carbon removal market remains in its early stages. On the flip side, Google has pointed out certain challenges.

First, the competition for resources such as clean energy is cutthroat to power carbon capture plants and emerging data centers. This clean energy challenge could limit availability and give rise to conflicts. As demand grows, balancing these needs will become critical to ensure both sectors can thrive without straining resources.

A befitting instance of this kind of scenario was when Carbon Capture, the leading DAC developer, was recently forced to relocate its Project Bison facility due to growing competition for clean energy in Wyoming.

The second challenge is that Holocene is still in its early stages and has yet to achieve commercial viability. While it aims to capture 100,000 tons of CO2, this is far less than the billions of tons experts say must be removed annually to avoid severe climate impacts.

Additionally, costs remain high, and the demand for carbon removal services is uncertain. Thus, these costs must drop significantly for DAC projects to gain robust support from businesses and governments.

Image: CO2 capture by DAC, planned projects, and in the Net Zero Emissions by 2050 Scenario, 2020-2030

Source: IEA

Source: IEA

Holocene Confident in Breaking Through the Challenges in Carbon Capture

The DAC startup is confident it can scale its operations, aiming to remove 1 million tons of CO2 annually by 2030. Moreover, being equipped with custom-built systems, it has high hopes to meet its carbon capture goals.

Notably, CEO Anca Timofte, a former Climeworks executive, believes Holocene’s technology will be more cost-effective and easier to deploy on a large scale.

The partnership between Google and Holocene is a major step in tackling climate change. By providing funding and committing to buy carbon credits, Google is helping scale direct air capture. If successful, this collaboration could make carbon removal more affordable which is crucial for meeting global climate targets.

However, while the auto industry association

However, while the auto industry association

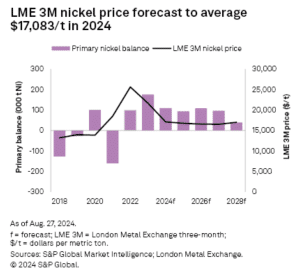

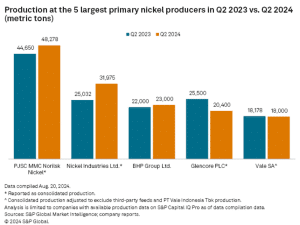

source: S&P Global

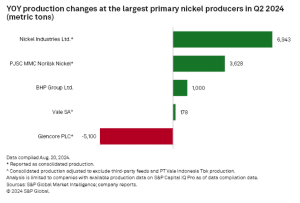

source: S&P Global