On June 4 Occidental Petroleum and BHE Renewables announced their joint venture to extract high-purity lithium from Berkshire’s geothermal facility in California. Together, they plan to revolutionize commercial lithium production by installing TerraLithium’s Direct Lithium Extraction (DLE) technology. This partnership marks a significant step in the advancement of sustainable energy solutions.

We shall deep dive into the JV details and explore the technology in the next paragraphs:

Oxy-BHE Synergy Leading the Future of Sustainable Lithium Extraction

The collaboration aims to leverage the strengths of both companies. Occidental will bring its expertise in chemical engineering and large-scale operations while BHE Renewables will contribute its knowledge of renewable energy and environmental sustainability.

Alicia Knapp, President and CEO of BHE Renewables has further assured that,

“This joint venture with TerraLithium represents a significant advancement in BHE Renewables’ commitment to pursuing commercial lithium production that is environmentally safe, commercially viable, and leads to good outcomes for the Imperial Valley community.”

She further envisions making Imperial Valley a global leader in lithium production.

After successfully demonstrating the technology, BHE Renewables will construct, own, and operate commercial lithium production facilities in California’s Imperial Valley. The joint venture also plans to license the technology and set up commercial lithium production facilities outside the Imperial Valley.

Oxy’s TerraLithium Acquisition Sparks Lithium Revolution

The demand for EVs and consumer electronics propels the lithium market. It is projected to soar from $22.2 billion to $89.9 billion by 2030. Conventional lithium production methods, like evaporation ponds, pose significant environmental concerns. Moreover, production facilities are heavily concentrated in Australia, Chile, and China.

- From the company’s climate report, we discovered that Oxy’s acquisition of TerraLithium in 2022, now a wholly owned subsidiary, is a game-changer.

formed through a partnership with All-American Lithium in 2019, TerraLithium boasts patented technologies capable of cost-effectively extracting trace lithium from waste brines, ensuring ultra-high-purity lithium while minimizing environmental impacts. By acquiring the remaining interests, Oxy harnesses its expertise in chemical plant operations and brine management, promoting sustainable lithium production and securing strategic domestic lithium sources. TerraLithium’s demonstration plant in Brawley, California, near the Salton Sea, is slated to commence operations in 2024.

Jeff Alvarez, President and General Manager of TerraLithium being extremely optimistic about the merger, commented,

“Creating a secure, reliable, and domestic supply of high-purity lithium products to help meet growing global lithium demand is essential for the energy transition. The partnership with BHE Renewables will enable the joint venture to accelerate the development of our Direct Lithium Extraction and associated technologies and advance them toward commercial lithium production.”

TheTerraLithium Technology Advantage

TerraLithium owns patented Direct Lithium Extraction (DLE) technologies that transform any lithium-containing brine into a superior and responsibly sourced lithium supply. It leverages Oxy’s expertise in subsurface and chemical engineering, coupled with a track record in technology scale-up, pilot project development, and global commercialization.

This lithium extraction process promises higher efficiency and lower environmental impact than traditional methods. It minimizes water usage and reduces carbon emissions.

Notably, BHE operates 10 geothermal power plants in California, processing 50,000 gallons of lithium-rich brine every minute and generating 345 MW of clean energy.

This sustainable technology is set to meet the growing demand for lithium, crucial for EV batteries and renewable energy storage. Thus, aligning with both companies’ commitments to environmental stewardship to a low-carbon future.

Oxy’s Commitment to Net Zero goals

Oxy is committed to being part of the climate change solutions and developed the Net-Zero Strategy in alignment with the Paris Agreement. Being the largest oil and gas producers in the U.S., they have established key operations in the Permian and DJ basins and offshore in the Gulf of Mexico.

Furthermore, their subsidiary, Oxy Low Carbon Ventures, spearheads innovative technologies and business strategies that drive economic growth while curbing emissions. They are committed to global carbon management to propel a transition towards a lower-carbon future.

Additionally, it attracted significant new investments into low-carbon projects like DAC, carbon sequestration hubs, hydrogen, and notably, lithium.

source: Occidental

source: Occidental

Warren Buffet’s Bold Lithium Bet

In 2021, Warren Buffett’s Berkshire Hathaway Inc. launched a groundbreaking plan to extract lithium from the superhot geothermal brines beneath California’s Salton Sea. It was believed to be a process that had never been explored before.

Here’s the image of it:

source: BHE

source: BHE

In 2022, they launched a demonstration project with this innovative technology. The strategic JV with Occidental is an extension of this plan. BHE Petroleum notes that if these demo projects succeed then construction of the first commercial plant could start as early as 2024. As already explained before it would essentially provide an environmentally responsible domestic source of lithium. Most significantly, all energy used in this lithium production process would be 100% renewable.

BHE Renewables is making strides in lithium production research in California’s Imperial Valley. Lithium, a crucial mineral for lithium-ion batteries used in cellphones, laptops, and EVs, dominates the brine processed at BHE Renewables’ geothermal facilities.

Will this JV Spark a Lithium Boom in the Future?

The demand for lithium is surging with the rise of EVs and renewable energy storage solutions. Technically the joint venture aims to capture a significant share of this expanding market. Furthermore, TerraLithium’s efficient and eco-friendly extraction process positions it as a competitive player in the industry.

