Mayfair Gold is aiming to be the first carbon neutral gold project in Canada by using carbon credits to offset their project in Ontario.

The Canadian mineral exploration company is focused on sustainably advancing its 100% owned Fenn-Gib gold project in the Timmins region of Northern Ontario.

The firm stated that its Fenn-Gib venture is now Canada’s first carbon neutral gold project. And that’s after Mayfair completed its carbon credit purchases to offset its 2021 emissions, its first year of operations.

Carbon Credits for Mayfair’s Gold Project Emissions

A Toronto-based company Carbonzero conducted an independent assessment of Mayfair’s CO2-equivalent GHG emissions in 2021.

Carbonzero focuses on the design and implementation of corporate carbon reduction strategies and solutions. It helps firms measure, report, and reduce their emission.

Carbonzero revealed that Mayfair emitted 738 tons of CO2e. In particular, the assessment covers the company’s total emissions. These include Scope 1, Scope 2, and material Scope 3 emissions.

The emissions were mainly related to Mayfair’s exploration activities at Fenn-Gib, where a total of 54,741m was drilled in 89 holes.

The Fenn-Gib project comprises ~4,800ha, of which more than 75% is unexplored. It contains 2.08 million ounces of indicated gold resources (NI43-101).

Mayfair Gold hopes to raise gold deposit size to 3 million ounces.

To compensate for Fenn-Gib’s emissions, Mayfair bought carbon offsets from the Thermal Residential Heating Aggregation Project.

Carbon offsets are tradeable certificates (or credits) issued to an emitter when CO2 is removed from (or prevented from getting emitted into) the atmosphere.

The carbon credits Mayfair bought offset its Fenn-Gib gold project 2021 emissions.

The Thermal Residential Heating Aggregation Project replaces traditional residential fossil fuel combustion heating with solar-powered heating systems.

Private residences and other facilities are using the project’s solar heating systems across Canada. And the offsets it generates correspond to the amount of CO2e emissions avoided from getting into the air.

The offsets are being retired on the Canadian Standards Association (CSA) Clean CleanProjects Registry.

Gold: The Most Valued Mined Commodity

Gold is one of the top exports by value for many countries around the world. In developing nations, a growing gold sector results in positive economic effects. These include royalty payments and tax revenues, employment, and business opportunities for local communities.

The gold industry is a key driver of economic activity in Canada and it employs around 400,000 Canadians. It also provides the highest average annual industrial rate of pay in the country as per Mayfair’s CEO Patrick Evans. He said that:

“Gold is Canada’s most valuable mined commodity, valued in excess of $12 billion annually… The future of the industry depends critically upon sustainable development. At Fenn-Gib, we are laying the foundation for Canada’s first carbon neutral gold mine.”

He also added that Mayfair’s commitment started when the firm acquired Fenn-Gib. The firm will continue through its exploration, mine development, operations, and eventual closure.

