If you’re into carbon accounting, you probably have encountered scopes 1, 2, and 3 emissions used to determine a company’s carbon footprint and guide reductions efforts… but have you heard of Scope 4 emissions?

Most likely, not yet. That’s because Scope 4 emissions are an addition to emissions that companies need to keep track of.

While the concept is quite new, understanding it and knowing how to account for it is useful for companies and organizations wanting to curb their emissions and meet their climate goals.

So, we’re going to explain what Scope 4 emissions are, how they differ from the other scopes, why they’re important and beneficial for companies to measure and report, alongside the major challenges in calculating them.

What Are Scope 4 Emissions? How Do They Differ From Other Scopes?

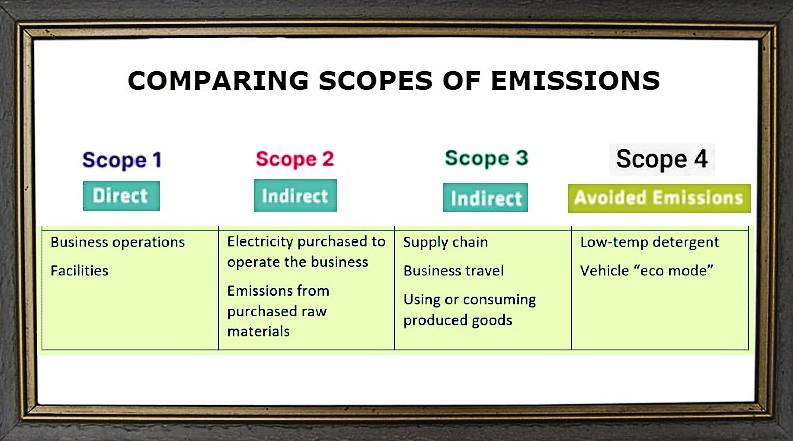

To understand Scope 4 (S4) emissions, we need to differentiate them from its peers. Scope 1, Scope 2, and Scope 3 emissions refer to direct, indirect, and other indirect emissions, respectively.

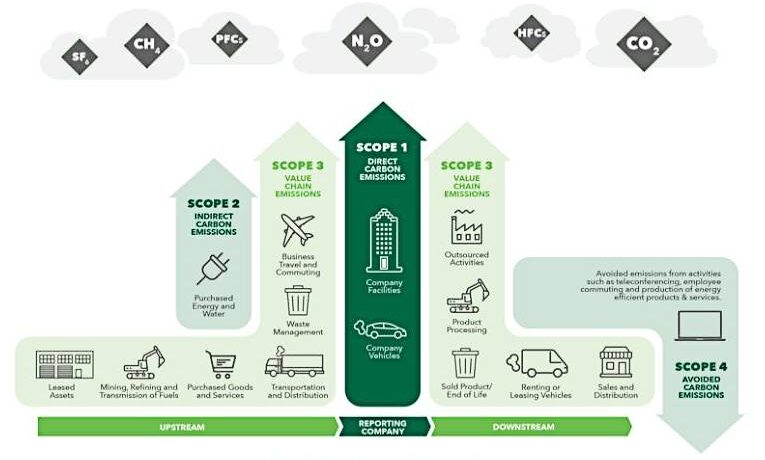

- Scope 1 emissions are from direct sources such as fuels burned to heat products or run a machine.

- Scope 2 emissions are indirect footprint resulting from purchased energy used by the company such as electricity.

- Scope 3 emissions refer to all other indirect emissions, such as embodied carbon of building materials and supply chain.

In other words, they’re what a company emits through their operations and other business activities.

Companies have full control over their Scope 1 and 2 emissions whereas Scope 3 emissions are generated by activities that the company can’t control.

Scope 4 emissions, on the other hand, refers to the AVOIDED emissions or carbon pollution that happen OUTSIDE of a product’s value chain. They’re a result of using that product or the saved emissions due to its performance.

Theoretically, S4 emissions provide companies a way to report on the avoided emissions by opting for more efficient products, either a product or a service.

For instance, telecommuting or carpooling to work saves on the carbon footprint of working. Likewise, decreasing energy consumption by using energy efficient equipment or appliances also cuts down carbon emissions.

At a glance, here’s how these different scope emissions differ from each other:

There are two main types of S4 emissions:

- Product or service that replaces a more carbon-intensive product: e.g. tele-conferencing services that reduces the emissions of traveling to office.

- Product or service that reduces emissions elsewhere: e.g. a low-temperature detergent that uses less energy.

Scope 4 emissions also cover work-from-home scenarios as they avoided using transport fuel and energy use in office work.

S4 emissions can be quite challenging to measure and report, but it’s becoming increasingly important for companies to do so. By fully understanding their Scope 4 emissions, businesses can identify areas where they can reduce their planet-warming emissions and contribute positively to climate change.

Why Should Companies Report Scope 4?

Most companies would like to account and report on their S4 emissions to gauge their efforts in helping their respective industry slash emissions.

