Aviation is one of the most carbon-intensive sectors and is tough to decarbonize. It contributes approximately 2-3% of global CO2 emissions. With the sector projected to grow, addressing its environmental impact is more crucial than ever. Airlines and manufacturers increasingly invest in sustainable aviation fuels, electric and hybrid aircraft technology, and improved operational efficiencies. In this mission, Boeing has immensely supported commercial aviation’s path toward net zero carbon emissions. Notably, initiatives like Boeing’s “Cascade” underscore a collective commitment to a greener, more sustainable future for air travel.

The Latest Advances in Aviation Decarbonization

Global aviation, including passenger and freight flights, emits around 1BT of CO2 annually.

The aviation sector faces significant challenges in reducing emissions due to specific parameters like the weight and size of the aircraft, long innovation cycles, and safety issues. Key technologies like Sustainable Aviation Fuels (SAFs) remain costly and are not yet widely adopted. According to last year’s McKinsey analysis, many stakeholders across the aviation value chain have committed to sustainability goals, including emission reductions, SAF adoption targets, and membership in coalitions. Furthermore, The Science Based Targets initiative (SBTi) has emerged as a leading standard, with 25 airlines and aerospace companies setting science-based targets as of April 2023.

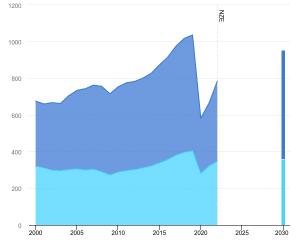

Image: CO2 emissions in aviation in the Net Zero Scenario, 2000-2030

source: IEA

source: IEA

Boeing Takes on Climate Change Challenges

Last year Boeing disclosed its Scope 3 emissions, which arise when customers use their products. This move is in response to investor and climate activist demands for transparency regarding companies’ efforts to minimize their environmental footprint.

Remarkably for the third time in 2022, Boeing achieved net-zero carbon emissions at manufacturing sites and in business travel. David L. Calhoun, CEO of Boeing envisions that in the era of more sustainable aerospace, there is anticipation to achieve it together.

The key highlights from the 2023 Sustainability report are: The strategy for Scope 1 and Scope 2 emissions supports a 1.5 degrees Celsius global warming scenario and global climate goals. Subsequently, aligning with the goals of the Paris Agreement.

Detailed Picture of Boeing’s operational target progress:

source: Boeing

source: Boeing

Harnessing Sustainable Aviation Fuel

The International Air Transport Association (IATA) projects that Sustainable Aviation Fuel (SAF) could provide approximately 65% of the emissions reduction necessary for aviation to achieve net zero CO2 emissions by 2050.

What is Sustainable Aviation Fuel?

Sustainable Aviation Fuel (SAF) is a liquid fuel used in commercial aviation that reduces CO2 emissions by up to 80%. It is derived from various sources including waste oil, fats, green and municipal waste, and non-food crops. SAF can also be produced synthetically by capturing carbon directly from the air. It uses feedstocks that do not compete with food crops, or water supplies, or contribute to forest degradation.

Unlike fossil fuels that release previously stored carbon into the atmosphere, SAF recycles CO2 absorbed by biomass during its lifecycle, reducing overall emissions.

Renewable energy, including SAF, green hydrogen, and batteries, plays a crucial role in reducing carbon emissions throughout Boeing’s operations and products. Boeing believes SAF is vital for decarbonizing aviation and advocates for a strategy that integrates multiple renewable energy solutions. This approach includes advancing the viability and safe implementation of various renewable energy carriers on aircraft.

- It is collaborating with suppliers to ensure all commercial airplanes delivered by 2030 are compatible with 100% sustainable aviation fuel (SAF).

- In 2022, the airliner purchased 5.6 million gallons (21.2 million liters) of blended SAF to support commercial operations.

Strategic Partnerships

Boeing and NASA continued their partnership to test SAF emissions, conducting tests on the 2022 Boeing ecoDemonstrator, which included a 777-200ER with Rolls-Royce Trent 800 engines and a 787-10 with GEnx-1B engines.

It launched the Cascade Climate Impact Model (Cascade) two years back. This web application utilizes global digital technical data to illustrate the environmental impact of different sustainable aviation options. It also offers stakeholders a data-driven tool to navigate decisions towards achieving the industry’s net-zero 2050 goal.

Ted Colbert, president and CEO of Boeing Defense, Space & Security

“We believe that operational effectiveness and sustainability are two sides of the same coin. A more sustainable, lower-cost, energy-efficient defense enterprise is more operationally effective. That’s why we have a history of partnering with our customers to pioneer the use of sustainable aviation fuels and are leveraging digital design and production to reduce our carbon footprint throughout the life cycle of our products.”

The air company aims to achieve 100% renewable energy in operations by 2030, reaching 35% renewable electricity in 2022 through increased usage and the purchase of renewable energy credits.

Is Boeing Facing the Turbulence Right Now?

However, lately, the top-notch airliner has been making news for the infamous, Boeing Scandal. The families of victims in two Boeing 737 Max crashes accused the company of the “deadliest corporate crime in US history”. They have urged the Justice Department to impose the maximum $24 billion fine in a potential criminal trial. As per the latest reports, Prosecutors have not yet finalized the proceedings. The Justice Department may require the aircraft maker to install an independent federal monitor for safety and quality oversight.

- FURTHER READING: Google Signs Up Shell’s SAF Program to Cut Business Travel Emissions

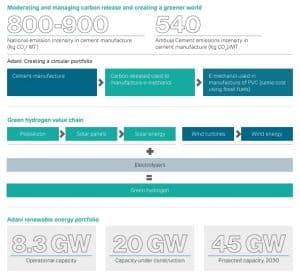

source: Adani

source: Adani source: Adani ESG report

source: Adani ESG report source: Adani

source: Adani

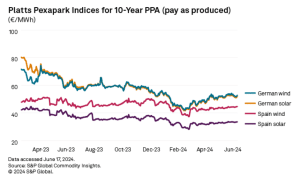

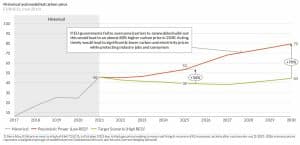

sources: Aurora Energy Research, EIKON, S&P

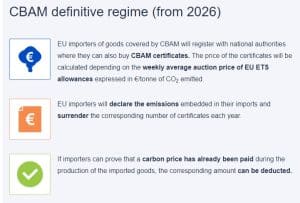

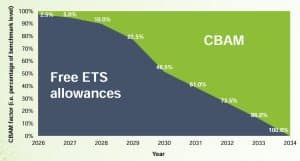

sources: Aurora Energy Research, EIKON, S&P source: EU-CBAM

source: EU-CBAM