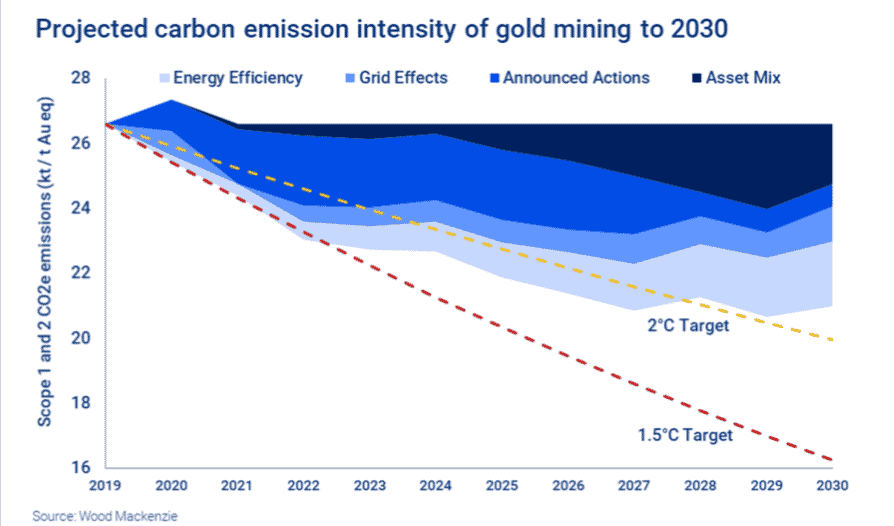

But GHG emissions from gold mining activities still pose serious climate concerns.

Estimated emissions for the global gold market are around 126.4 Mt CO2-e a year. This equates to the emissions intensity of 28,700 kg CO2-e/kg gold for Scopes 1 and 2.

The major factor for the increasing emissions of gold over time is declining gold ore grades.

The chart below plots the projected progress of gold miners in reducing emissions intensity to 2030. The forecast is against the reductions necessary to align with 2°C and 1.5°C climate goals.

Even if gold mining emissions are not that huge, still gold producers seek ways to offset their carbon footprint to help fight climate change.

Mayfair’s carbon credits purchase for offsetting its gold project is one among the many other initiatives in the industry.

Australian-based Karora Resources has also announced reaching its carbon neutrality in 2021. The multi-asset mineral resource company also bought and retired verified carbon offset credits.

Mayfair Gold plans to provide a resource update in the third quarter of this year. While the preliminary economic assessment of its Fenn-Gib project will be over by the last quarter.

Mayfair successfully completed its metallurgical testing last March. It also confirms that the Fenn-Gib deposit can deliver robust gold recoveries. And that’s through both whole ore cyanidation (84.3% recoveries) and flotation (94% recoveries).

The Net Zero Asset Managers (NZAM) was launched in December 2020 with 30 asset managers representing about $9 trillion in Assets Under Management (AUM).

It has grown to now include 273 firms, representing over $60 trillion in assets under management.

The group’s main purpose is to encourage asset managers to support the goal of net zero by 2050. This is in line with global efforts to limit warming to 1.5°C.

The recent additions include the T. Rowe Price, Credit Suisse Asset Management, and Frontier Investment Management. While old members like AXA Investment Managers and Aviva Investors made their initial goals more ambitious.

Marco Morelli, AXA Investment Management Executive Chairman said:

“Since our first submission in October, we have further intensified our efforts across the whole business to develop an approach which is robust and can be implemented in an effective manner by investment teams… Meaning our revised figure now stands at 65% of total assets managed in line with net zero by 2050.”

NZAM Asset Managers Net Zero Commitment

NZAM is part of the Glasgow Financial Alliance for Net Zero (GFANZ). Six Founding Partner investor networks formed the group namely:

Asia Investor Group on Climate Change (AIGCC),

CDP Global,

Ceres,

Investor Group on Climate Change (IGCC),

Institutional Investors Group on Climate Change (IIGCC), and

Principles for Responsible Investment (PRI).

NZAM asset managers’ commitment to transitioning their investment portfolios to align with the net zero emissions by 2050 is by far the biggest initiative there is.

According to IIGCC CEO, Stephanie Pfeifer:

“While there is some way to go, that $16 trillion of assets are now committed to being managed in line with achieving net zero by 2050, is a more than positive start – although targets must of course still translate into action.”

Signatories to the group agree to carry out a series of commitments including:

Setting interim targets for 2030 for the proportion of assets under management (AUM) in line with achieving net zero emissions

Review those goals every five years to ensure that the proportion of AUM covered by their net zero commitment increases up to 100%

Working in partnership with asset owner clients on their decarbonization goals

The set targets will see to it that asset managers assure real reductions in emissions at the businesses they invest in.

As per the NZAM’s report, the group members manage a total of $61 trillion in assets.

83 of the signatories who are managing $42 trillion have set their initial targets so far.

