Fondaction Asset Management (FAM), Priori-T Capital and partners launch one of the largest carbon funds with CAD$115 million to finance emissions reduction projects in North America – the Inlandsis II Fund.

The Fund will be managed by Fondaction’s new fund management platform, FAM, and its partners. The raised capital will be for projects that generate carbon credits both from compliance and voluntary carbon markets in North America.

Fondaction is the investment fund for those mobilizing capital for positive economic, social, and environmental outcomes. It manages net assets of over 3.11 billion dollars invested in the financial markets.

The COP15 is underway in Montréal as the launching happens. It’s another initiative in the financing sector that highlights the importance of pumping capital into climate change, biodiversity and nature conservation.

The Inlandsis II Fund’s $115 million capital is from 30+ investors, led by Fondaction, and includes these major ones:

Chairman of FAM and VP of Fondaction, Stéphan Morency said:

“In addition to financing corrective measures throughout industry to reduce GHG emissions, the Inlandsis II Fund will also deploy its capital on voluntary markets to ensure that efforts toward biodiversity and natural capital protection are more sustained as compared to its predecessor.”

Fighting climate change and protecting nature are closely related. That’s because nature gives us the solutions to lower our GHG emissions by sequestering carbon.

Forests are great carbon sinks, and if the trees are cut down, the capacity to store carbon is also lost. That doesn’t only impact climate change but also the local biodiversity. Thus, similar investments were meant to protect nature and tackle climate change.

According to Fondaction’s Deputy Chief Investment Officer “fighting climate change through forest preservation creates greater biodiversity, as forests often provide refuge to threatened species, but also more economic value for the forests and the communities that rely on them”.

Increasing Inlandsis II Fund’s Capitalization

Actions needed to reach the world’s 2050 net zero goals will require a huge amount of money. And so FAM and its partners expect another funding in the coming months. They anticipate that the Inlandsis II Fund’s capital will go up to $160 million.

Fondaction itself has invested a total of $54 million into the Fund, $24 million in Inlandsis I and $30 million in Inlandsis II. Commenting on the launch, CEO and co-founder of Priori-T Capital Jean-François Babin said:

“Inlandsis is one of the first investment funds worldwide to generate revenue with the carbon credits it makes available through the projects it supports. In addition to generating competitive returns for its investors, the Inlandsis Fund innovates by investing in several types of GHG reduction projects, including the reduction of methane emissions in agriculture and in abandoned coal mines.”

Priori-T Capital develops alternative investment solutions to fight climate change such as the Inlandsis Fund. It seeks to provide investors with opportunities that are carbon market-driven and open access to capital for a greener economy.

For the firm’s Chairman of the Board, launching Inlandsis II Fund gives them leverage in the impact financing ecosystem.

The Inlandsis Fund was established by Fondaction and Coop Carbone in 2017 and committed to harnessing markets to address climate change. It is the only Canadian fund, and one of the few worldwide, to exclusively finance carbon emission reductions.

The Fund provides a unique project financing solution that supplies initial capital in exchange for carbon credits — an innovation that’s vital to bringing carbon emission reduction projects to fruition. Here is Inlandsis Fund’s project map.

From Quebec to the Whole of North America

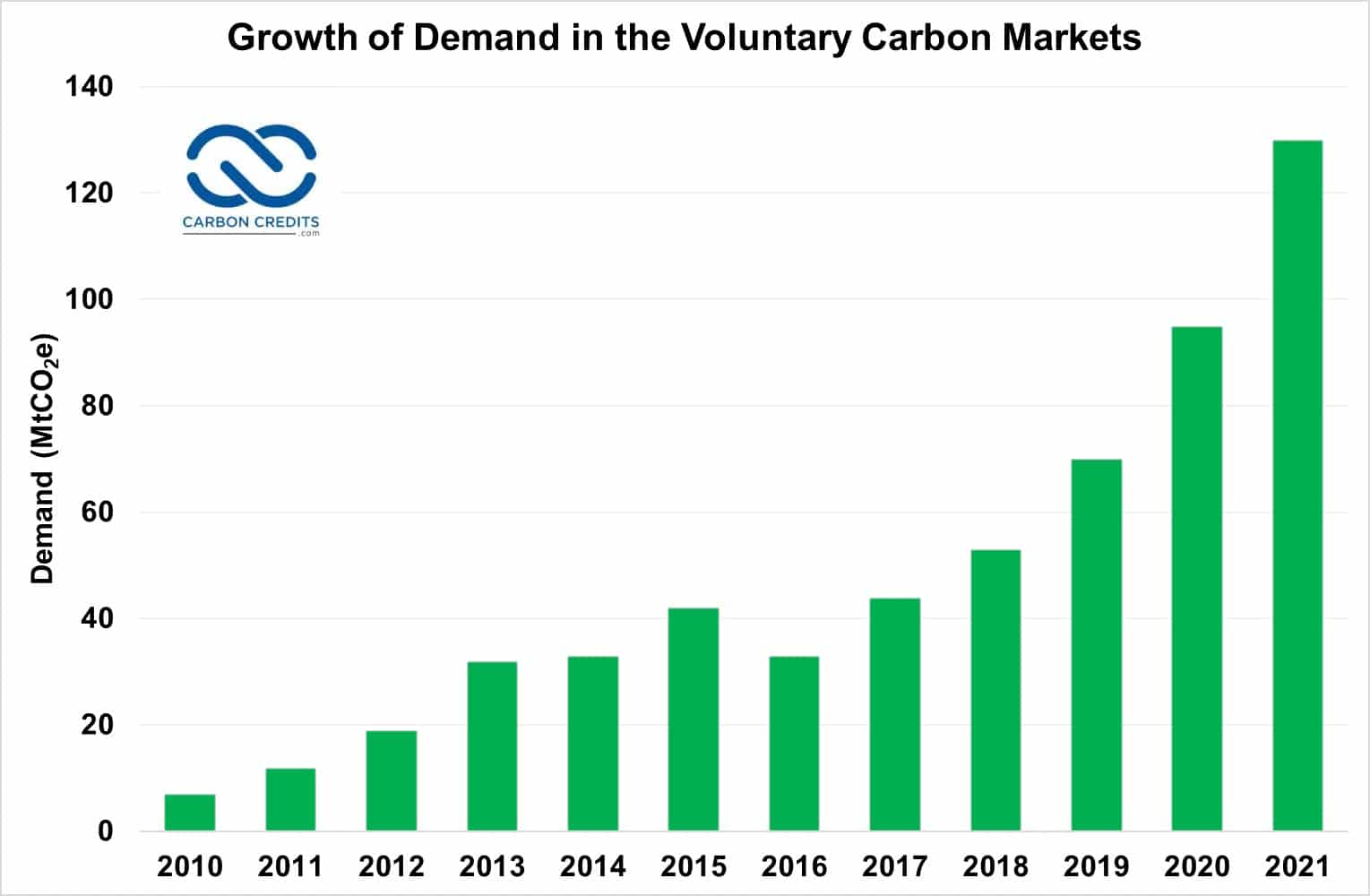

Carbon markets have grown a lot over the last 2 years as shown below. Thanks to the rising net zero pledges from large global companies. Most of these commitments include offsetting emissions by buying carbon credits.

The reason behind the carbon market growth is what inspires the creation of Inlandsis II Fund. The managing director of the Fund, David Moffat, said that the Inlandsis I Fund formed a pioneering center of climate finance expertise in Quebec.

