The global aviation industry’s main carbon offset program is at a key point. With less than two years until airlines meet their first CORSIA obligations, a new report from Sylvera warns of a potential supply shortage. This could lead to higher carbon prices and increased compliance risks.

CORSIA, launched by the International Civil Aviation Organization (ICAO), is the first global market-based plan for aviation emissions. Airlines must offset emissions from international flights that exceed 85% of 2019 levels. The first phase, from 2024 to 2026, addresses current emissions. However, airlines won’t need to retire eligible carbon credits until January 31, 2028.

Sylvera thinks airlines may be underestimating the challenges ahead, even if the deadline feels distant

CORSIA Demand Is Rising, But Eligible Supply Remains Scarce

By 2026, 130 countries will join CORSIA, one of the world’s largest carbon compliance systems.

Sylvera estimates that CORSIA’s first compliance phase could create demand for about 163 million eligible emissions units (EEUs). This excludes intra-European Economic Area flights already covered by the EU Emissions Trading System and smaller aviation markets. Demand could rise to 198 million credits under full implementation.

The challenge is that eligible supply is well below these numbers.

Currently, only 38 million carbon credits qualify as EEUs, covering just 23% of expected demand. Around 300 million credits have been issued, but many are stuck due to extra authorization requirements.

- This situation leaves a supply gap of about 125 million credits.

The shortage comes from two main hurdles in Article 6 of the Paris Agreement: Host-country Letters of Authorization (LoAs) and Corresponding Adjustments (CAs) or approved insurance mechanisms. Without these approvals, carbon credits can’t be used for CORSIA compliance, even if issued.

The Article 6 Bottleneck Is Slowing the Market

Article 6 rules have changed how carbon credits are used in international markets.

Host countries must formally authorize credits for international use and adjust their emissions accounting to avoid double counting. While this strengthens environmental integrity, it creates a significant administrative bottleneck.

Sylvera reports that only 24 countries have issued LoAs, and just five have reported corresponding adjustments. The company estimates that only 21% of assessed countries are likely to meet both requirements.

Even with optimistic views, the outlook remains tight.

By January 2028, potentially eligible credit volumes could reach 640 million. But considering authorization risks, likely eligible supply drops to around 104 million credits. Fully confirmed eligible supply is only about 48 million credits.

This gap makes many analysts view authorization risk as a key factor in carbon markets today.

Airlines Are Waiting—But Waiting May Become Expensive

One striking finding is the low level of buying activity. Despite airlines facing compliance obligations for 2024-2026, only around 400,000 tonnes of CORSIA credits have been retired—about 0.2% of expected demand.

Many airlines are waiting for clearer signals from regulators before spending money.

However, Sylvera warns that delaying credit purchases could lead to a supply squeeze. If airlines wait until 2027 or early 2028, liquidity might dry up just as demand peaks.

This situation echoes concerns from market intelligence firm Abatable, which has warned that CORSIA demand could exceed available supply in its second phase if new projects don’t enter the market.

Several Factors Could Reduce Demand

While supply issues dominate discussions, demand is also uncertain. Sylvera identifies three key factors that could lower total compliance needs.

1. Geopolitical Tensions

The report notes that ongoing disruptions from the US-Iran conflict could cut international aviation activity. This may reduce CORSIA demand by 4% to 9%. Depending on how long these disruptions last, demand could fall to between 149 million and 157 million credits.

2. Europe’s CORSIA Review

The European Commission is reviewing how CORSIA interacts with the EU ETS.

If flights from the European Economic Area shift entirely to the EU ETS, CORSIA demand could drop by about 24%, lowering it to around 123 million credits.

This review is crucial because Europe is a major source of compliance demand. Market players worry that new EU eligibility rules could shrink the pool of acceptable credits.

3. US Airline Participation

While the US is part of CORSIA, domestic enforcement remains unclear.

Sylvera estimates that if major US airlines opt out of full participation, demand could fall by roughly 18%.

Still, some airlines in Asia may continue to buy credits voluntarily. Japan Airlines, All Nippon Airways, Singapore Airlines, and Scoot have already retired credits for future compliance.

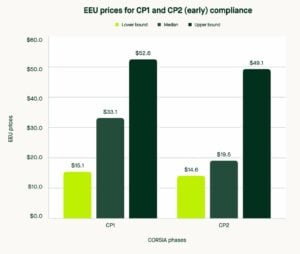

Carbon Credit Prices Could More Than Triple

The uncertainty around supply and demand complicates price forecasting.

Currently, CORSIA markets are thinly traded with limited transaction data. However, Sylvera’s models across 50 scenarios suggest significant upside risk.

The firm projects three possible outcomes for first-phase compliance credits:

- Low case: about $15 per credit

- Base case: about $33 per credit

- High case: approximately $53 per credit by January 2028

The highest-price scenario assumes ongoing authorization bottlenecks, limited supply growth, and a late rush in airline buying. If this occurs, compliance costs could rise sharply for the aviation sector.

Billions of Dollars Are at Stake

The financial stakes are certainly high. Sylvera estimates total airline exposure at around $2.4 billion under a $15-per-credit scenario. If credits hit $53, costs could soar. The top ten airlines alone might face about $3.8 billion in procurement costs.

Since compliance obligations are based on past flight activity, airlines have few options to lower their exposure. Their main strategy is timing—when and how they secure credits.

The Road to 2028

Despite uncertainties, most market observers expect CORSIA to succeed.

Countries continue to develop Article 6 frameworks. Authorization systems are improving, and governments increasingly see the economic value of joining international carbon markets.

However, the next 18 months may determine if CORSIA becomes a smooth compliance market or faces a supply crunch that drives prices higher.

For airlines, project developers, and investors, Sylvera’s message is clear: the compliance deadline may be in 2028, but today’s market is already taking shape.