In fact, 75% of the surveyed companies by the Carbon Disclosure Project (CDP) are offering products and services that help others reduce emissions. The caveat, however, is that without enough data to back up their claims, they remain unsubstantiated.

In other words, to validate their claim on reductions of a product/service, rigorous testing, predictions, and reporting is key. It also calls for scientific estimations or calculations on how consumers use a company’s product.

In principle, calculating avoided emissions needs extensive research and product development or improvement. In practice, though, it’s so much more difficult to make accurate calculations and substantiate claims.

That’s why accounting for S4 emissions right from the very beginning of making a product/service is crucial. It also sets a baseline from which to measure the avoided emissions.

On the contrary, failing to consider these emissions may result in serious consequences for a company. Apart from a potential fine if a certain regulation is not met, the business may report its total emissions incorrectly.

More remarkably, incorporating avoided emissions the soonest time possible puts a company at an advantage compared to its peers. Currently, it’s not mandated to report on these emissions, but as governments started to become more stringent in regulating climate disclosures, companies who have their feet on this front will find it easier later on.

Existing Guidance or Framework for Reporting S4

Tracking and disclosing emissions under S4 can be tricky and there’s no standards available yet today. But if your company attempts to do it, there are some frameworks that can guide you.

A good starting point is the World Resources Institute’s guideline entitled “Estimating and Reporting the Comparative Emissions Impacts of Products”. It may not be the most comprehensive framework but it helps in learning how to collect credible data for S4. It’s a sector-specific guidance for industry associations.

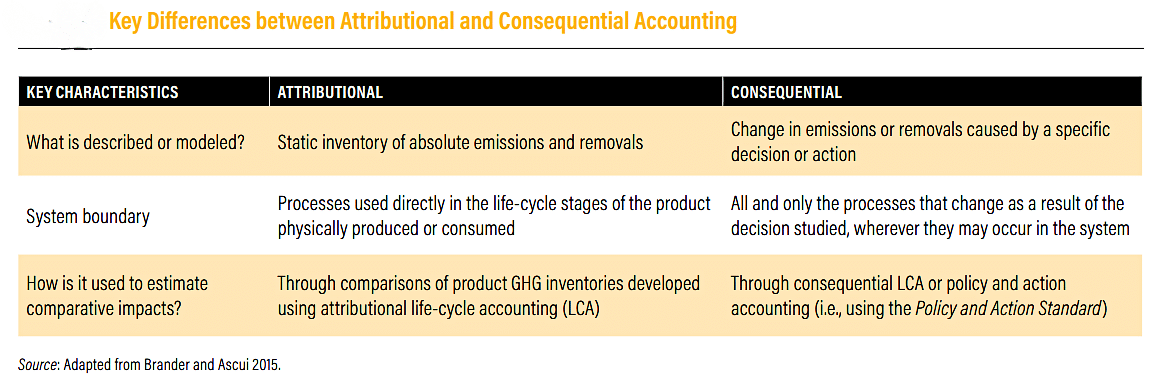

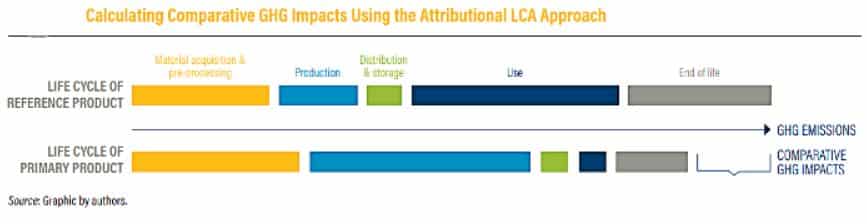

As the paper suggests, it’s a framework for estimating and disclosing the full impact of products. It includes guidance for accounting for a product’s negative and positive impact on emissions. This S4 accounting comes in two different approaches defined and compared in the table:

The framework also offers recommendations on how companies can improve the credibility and consistency of their claims. Companies can consider three common avoided emissions claims that the WRI specified:

The framework also offers recommendations on how companies can improve the credibility and consistency of their claims. Companies can consider three common avoided emissions claims that the WRI specified:

- Claims that compare avoided emissions of a product to its previous version,

- Claims applying the benefits of a product’s S4 emissions to the whole market to measure emissions, and

- Claims resulting from comparing emissions of various products.

One of the recommendations of WRI in using their guidelines is for companies to measure emissions from every stage of the product’s life cycle for correct representation of how it compares to the previous product.

Another supplemental guideline is the GHG Protocol’s Policy and Action Standard. The GHG Protocol is also developed by the WRI. Though the standard seems to be more general, it suggests that reporting companies consider how their products will change emissions.

Another supplemental guideline is the GHG Protocol’s Policy and Action Standard. The GHG Protocol is also developed by the WRI. Though the standard seems to be more general, it suggests that reporting companies consider how their products will change emissions.

By using these frameworks and approaches, you can more effectively measure and reduce your company’s Scope 4 emissions.

However, given that S4 emissions are outside of your company’s value chain, capturing it comes with some hurdles.