Inlandsis I supports the following projects and initiatives:

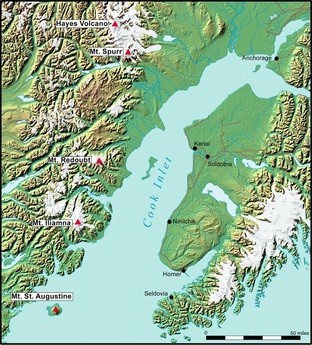

Alaska is earning hundreds of millions of dollars every year through the sales of fossil fuels that contribute a lot to climate change, but it’s now looking to earn money by selling carbon credits.

Alaska only earned a few tens of millions of dollars in all the decades it has been selling timber. And the federal government has locked up the Tongass National Forest, drying up the timber industry in the state.

So, simply put, there were not enough forests to be commercially viable anymore.

Gov. Mike Dunleavy plans to raise money from a new source – carbon credits. For at least some of Alaska’s forested land that’s not harvestable. He said it will bring in hundreds of millions to a billion dollars of income each year.

A Bill on Carbon Sequestration

Carbon sequestration means capturing and storing carbon dioxide, preventing it from entering the atmosphere. It’s one of the commonly used methods in cutting down carbon emissions. It can be done using modern technologies or natural processes.

Gov. Dunleavy aims to introduce a bill to turn Alaska’s capacity to sequester carbon into a revenue stream. He said during a press briefing that:

“Alaska has a real opportunity to sequester carbon in many different ways in the state – through our forests, through our depleted oil and gas basins, as well as the potential for seaweed sequestration off our coasts.”

The governor also said that the state’s depleted basins are excellent carbon sinks. Cook Inlet, for instance, can store as much as 50 gigatons of carbon.

Can Alaska profit from this new business of carbon sequestration with carbon credits? The governor aims to know and he needs to pass a bill that will allow him to develop contracts.

He will propose to the Legislature a carbon credit program for forest lands, depleted oil basins, and even seaweed forests off of the Alaska coast.

The governor said this bill will be a starting point for how carbon sequestration would look in the state. It will also explore how the state can contract with potential credit buyers and what carbon sinks will be involved.

Alaska Forest and Blue Carbon Credits

Trees in forests sequester carbon from the air. This sequestration can generate income through carbon credits sold to entities wanting to offset their emissions.

Gov. Dunleavy disclosed that a firm has approached Alaska, saying that a carbon credit program can generate $30+ billion over 20 years. That’s if Alaska will leave some forests intact. It won’t prohibit other uses of the land like recreation, but the trees should not be cut in exchange for the billions.

“From our perspective at SEACC, the easiest way to increase carbon sequestration in Alaska is to protect the Tongass National Forest. That’s not necessarily up to Gov. Dunleavy, but seeing the governor think more broadly about ways to protect forested areas over which the state does have influence would be critical...”

Some existing forest carbon projects were developed in the state several years ago. Developers such as Sealaska and Ahtna are a few of the Alaska Native organizations doing it.

Fast-growing seaweed like sargassum is an efficient carbon soaker, sequestering up to 20x more CO2 than a tree of the same volume.

Both of these carbon credits, from forests and seaweeds, will not “gore any ox”, according to Gov. Dunleavy. He said that Alaska now has a real possibility of earning revenue with carbon credits. With this, they don’t have to gore any ox (e.g., do an income or corporate taxes on the people).

Potential Carbon Credit Revenues

There was no revenue from carbon sequestration specified in the state’s proposed budget for 2023. But Dunleavy’s 10-year plan includes a target for potential revenue from carbon credits.

His plan projects the following carbon credit revenue generation:

$300 million in 2024

$500 million in 2025

$750 million in 2026

$900 million in subsequent years

Those figures, if they become a reality, will help balance out the finances the state needs to function. But some senators believe that such revenue will not come in that fast.

The bill will take careful analysis and discussion to become law. After all, if it turns into legislation, it can create an opportunity for ‘multigenerational contracts’ between the state of Alaska and the investors, as Senator Stedman said.

Biodiversity credits are the latest tool in the climate action arsenal and the United Nation says that these credits can succeed where carbon offsets fail or don’t apply. So, the organization is backing them up.

But as it’s quite a new concept within the mitigation hierarchy, many people are asking what is a biodiversity credit, why does it matter, and how to earn it.

Meanwhile, others are also wondering how biodiversity offsets work and how they differ from biodiversity credits. If you also have the same queries in mind, this guide will give you the answers and more.

What is a Biodiversity Credit?

First things first – let’s talk about what a biodiversity credit is.

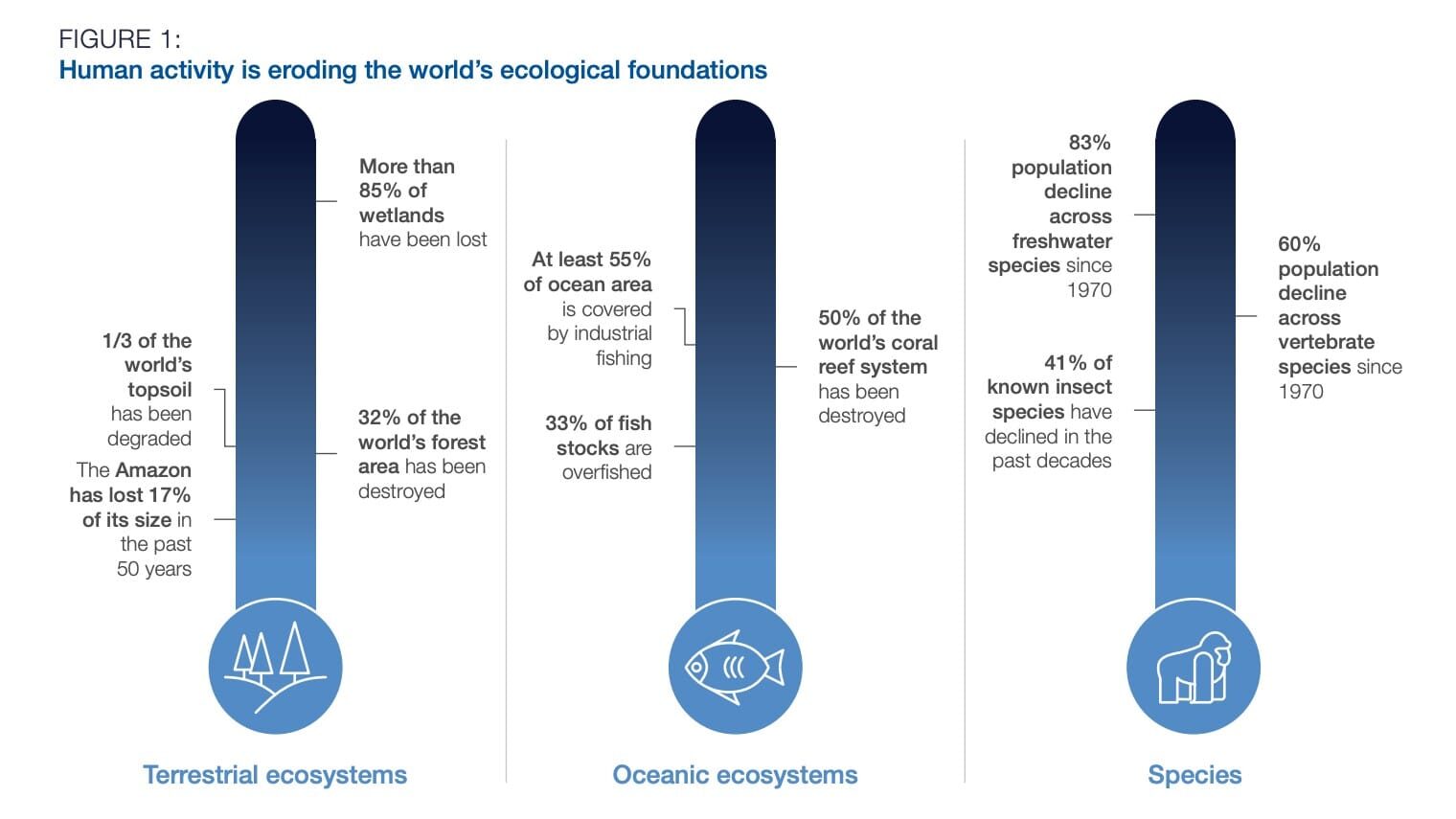

From polar bears to plankton, the breadth and variety of life and ecosystems on earth, or what we call biodiversity, is declining faster than at any other time in human history. This poses a threat not only to the planet but also to humans, the financial systems, while hastening the pace of global warming.