Looking ahead, Occidental and BHE Renewables plan to scale up TerraLithium’s deployment. They are exploring opportunities to implement this technology at various sites. The goal is to enhance the supply chain for lithium, ensuring a stable and sustainable source for future energy needs.

Global oil giants are entering the electrification sector as the US and EU promote higher EV adoption and reduced fossil fuel dependency. Subsequently, Exxon Mobil aims to commence lithium production from sub-surface wells by 2027. Meanwhile, European oil leaders BP and Shell have directed investments toward EV charging stations as integral components of their energy transition strategies.

Last but not least, Richard Jackson, President, of US Onshore Resources and Carbon Management, Operations at Occidental has expressed himself that:

“By leveraging Occidental’s expertise in managing and processing brine in our oil and gas and chemicals businesses, combined with BHE Renewables’ deep knowledge in geothermal operations, we are uniquely positioned to advance a more sustainable form of lithium production. We look forward to working with BHE Renewables to demonstrate how DLE technology can produce a critical mineral that society needs to further net zero goals.”

All said and done, the partnership between Occidental and BHE Renewables signifies a major leap forward in lithium extraction technology and a transition to a greener future.

source: EKI

source: EKI

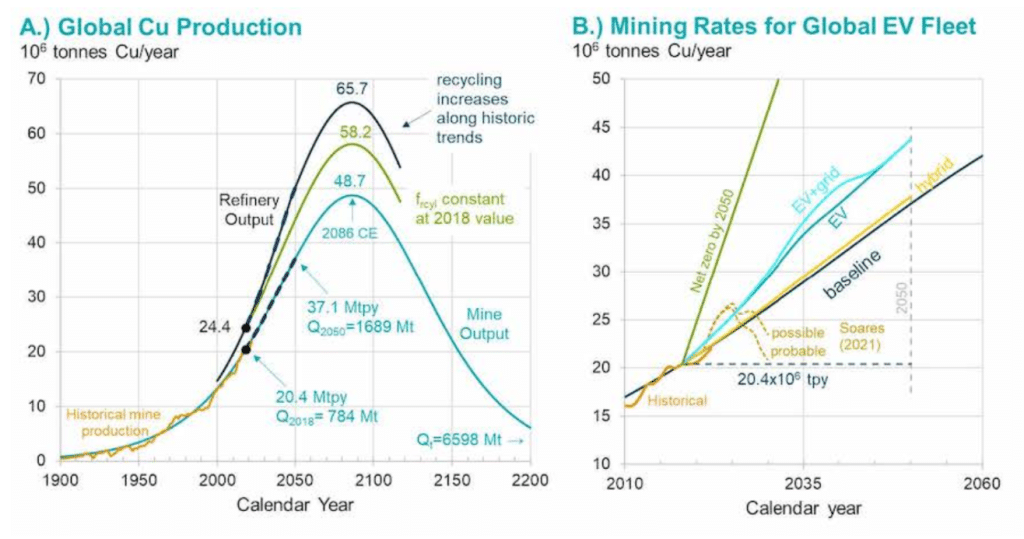

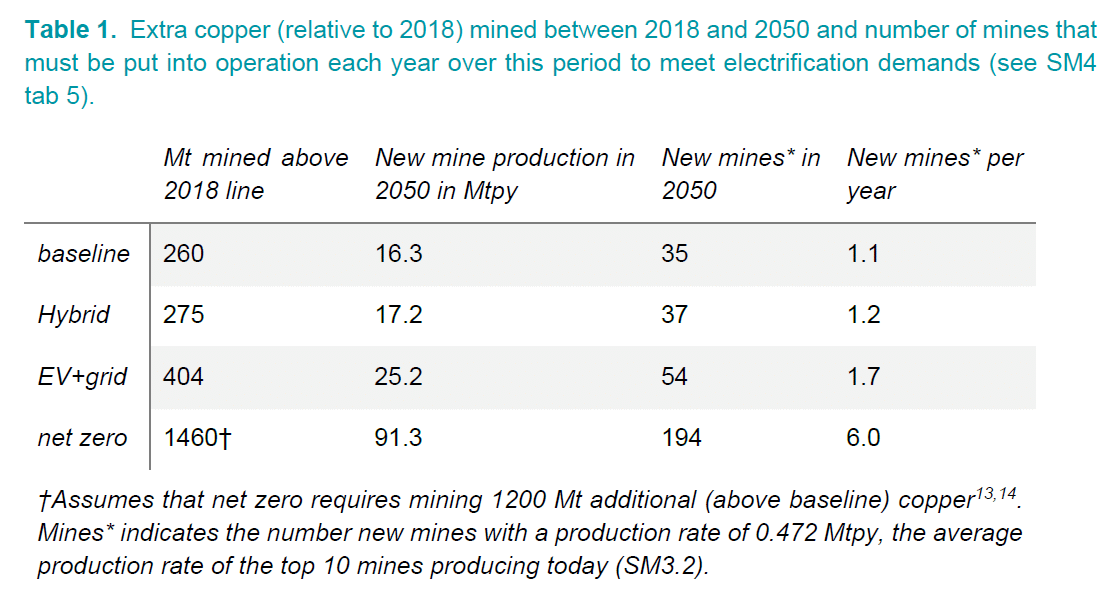

Adam Simon emphasizes the importance of adopting pragmatic approaches to the

Adam Simon emphasizes the importance of adopting pragmatic approaches to the