Key Challenges and Limitations in Disclosing Scope 4

Reporting on S4 emissions entails overthrowing some roadblocks along the way. Let’s enumerate and explain the main challenges you may encounter along the way.

-

Difficulties in Measuring S4

To measure scope 4 emissions accurately, companies must validate that their offerings really do avoid emissions. This entails a lot of resources from start to end of the validation process. The most difficult part is estimating on how customers use and dispose of the product.

Not to mention that it may involve complicated assumptions and calculations, calling for extra market research.

For instance, the company has to know how many consumers were using the older product and whether they’ll replace it with the new version. Incorrect data collected would be very bad if used as a basis for decision making related to the product.

-

Quantifying Avoidance is Complicated

Measurement is one thing and quantifying avoidance is another thing. But they’re both hard to come by accurately. Take for example the case of selling second hand items like bags or shoes. The seller can assume that their second hand products can avoid buying new items.

But what this assumption may use to consider is that consumers may buy more than one of their items. That’s simply because they’re cheaper to buy, so they can buy more. The seller has to factor all these things when quantifying for the product’s avoided emissions.

-

Quantifying Avoidance is Complicated

As mentioned earlier, researching, developing and testing new products needs plenty of resources. In other words, companies may have to invest big for the upfront costs. But this should not discourage them to make new and innovative products that can actually reduce emissions.

-

No Widely Accepted Standard

While there are some guidelines available relating to Scope 4 or avoided emissions, there’s still no widely accepted standard. This lack of standardization further makes it more challenging what to follow when measuring and reporting S4. But the WRI framework would be a good way to start on this climate disclosure quest.

-

Accusation for False Claims

All the previous hurdles above boil down to one thing that companies all fear to face – greenwashing. Inaccurate data or overestimations of avoided emissions will likely put the company in the spotlight for scrutiny.

Climate activists are even more vigilant today as planet-warming emissions continue to cause disasters and damages worldwide. Being subject to greenwashing accusations would damage the stakeholder’s trust, including customers and investors.

Now, we’ve come to the last question you may have – how to calculate and report S4? That depends on the specific industry you’re in. Let’s take a look at some examples.

How Can Industries Calculate and Report S4?

Companies operating in the real estate industry can measure their S4 by measuring tenant commuting footprint. They can do that either by sourcing data from transportation apps or directly asking or surveying their tenants. They may also factor in waste diversion rates to account for avoided emissions.

If you’re into a retail business, you can calculate the environmental footprint of your products using life cycle assessments. This approach takes into account avoided emissions in the supply chain.

It’s different if you have a manufacturing company. You can measure Scope 4 emissions through energy efficiency initiatives and process improvements.

Specifically, if a company is manufacturing capital goods, they can follow the example of French multinational company Schneider Electric. Schneider specializes in digital automation and energy management, making it easier for them to provide examples of calculation of avoided emissions via their variable speed drives, which generate savings on energy consumed by using their VSD.

For instance, in one of Schneider’s reports, it showed that its EcoStruxure Industrial Internet of Things platform enabled customers to save a whopping 134 million metric tonnes of CO2 since 2018. That avoided emissions equal to the footprint of over 28 million gas-powered passenger cars driven for a year.

If you’re running a business in the hospitality industry, you can consider transportation emissions, such as shuttle services. You can also convince guests to reduce their own footprint while using your facilities and amenities.

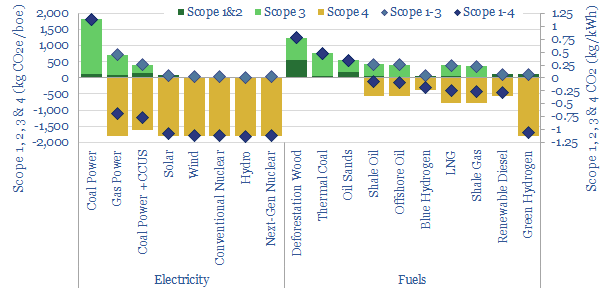

Here’s a sample calculation of various emissions, including scope 4 by the Thunder Said Energy.

After getting all the Scope 1, 2, and 3 emissions, they deduct the S4 emissions that are avoided by using the energy product compared with the most likely counterpart.

After getting all the Scope 1, 2, and 3 emissions, they deduct the S4 emissions that are avoided by using the energy product compared with the most likely counterpart.

Why Get Started With Scope 4?

Disclosing S4 emissions is voluntary; it doesn’t count towards a company’s total emissions reductions. It remains a theoretical estimation using a reference scenario.

Avoided emissions also is in its nascent stage but improving transparency and standardizing measurement methods will drive value to investors.

The calculation of this metric enables companies to determine how capable their product is in helping decarbonize their business. Taking into account Scope 4 disclosures makes sense from a decarbonization perspective. It can also provide financial insight as it reveals the real added value a business is making toward its sustainability agenda.

Ultimately, while carbon accounting including all scopes of emissions won’t be an easy task, it’s essential to guide companies, their investors, and other stakeholders to better understand how they are progressing towards their climate and corporate sustainability goals.