The World Economic Forum estimates that about half of global GDP, or around $44 trillion in figures, depends on the natural world in major ways. That means its degradation also carries a great toll on the global economies.

The world’s 7.6 billion people represent only 0.01% of all living things by weight, but humans have caused the loss of 83% of all wild mammals and half of all plants.

What causes this huge loss?

Same with climate change, human activities are eroding biodiversity and here’s how bad it looks.

Source: IPBES, “Global Assessment Report on Biodiversity and Ecosystem Services”, 2020

So protecting biodiversity is not only good for natural ecosystems, but also for the people that inhabit them. But there’s a huge financing gap to preserve and protect nature – that’s worth $700 billion annually.

And one mechanism that individuals and firms created to plug in the gap and reverse the loss is the biodiversity credits. Through these credits, entities can invest in environmental projects that contribute to a richer biodiversity.

Concept defined: A biodiversity credit is a legal document that represents the environmental action made, where it took place, who developed it, under what methodologies, and that has been certified following a specific system.

Biodiversity credits, or the so-called biocredits, are measurable, traceable, and tradeable units of biodiversity. They are instruments that offer a solution to financing conservation and restoration of nature.

Interest in biodiversity credits is “at a high level” and asset managers have also shown high regard to them. There are good reasons why investors are willing to pour billions of dollars into biocredits.

Biodiversity brings great benefits.

What Benefits Does Biodiversity Offer?

Biodiversity is crucial for health and food security

Biodiversity underpins global nutrition and food security as millions of species work together to provide humans with various fruits, vegetables, and animal products. All these are essential to a healthy and balanced diet but are now under threat.

As a result, ⅓ of the world suffers from micronutrient deficiencies.

Plus, there has been reduced resiliency in supply chains and what we put on our plates. For instance, the number of rice varieties cultivated in Asia has fallen from tens of thousands to only a few dozen. Likewise, in Thailand, 50% of land used for cultivating rice only produces two varieties.

Obviously, conservation of diverse species is critical for our health as well as feeding humanity.

Biodiversity helps combat disease

As humans encroach upon the natural ecosystems, we also reduce the size and number of species living in them. As such, animals live in close quarters with humans which create ideal conditions for the spread of diseases.

About 60% of infectious diseases are from animals. In other words, higher biodiversity rates are associated with better human health.

One obvious reason is that plants are essential ingredients for medicines; 75% of cancer drugs are natural or inspired by nature. So each time a species goes extinct, we’re also missing out on a chance for making new medicines.

Biodiversity benefits businesses

According to the WEF’s report, more than half of the world’s GDP is highly dependent on nature. Take for instance the case of pharmaceuticals – about $75 billion/year of its sales are based on materials of natural origin.

Companies in the food and tourism sectors are also dependent on nature. What this means is that businesses are at risk because of increasing biodiversity loss.

On the contrary, each dollar spent on restoring nature results in about $9 of economic benefits. It also helps avoid trillions of dollars’ cost of social and environmental damages.

Biodiversity brings more livelihoods

Estimates show that around $125 trillion of value comes from natural ecosystems each year. In fact, 3 out of 4 jobs involve water while agriculture employs ~60% of the working poor.

Plus, forests are the main source of livelihood for more than 1 billion people in the Global South.

We must, therefore, protect and restore biodiversity – not only for the good of nature but more so for the people whose livelihoods depend on it.

Why do Biodiversity Credits Matter?

Those four benefits of restoring ecology are good enough reasons to invest in biodiversity. But why do biodiversity credits matter, apart from the strong economic incentives involve?

The key driver behind market driven instruments for biodiversity restoration efforts is that their impacts can be measured and represented in credits. It simply means that they can be integrated into economic decision making.

In a business perspective, the owners can improve their reputation towards customers if they wish to voluntarily support projects that restore or conserve nature.

In the same way, landowners can gain profits from protecting or restoring a habitat. They can also provide more ecological protection than they would have done without the credits as compensation for their efforts.

An executive director’s statement may perhaps sum it all up – the importance of biodiversity credits. He said that “Biocredits offer a tangible solution to the challenge of how to finance the conservation and restoration of nature”.

That’s because the credits can meaningfully channel funds to communities that are the most effective stewards of biodiversity.

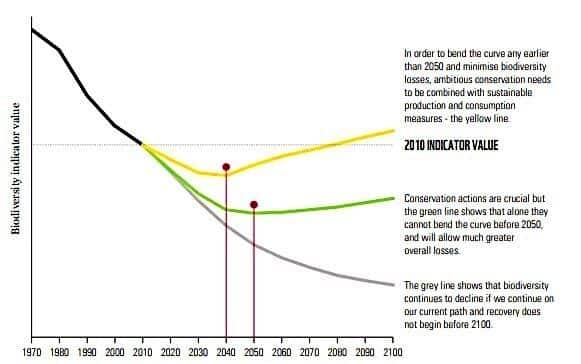

More importantly, biocredits can help bend the biodiversity loss curve as shown in the chart below.

Ambitious conservation efforts – in yellow line – are vital to bend the curve at the critical time requires (before 2050). But conservation actions plus sustainable production and consumption should go together for the world to succeed.

So where does the concept of biodiversity offset blends in? How does it work?

How Does Biodiversity Offset Work?

Biodiversity offsets work somehow similar to carbon offsets. They’re based on a premise that impacts from development can be compensated for if sufficient habitat can be protected, enhanced or established elsewhere. Project development can be in the form of land exploitation for building, mining, or any other activities that have negative impacts on nature.

Biodiversity offsets measurable conservation outcomes designed to compensate for material, residual biodiversity loss after reasonable prevention and mitigation steps have been done. And the need for equivalent ecosystems explains why biodiversity offsets are often entirely local.

The goal of biodiversity offset is to gain ‘no net loss’ of biodiversity.

An offset site is a place where vegetation and species habitat are protected and improved. Protection can be done in various means like fencing, weed and pest control, and planting native species.

The aim of biodiversity offsets is to let development happen in an ecologically sustainable manner, making sure it doesn’t have undesirable effects on ecosystems and species inhabiting them.

Biodiversity offsetting also provides an incentive to protect ecosystems on private land, provides an income for landholders, and achieves biodiversity conservation outcomes into the future.

Biodiversity Offsets vs. Credits

Offsets are economic instruments based on the “polluter pays approach”. They seek to factor in the external costs of biodiversity loss from development projects by quantifying the cost of activities that damage biodiversity.

Biodiversity offsets are often a legal requirement to get, for example, an exploitation permit by a state agency.

Biodiversity credits, on the other hand, are not a legal obligation owed by an entity. They are an instrument used to finance initiatives that result in measurable positive outcomes for biodiversity – be it the species or natural habitats – via the creation and sale of biodiversity units.

Biodiversity offsets and credits may seem to be similar in design. But what makes them different from each other is the intention of the purchase and the claims made around it.

Biodiversity credits are part of a company’s nature-positive journey. In other words, they are an investment in nature’s recovery, not an offset for any damage done.

Biodiversity Credits in Practice

There are some initiatives underway that design biodiversity credits to test the waters for them. New Zealand, Colombia, and Australia are popular examples.

1. New Zealand: “sustainable development units”

In July 2022, New Zealand launched its new biocredits product facilitated by Ekos with funding support from Trust Waikato, the Wel Energy Trust and the D.V. Bryant Trust.

These credits are called “sustainable development units” bought by a supply chain business (Profile Group Limited). They fund the conservation management of 83 hectares at Sanctuary Mountain Maungatautari. The biocredits are not offsets and were issued for short-term biodiversity outcomes.

2. Colombia: “voluntary biodiversity credits”

Colombia introduced its new biodiversity credits last May 2022 created by ClimateTrade and Terrasos. These biocredits are called “voluntary biodiversity credits” (VBCs) first issued by the Bosque de Niebla-El Globo Habitat Bank.

Each VBC, priced at $30, corresponds to 30 years of conservation and/or restoration of 10 square meters of the Bosque de Niebla forest. It’s a cloud forest home to a number of threatened species

3. Australia: “EcoAustralia™ credits”

In 2018, Australia introduced its unique EcoAustralia™ credits by developer South Pole. Unlike other biocredits, each EcoAustralia™ credit is a combination of one “Australian biodiversity unit” (ABU) and one carbon credit (issued by Gold Standard).

Each ABU represents 1.5 square meters of habitat protection.

An example of a project that issues ABUs is the Mount Sandy project. It protects a rare pocket of native vegetation in South Australia’s Coorong region under the care of the Ngarrindjeri people.

Buyers of EcoAustralia™ credits are Porsche Australia, the University of Melbourne, and CareSuper.

These examples show that biodiversity credits are very recent but they’re real. And you can expect that they will be the talk of the town soon just like how carbon credits became the craze.

So, if you’re interested to know how you earn biodiversity credits, let’s move into that.

How Do You Earn Biodiversity Credits?

A key concept you need to grasp if you want to learn how to get biocredits is biodiversity stewardship.

Concept defined:Biodiversity stewardship is an approach to enter into agreements with private and communal landowners to manage and protect land in biodiversity areas.

As a landholder, you must establish a biodiversity stewardship site on your land first then generate the credits to sell to those who need them.

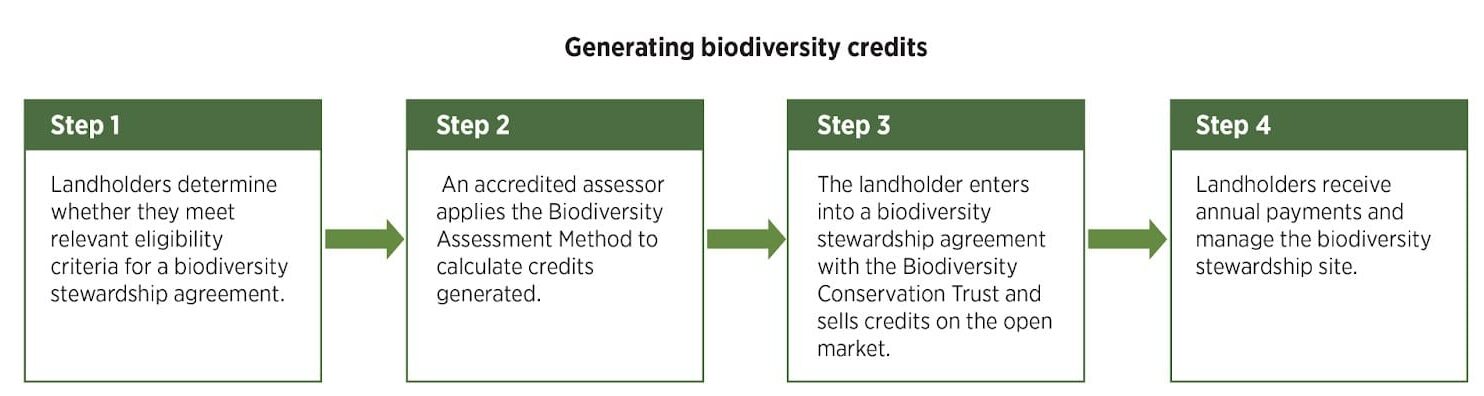

Here are the four major steps to follow to earn and sell biodiversity credits. Australia is, by far, has the most experience in this space, being in the industry for four years now.

Step 1: Determine if you meet the eligibility criteria

The first thing you need is to establish that your land meets the eligibility criteria to be issued with biocredits. At this stage, you can solicit advice from an accredited assessor. They will identify the likely types of credits that will be generated on your site.

Before you formally apply, you may also want to advertise your site on the corresponding register to identify potential buyers of biocredits.

Step 2: An accredited assessor applies the Biodiversity Assessment Method

The accredited assessor will apply the Biodiversity Assessment Method (BAM) to your site and produce a Biodiversity Stewardship Site Assessment Report. It contains the type and number of biodiversity credits generated by having a Biodiversity Stewardship Agreement (BSA) on your site.

The BSA also outlines the proposed management plan for your site. These documents are then submitted to the responsible body.

Step 3: Enter into a Biodiversity Stewardship Agreement to sells the credits

After the relevant body assesses your application against the requirements and agrees on the terms of the BSA, the credits will be registered on the relevant registers, and on the title of your land.

You can then sell the biodiversity credits and the sale will be recorded in the public register of credit transactions.

Step 4: You receive payments and manage your biodiversity stewardship site

Once you receive your first annual management payment, your site turns into an ‘active management’. This means you must start actively managing the site as per the agreed management plan.

After the period of the BSA expires, you can re-apply to renew the active management plan or continue to receive payments to maintain the BSA site.

Biodiversity Credits: Role in Relation to Carbon Markets

Biodiversity protection and restoration is one of the key topics at COP27 in Egypt this year. Apart from the tragedy of flora and fauna species going extinct, this massive loss also hinders efforts to fight climate change.

That’s because natural ecosystems like forests, oceans, and peatlands are great carbon sinks. So losing them means the planet is also losing the chance to stop global warming.

In that sense, biocredits are closely related to carbon credits.

For instance, to make the REDD+ programs work, you need to show an imminent threat for the forest to generate carbon credits. And if no such threat exists, the projects can still offer other benefits to the communities such as livelihoods.

But that may lead to some difficulties in accessing the necessary carbon finance. This is where biodiversity credits come in to rescue and fill the gap. When it comes to where the demand for these credits come from, education and regulation will be the key drivers at this early stage.

But Verra itself has started to develop a framework around biodiversity credits to ensure that they can complement the carbon market.

As to when the biodiversity credits will hit the same maturity of the carbon market right now, others predict it will not be later than four years. Some say it depends. Depends on what?

Education. Regulation. Market dynamics. And having the right metrics and mechanisms that will allow investors to bet their money on protecting nature, with confidence.

The Earthshot Prize awards ceremony for 2022 was recently held in the United States at the MGM Music Hall in Boston, naming five winners.

Each winner was awarded Earthshot prize funding of $1.2 million to develop their environmental solution. The winning participants were from Kenya, India, Oman, the UK, and Australia, with five categories available.

The five Earthshot Prize 2022 winners were selected for five categories, each representing a specific global environmental challenge. The five categories are:

Restoration and Protection of Nature,

Air Cleanliness,

Ocean Revival,

Waste-free Living, and

Climate Action.

These five categories were after the UN’s Sustainable Development Goals.

What is the Earthshot Prize?

The Moonshot challenge launched by President J.F. Kennedy in 1962 inspired the Earthshot Prize. The said challenge set out to reach the monumental goal of landing on the moon within 10 years.

Finding tangible solutions to looming environmental issues that will become critical in the next few years is the main objective of the Earthshot Prize.

Prince William and Sir David Attenborough launched the initiative in 2020 after two years of development, and the prize will run until 2030.

Five annual winners from 15 finalists, will each receive $1.2m in funding. The inaugural Earthshot prize awards ceremony was held in October 2021 at Alexandra Palace in the UK.

The Earthshot Prize Council selected the winners, a thirteen-member council of global ambassadors in various fields of climate action and environmentalism. Some of the council members include Queen Rania of Jordan, Sir David Attenborough, Prince William, and Ngozi Okonjo-Iweala, the current Director-General of the World Trade Organization.

The Earthshot Prize 2022 Winners

The Earthshot prize winner for the ‘Protect and Restore Nature’ category was Kheyti. It’s an Indian startup that developed a ‘greenhouse-in-a-box’ solution to help smallholder farmers increase their yield.

Mukuru Clean Stoves won the Clean Our Air prize award. They’re to develop clean and safe cooking stoves in Africa that do not emit harmful chemicals that cause respiratory issues.

The Revive Our Oceans category winner was the Indigenous Women of the Great Barrier Reef. It is an initiative led by the Indigenous women in Australia to protect critical ecosystems around the world.

The Build a Waste Free World Earthshot Prize winner 2022 was Notpla. The firm is a London-based startup that tackles the plastic waste issue by developing an eco-friendly seaweed-based alternative.

Finally, the Fix Our Climate part of the 2022 Earthshot Prize award went to 44.01, a novel carbon removal solution that permanently stores carbon dioxide by mineralizing it inside rocks. Permanent storage of carbon dioxide has been a critical issue in recent years as part of an effort to drastically reduce carbon dioxide from the atmosphere.

Some of the 2021 Earthshot Prize winners included the Indian-based Takachar, an agricultural waste recycling initiative, and Enapter’s green hydrogen solution, the AEM Electrolyser.

Meanwhile, the Earthshot Prize 2023 nominations are currently open. And the deadline for nominations is on the 31st of January 2023. Submissions can be made via the hundreds of global official nominators for the Earthshot Prize 2023.

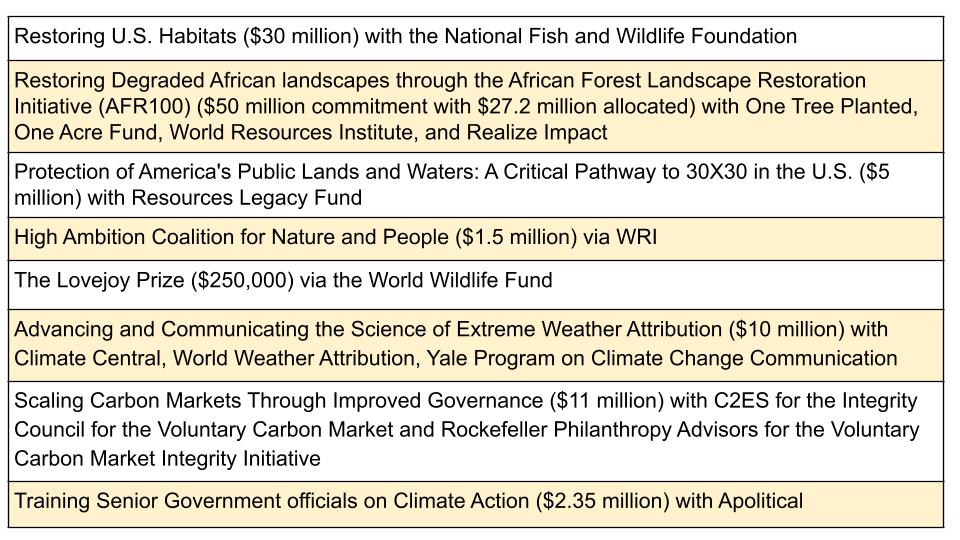

The Bezos Earth Fund announced grants amounting to $110 million as part of its $10 billion commitment to drive climate and nature solutions while advancing environmental justice.

The Bezos Earth Fund, founded in 2020, is Jeff Bezos’ commitment to fund entities and individuals who can deliver solutions to fight climate change and help restore and conserve nature. The $10 billion funds will be zeroed out by 2030, the same deadline for achieving the UN SDGs.

Bezos has been criticized for the amount of carbon that Amazon emits. The retail giant has pumped millions of tons of carbon into the air each year, totaling to over 71 million metric tons as of 2021. Personally, Bezos is trying to reverse that through the Fund.

Last year, Bezos pledged $2 billion towards environmental conservation. The goal is to protect 30% of the Earth’s land and sea by 2030.

Bezos Earth Fund Climate Commitment

The current $110 million funding will be for restoration efforts in Africa and the United States as well as advance climate science, monitoring, and governance in carbon markets.

Recognizing this, Bezos Earth Fund grants the National Fish and Wildlife Foundation with $30 million. The aim is to restore 1.25 million acres of land and forests in the Northern Great Plains and the longleaf pine ecosystem in the American South.

Restoration efforts at this scale can capture carbon and protect biodiversity, particularly in the most significant but damaged ecosystems in the U.S. Community leaders will be the one to design and execute restoration in those areas.

The African Forest Landscape Restoration Initiative

The Fund also awarded another $50 million to AFR100, a local restoration initiative in Africa. It seeks to restore 100 million hectares of deforested and degraded landscapes by 2030. $27.2 million of that funding is given to One Tree Planted, One Acre Fund, World Resources Institute and Realize Impact for restoring the Greater Rusizi Basin and Great Rift Valley.

The Greater Rusizi Basin is known as the ‘lungs of the world’ while the Greater Rift Valley provides habitat for critical forests in Kenya.

Kenya’s Great Rift Valley

The fund from Bezos will serve as grants and loans to projects that restore the land in the region. It will also support initiatives that provide training and monitoring to help scale up those projects. Commenting on this, Vice Chair of the Bezos Earth Fund Lauren Sánchez said:

“Locally-led initiatives can help us fight climate change and protect biodiversity globally, and we are proud to work with partners on the ground to advance these efforts.”

Meanwhile, the Fund’s CEO and President also remarked:

“Local groups are central to achieving global restoration goals. By supporting the African Forest Landscape Restoration Initiative, the Bezos Earth Fund is working to remove three critical barriers to locally led restoration…”

Those barriers include:

Building capacity and drawing on the existing expertise in the region to help restoration projects scale

Ensuring that finance reaches frontline groups

Ensuring that best-in-class monitoring systems are in place to track progress on the ground

With a $10 million commitment, Bezos Earth Fund works with the experts in climate science to give real-time attribution of specific extreme weather events. Examples are fires, droughts, and hurricanes happening in the U.S., the UK, and India.

Carbon markets play a vital role in addressing climate change. They can drive hundreds of millions of dollars to climate solutions. But high standards and strict rules are key to success.

Without them, low-quality carbon credits and unfounded greenwash claims can undermine the market’s potential to deliver billions of tons of emission reductions and removals.

This is where the Fund comes in to help address market governance and credits quality. A $11 million funding goes to initiatives that provide a label for high-quality carbon credits. Example is that of The Integrity Council for the Voluntary Carbon Market that helps buyers find high-quality credits.

And since the public sector also has a big role to take on climate action, the Bezos Earth Fund is also giving a $2.3 million grant to train public officials. The Fund partners with the Government Climate Campus, an initiative looking to close the gap in climate skills and knowledge among key government officials.

Together they will train the first 5,000 officials in the U.S., Brazil, and India across government levels. By 2025, the number will go up to 50,000 public leaders trained to reduce emissions by 50% within the decade.

In summary, here’s the list of the grants awarded by the Bezos Earth Fund:

The U.S. Department of Energy (DOE) announced the launch of four programs funded with $3.7 billion to help build a commercially viable carbon dioxide removal industry in the country.

DOE, the Bipartisan Infrastructure Law, & Carbon Removal

There are efforts currently done to reduce carbon emissions. But they’re not enough to bring the nation to its net zero target by 2050.

Thus, large-scale deployment of carbon removal technologies is crucial to tackle the climate crisis and meet decarbonization goals.

According to Secretary of Energy Jennifer M. Granholm:

“President Biden’s Bipartisan Infrastructure Law provides the transformative investments needed to scale up the commercial use of technologies that can remove or capture CO2… which will bring jobs to our regions across the country and deliver a healthier environment for all Americans.”

Carbon dioxide removal is a critical tool for cleaning up legacy carbon pollution that is already causing significant climate-related damages like intense floods, storms, and wildfires.

In addition, President Biden’s Inflation Reduction Act (IRA) also brings substantial improvements to Section 45Q tax credit for carbon capture and storage.

As per DOE’s estimates, actions both under the IRA and the Bipartisan Infrastructure Law will lead to 40% emissions reduction against 2005 levels across the economy.

The Department’s efforts will bring benefits to communities across the United States. Here are its new carbon removal programs under the Bipartisan Infrastructure Law worth $3.7 billion.

Direct Air Capture (DAC) Commercial and Pre-Commercial Prize

The Office of Fossil Energy and Carbon Management (FECM) is responsible for the $115 millionDirect Air Capture Prize awards to bolster different approaches to DAC.

The DAC Pre-Commercial Prize provides up to $15 million in prizes to boost research and development of breakthrough DAC technologies. While the DAC Commercial Prize provides $100 million in prizes to qualified DAC facilities for capturing CO2 from the air.

Regional DAC Hubs

The Office of Clean Energy Demonstrations (OCED), in tandem with FECM, takes charge of the Regional DAC Hubs program. This is where the biggest investment from DOE goes – $3.5 billion.

The goal is to develop 4 domestic regional direct air capture hubs.

Each of them has to show a DAC technology or suite of technologies at commercial scale with the ability to capture at least 1 million metric tons of CO2 each year from the atmosphere. Then they have to show that they can store that CO2 permanently or convert it into products.

The first funding opportunity announced under this program is worth over $1.2 billion. It will be for conceptualizing, designing, planning, constructing, and operating DAC hubs. More opportunities are expected to follow in the coming years.

Carbon Utilization Procurement Grants

FECM will manage this program, which will provide grants to states, local governments, and public utilities to support the commercialization of technologies that reduce carbon emissions. The same goes for acquiring and using products made from captured carbon.

The first funding issuance will provide grants amounting to $100 million.

Bipartisan Infrastructure Law Technology Commercialization Fund (TCF)

This last program is under DOE’s Office of Technology Transitions (OTT), in tandem with FECM. It will issue a Lab Call to enhance commercialization of carbon dioxide removal technologies such as DAC. The office will do that by advancing measurement, reporting, and verification best practices and capabilities.

OTT will award $15 million to projects led by DOE and supported by industry partners from the emerging carbon dioxide removal sector.

Boosting Innovations in Carbon Removal

DOE launched an initiative called Carbon Negative Shot. The four programs above support the initiative’s goals, looking for innovation in carbon removal pathways that will capture CO2 and store it at gigaton scales for below $100/net metric ton of CO2-equivalent.

They also link with the Carbon Dioxide Removal Launchpad, a coalition of countries committed to leveraging collective resources and best practices to boost innovation and cost reductions across a portfolio of carbon removal technologies.

The coalition members, including the U.S., agree to achieve the following goals:

have at least one 1,000+ ton/year carbon removal project by 2025,

contribute to total investment of $100 million by 2025 to support demonstration projects, and

support efforts to advance robust measurement, reporting, and verification.

Since January this year, DOE has invested ~$250 million in R&D projects and front-end engineering design studies to advance carbon management approaches, including carbon dioxide removal and utilization projects.

The UN Biodiversity Conference (COP15) in Montreal seeks to reverse nature loss and restore biodiversity, but some groups suggested payments for this huge task with “biodiversity credit”.

According to a UN report, the world needs over $384 billion a year by 2025 to protect nature. That goes up to $674 billion by 2050. Biodiversity credits play a critical role to fill that money up.

The Concept of Biodiversity Credit

Biodiversity credits are patterned after the concept of carbon credits. Each carbon credit represents a 1 tonne reduction of carbon emissions.

However, things are more complicated with preserving or restoring biodiversity. There are plenty of metrics involved to track progress. So analysts can’t agree on many things.

For instance, what these credits must look like and how to use them. Some even say that the scheme may go wrong if it allows firms to buy credits as permits for degradation elsewhere.

As the debate continues during the summit, many questions remain on the table.

The hardest one to address is how to value biodiversity uniformly. There are simply millions of diverse species of flora and fauna. Plus, the biodiversity in each area is unique.

So, how should the market price the value of fungi living in a forest? Or the variety of plant species under the ocean?

No Unified Approach to Quantify Biodiversity Gains

Some organizations, including businesses and academics, believe that biodiversity credits can drive financing toward nature conservation. They have some proposals for different methodologies.

With nature’s complexity, various methodologies may exist, according to a founder of a biodiversity credit firm. For example, a well-preserved natural habitat may have to quantify only conservation costs. But an area that needs restoration may have to also measure increases in species richness.

Some don’t even propose to track the flora or fauna. They instead value efforts such as hiring rangers or implementing monitoring systems to avoid deforestation.

But there’s one approach that aims to measure and value biodiversity gains. Wallacea Trust, a UK non-profit, monitors at least 5 animal categories in an area. Each of them is valued based on how rare the species are in the country, and their abundance is estimated.

For every 1% increase in species abundance/richness or prevented loss per hectare, one biodiversity credit is generated.

Implementing Voluntary Market for Biodiversity Credits

The big question remains on why companies should buy biodiversity credits with a lot of queries around them.

In Australia, the government makes it compulsory for companies to buy biodiversity credits to offset damage caused in one area and fund preservation in another. This may be the case with EU firms with new rules forcing them to disclose impacts on nature.

But some industry groups oppose the idea of the credits letting businesses offset destruction elsewhere.

However, negotiators at the COP15 summit focus their talks on the potential voluntary markets in the private sector. They’re not after the compliance markets where biodiversity credits trading is mandatory.

The draft of the COP15 discussion also hinted at the promotion of a related scheme “biodiversity offsets”.

Outside the summit, the World Economic Forum (WEF) and the Biodiversity Credit Alliance are discussing how to set up a voluntary market. They plan to launch it next year with a system that ensures the credits deliver their conservation claims.

Having a high standard in place is critical as a policy officer from a carbon credit platform noted:

“When you can point to many examples in a market of low quality or low standards, it creates distrust and it impacts the integrity of the overall market…”

Other experts caution that biodiversity credits will allow companies to “greenwash,” or make false claims of conserving nature.

But it’s worth emphasizing that biodiversity credits do not replace governments with strict laws prohibiting nature’s degradation. According to Pollination’s CEO, Martijn Wilder, governments must compel companies to invest in biodiversity.

“Paper or plastic?” was the old supermarket question, and it still rolls around every year at Christmas. But when it comes to carbon emissions of a real or fake Christmas tree, the debate can get heated.

Specifically, there’s an intense discussion around the idea of which is better for the environment.

Trees – the real kind – are, after all, carbon sinks. Cutting one down to place it in your living room for a few weeks seems wasteful.

On the other hand, replacing something all-natural and all-organic with yet another non-recyclable, plastic imitation feels as un-green as it can get.

So, when it comes to Christmas tree carbon emissions, which is worse – paper, or plastic?

The Real vs. Fake Debate and CO2 Emissions

The debate about “environmentally friendly” Christmas trees boils down to one important stat: CO2 emissions.

On the surface, the debate seems to favor fake trees. If real trees are carbon sinks, cutting them down provides one less way to lock away atmospheric carbon. And that’s one more way to release that CO2 back into the air.

But as it turns out, things aren’t that simple regarding trees.

Also, there are nearly 350,000 acres in production for growing Christmas Trees in the U.S.; much of these productions preserve green space.

When it comes to growing Christmas trees, the time can range from 5 to 15 years to grow a tree depending on the growth conditions. But on average it takes 7 years to grow a 6-7 ft Christmas tree.

Cutting down trees sounds bad, but making them might be even worse. A closer look at average carbon emissions for both real and artificial Christmas trees paints a clearer picture.

CO2 emissions for a real Christmas tree: Keep the carbon locked away

Time for the headline stat: 0 kg of CO2.

That’s the amount of CO2 your annual Christmas tree releases if you cut it, use it, then chip it up (using renewable power) and spread it on your garden.

Why nothing? Because trees lock away carbon primarily in their trunks.

True, forget to water the tree after you’ve brought it in, and you’ll see needles everywhere. But even when those needles decay, the CO2 they release is negligible. It’s the trunk and branches that matter after all.

And if you grind those up at the end of Christmas, you produce long-lasting bark mulch that releases CO2 very slowly over several years as part of a natural process.

Of course, not everyone has a wood chipper around to dispose of their tree. Toss your old tree in the landfill, and the resulting decomposition (which releases methane, as well as CO2) results in about 16 kg of CO2e per 6.5-foot tree.

It’s actually better to simply burn your old Christmas tree. This is a simple one-for-one exchange, as burning the tree releases all the CO2 it had absorbed over its life – for an average Christmas tree, roughly 4 kg of CO2. Burning does not result in the extra methane emissions, making it a more emissions-friendly option.

By far the best option is to use a potted tree. Bring the same one in, year after year, or plant it and purchase a new one to repeat the process – and kickstart your own personal Christmas tree offset program.

Carbon emissions for a fake Christmas tree: Production footprint

What about fake trees?

On the plus side, there’s no methane from decomposition, and no release of CO2.

But that’s about as good as it gets. Fake trees are generally made from plastic and metal. Both of them traditionally rely on carbon-intensive manufacturing methods and account for roughly 70% of a plastic tree’s carbon footprint.

Moreover, between 80%-90% of the artificial Christmas trees sold each year in the US – somewhere around 10 million trees – are produced in China. To calculate the true carbon footprint of your average artificial tree, you also need to include transportation and production costs.

That’s why the average artificial tree carries a carbon emissions cost of around 40kg, compared to the 3.5-16kg per real tree.

At the end of the day, artificial trees are largely plastic. Oil-based production plus global shipping costs tend to result in high carbon emissions.

Real Christmas Trees: Ongoing Reforestry Offsets

To make the Christmas tree carbon emissions math work, each fake tree would need to be reused between 4-10 times before it resulted in less emissions than a real tree.

And even if that were the case, artificial trees would still take up space in a landfill, without the benefit of being biodegradable.

In contrast, for every Christmas tree cut down, around another three trees are planted each year.

Real trees result in lower shipping costs and reduced emissions from transport in comparison to artificial trees: the average real tree travels a little over 200 miles from source to final destination, while plastic trees can cover over 8000 miles on their trip from manufacturing in Asia to other global markets.

The Christmas tree industry operates as a market-induced carbon offset mechanism. Thousands of Christmas tree farms sequester as much as one tonne of carbon per acre. And trees are generally replanted as fast as or faster than they are cut.

Christmas tree co-benefits:

Supports local farmers and producers

Encourages young-growth forests (trees are typically cut after seven years

Easy to recycle

Filters air and produces oxygen while inside

Can be used in aquatic or riparian environments to encourage diversity

The result is a carbon-neutral industry that removes nearly as much CO2e as it emits. Even The Nature Conservancy acknowledges that the real Christmas tree industry plays a vital role in the push for forest restorations that could account for 30% of the carbon emissions reductions the world desperately needs.

Not to mention that the great Christmas tree industry employs ~100,000 people in 15,000 farms across the U.S.

But in the end, the answer is pretty simple; when it comes to Christmas tree carbon emissions, pine beats plastic every time.

Amazon is testing out its new carbon credit label called ABACUS Verified Carbon Unit (VCU), which goes above and beyond Verra’s methodology and will focus on ensuring additionality, leakage, and durability standards in the market.

Trust has been at the center when dealing with the issues confronting the carbon market. Some buyers of carbon credits are afraid that they will not receive the emissions reduction those credits promise.

Same with other products, there are good and bad carbon credits. The good ones are from projects that result in actual and real removal or avoidance of carbon. The bad ones don’t deliver real and positive impacts.

The challenge for both buyers and sellers is to spot the difference. And this is what the new carbon credit label of Amazon will try to address.

Amazon ABACUS Verified Carbon Unit (VCU)

In partnership with Verra, Amazon unveiled their plan to create a label that they claim to bring a higher standard of producing carbon credits back in July.

The carbon credits the system will generate will satisfy additional standards already required from traditional VCUs. Verra said that ABACUS is the first VCU label that came from a 3rd-party working group.

That group comprises Amazon research scientists and experts at the University of California Berkeley, The Nature Conservancy, and other organizations.

Amazon’s inspiration for creating the ABACUS VCU label is to improve public trust in the environmental integrity of carbon credits. This is critical for the voluntary carbon market to grow.

The architect behind the new carbon credit label, Jamey Mulligan, gave a sneak peek of the Amazon ABACUS VCU. He said:

“It is the first carbon market label that reflects innovations in the carbon accounting itself. [We are] creating an incentive for project developers to road test new project design concepts and carbon quantification methodologies that, at the end of the day, are built to enable confidence that the credits represent what they claim.”

The new carbon credit label will focus on two project types – agroforestry and reforestation. That’s because additionality, leakage, and durability are hard to deal with in those areas. But the projects also have great potential for significant climate, social, and environmental benefits.

Mulligan noted that ABACUS will improve the story for each of those standards. And to qualify for that label, VCUs must come from projects verified by Verra’s afforestation, reforestation, and revegetation (ARR) methodology.

How ABACUS Differs From Traditional Carbon Credits

Additionality:

One way that ABACUS VCUs are different from the existing credits available on the market is how they account for additionality. The label will require project developers to consider additionality at the start of the project.

Rather, they have to track changes in the project’s carbon stock over its lifetime while comparing it continuously to a baseline. This practice uses what they call a dynamic baseline to evaluate additionality.

In Mulligan’s words,

“Essentially, projects have to outcompete matched control plots in the surrounding landscape to maintain additionality. This effectively transfers the risk of future non-additionality, from the atmosphere to where it is today, to project investors, where we think it belongs.”

Leakage:

Another way that Amazon hopes ABACUS VCU will improve the credit standard is on leakage. It happens a lot when agriculture results in indirect land use change and loss of carbon.

ABACUS will prevent that leakage by supporting projects that make the rest of the degraded land or its nearby region equally productive. This will help maintain the agricultural production rate of that location.

The new label believes that carbon removal projects must not come at the expense of food production but must be engines of food security.

Durability:

Lastly, climate solutions through nature have struggled to prove their durability or permanence. This is why buffer pools are created to cover for their potential losses due to wildfire or harvests.

ABACUS crediting will still use the same approach of pooled buffer accounts. But they will be from projects with high quality. And that tree species are better adapted to the project area.

Still on durability, the new scheme will cut down the crediting period from the standard 50 years to only 30.

Ridding of the last 20 years will have little impact on the investors’ financial outlook at the time of investment, said Mulligan. This, in fact, creates unaccredited removals that can compensate for partial losses, acting as another buffer pool.

Testing and Refining ABACUS

Though such changes in carbon crediting scheme sound promising, they need polishing. Amazon and Verra will work together to test and refine the ABACUS VCU label.

Verra completed a pre-consultation last October but ABACUS still needs testing on the ground with real and pilot carbon projects.

Plus, both organizations have to do a lot of work to ensure the success of ABACUS. And the key to that is trust and cultivating it on both sides, according to Mulligan.

A final decision on the proposed label will be due in January 2023.

Carbon offsets are one of the ways to help airlines in their race to net zero emissions. But recently, two major airlines – JetBlue and EasyJet – opted to stop carbon offsetting and focus on other ways to lower their carbon footprint by ramping up their use of sustainable aviation fuel (SAF).

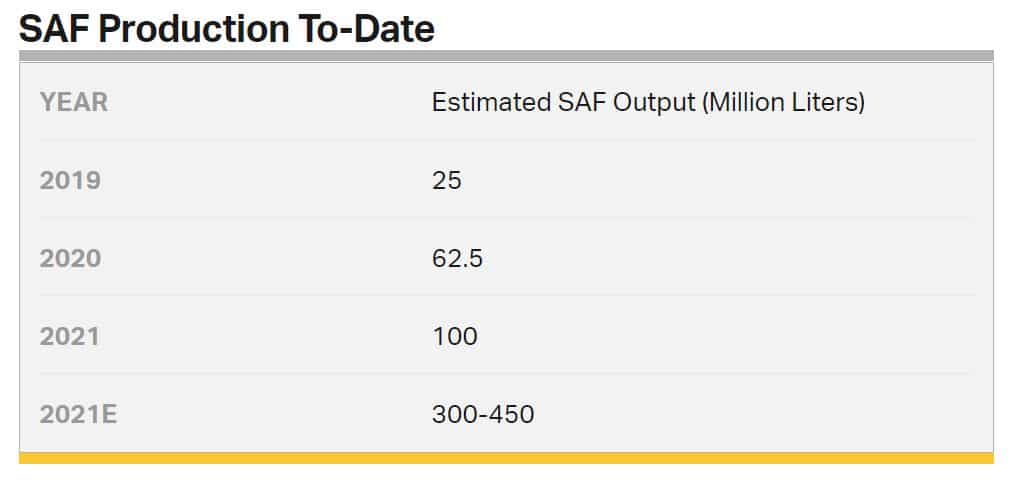

Some airlines now see SAF as a way to ramp up their decarbonization goals. Current estimates by the International Air Transport Association (IATA) show that SAF will account for about 65% of mitigation needed by the aviation sector.

The IATA estimated that total SAF production will reach 450 million liters in 2022. That’s over a 3x increase over the 2021 production of 100 million liters.

Here’s the growth of SAF production to date as per the IATA data.

To date, over 450,000 commercial flights have been operated using SAF. And the growing number of airlines signing agreements with SAF producers sends a clear market signal that this low-carbon fuel is in demand. Two recent examples are JetBlue and EasyJet.

JetBlue Ramps Up SAF Uptake

JetBlue Airways, a major American low-cost airline, pledged to reach net zero by 2040 using six methods including SAF and a massive carbon offsetting program. The airline first used carbon offsets in 2008, using the proceeds to support projects like wind power development, methane gas capture at landfills, and reforestation.

But it recently announced that it will quit buying carbon offsets for its domestic flights in 2023 and decided to focus on using SAF instead.

JetBlue considers carbon offsets as a powerful tool that enables them to tackle emissions immediately when developing a longer-term reduction plan including SAF. The airline’s director of sustainability and ESG Sara Bogdan said in an email that:

“The time is now to maximize investment into the space [green fuel] and accelerate our uptake of SAF…”

The US carrier revealed the shift as part of its wider commitment to cutting GHG emissions from jet fuel by 50% per revenue ton kilometer by 2035 from 2019 levels. This reduction is its most aggressive near-term target, the airline said.

Yet, JetBlue is not giving up on carbon offsets completely. It will continue to buy a small quantity of high-integrity carbon credits for flying from 2024 and to offset emissions from expanding international flights. The airline will work with experts to deal with issues on carbon offsets and assess which bring the biggest benefit.

Bogdan further added that “we do see an opportunity for greater transparency from the carbon credit market.”

The airlines has been using SAF for some flights since 2020 under supply agreements with Neste and World Energy. It has also signed deals with three more SAF producers with the plans to convert 10% of its fuel to SAF by 2030.

The US carrier joins Swiss EasyJet, which in September said will ditch carbon offsetting by the end of this year. It will opt to use SAF, too, as part of its roadmap to net zero emissions by 2050.

EasyJet Shifts to SAF

EasyJet was one of the first major airlines to offset all of its emissions when it introduced the program in 2019. The company said it had offset about 8.7 million tonnes of emissions since then.

But the carrier decided to use its money to invest in new technologies from fuel-efficient aircraft to switching to greener fuels like SAF. This shift will reduce its emissions by 78% by 2050, while the 22% cut by using carbon capture technology.

The Swiss carrier’s CEO Johan Lundgren remarked:

“Our carbon offsetting programme has been the right thing to do . . . [but] you need to deal with your own operations, you cannot rely on out-of-sector initiatives. It makes much more sense to invest into direct initiatives that reduce our own carbon intensity.”

But the airline said it will still allow customers to pay to voluntarily offset their own emissions.

According to the Science Based Targets initiative (SBTi), offsets can only be used to compensate for a small portion of residual emissions that can’t be dealt with in the long term.

EasyJet’s and JetBlue’s shift to SAF contrasts with some airlines.

US carrier Delta Air Lines, for instance, spent $137 million to buy and use 27 million offsets last year. While British Airways claims that all its domestic UK flights are “carbon neutral” by offsets that cover these journeys.

As they race to net zero, airlines are using both carbon credits to offset their emissions and SAF to cut pollution directly at the core.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

.jpg)