This translates to a total of $16 trillion of assets committed to meeting net zero emissions targets.

24 have tied 100% of their assets to the target. Meanwhile, 19 others have committed more than 75% of the funds they manage.

Rebecca Mikula-Wright, CEO of the AIGCC and the IGCC, noted that in the 18 months since NZAM formed, the world’s biggest asset managers have started setting targets and getting their portfolios on track for net zero by 2050. She further said that:

“This momentum must continue; climate is a risk that can’t be divested from… so investors will need to use their influence over capital flows, their influence on companies and their voice to policy-makers to speed up the transition to a net zero global economy.”

The Challenge in Setting Net Zero Emissions Targets

NZAM’s report noted that the geopolitical backdrop for target setting is “increasingly challenging”.

The group cited the increased politicization of ESG issues and changes in the regulatory and policy environments.

The report also highlighted some key themes that emerged during the target disclosure and review process. In particular, firms have different business models or approaches to the net zero transition process.

Also, some asset managers with varied clients across funds may face a lengthier process to align their AUM with net zero. But asset managers with concentrated funds may have more flexibility in aligning their assets.

Other big asset managers have voted against shareholders (from major banks that signed up to GFANZ) who desire to embrace climate goals.

Environmental ministers from the G7 major industrial countries agreed to end financing for international coal-fired power generation and to speed up the phasing out of coal plants by 2035.

G7 or the Group of Seven is an intergovernmental organization made up of the world’s largest developed economies. These are Canada, France, Germany, Italy, Japan, the UK, the U.S., and the European Union.

The group agreed that it will phase out coal-fuelled power during its annual meeting in Germany. They also reaffirmed decarbonizing the electricity sector by 2035.

This commitment will especially impact Japan as it strongly depends on coal-fired power plants.

Unabated coal-fired plants are those that don’t use technology that captures and uses CO2.

Carbon capture and utilization technologies are one of the hottest trends in the carbon market today. They hold great promise to slash emissions by capturing CO2 and putting it into meaningful uses.

The G7 Promise: $100 Billion Each Year

The ministers from Group Seven advanced climate action, energy security, and environmental protection.

Their pledge marked the latest in a global push for governments worldwide to end public funding for fossil fuel projects. This move from the G7 nations is to also help developing nations grow their economies without depending on coal-fired power.

In particular, they plan to speed up reductions in using Russian natural gas and replace it with clean power instead. The wealthy nations also expressed intentions to have zero-emissions vehicles by 2030.

Bronwen Tucker, public finance campaign co-manager at Oil Change International, said:

“The G-7 committing to end public finance for fossil fuels and shift it to clean is a massive win… We now need concrete action, not just words.”

Indeed, the richest countries committed over again to generating at least $100 billion each year in climate financing to help poorer countries deal with the effects of climate change and boost clean energy.

Yet, that figure is only a fraction of the funding needed to achieve those goals. And the wealthy nations have yet to remain true to that promise.

In fact, President Biden didn’t even succeed in convincing Congress to provide the amount (over $11 billion a year) he asked to fight climate change.

Even the private sectors in the G7 nations need to pump up financing, making it trillions rather than billions.

This is in line with the IEA’s analysis that developed countries need to invest $1.3 trillion in renewable energy, at the least. This means they have to triple investments in clean power and electricity during this decade.

Funding support for the transition from fossil fuel economies to sustainable and clean energy sources gained steam recently. This is despite the fact that this is happening very slowly as it should be.

To meet the Paris Accord on climate change, the world has to limit global warming to the critical 1.5⁰C.

And a big part of that is to phase out the use of coal-fired power plants that the G7 is promising.

What’s more, other countries should also be doing the same to further cut global emissions.

A bigger pact during the U.N. Glasgow climate conference (COP26) where over a hundred nations also committed to stopping the use of coal. But two of the biggest users of coal, the U.S. and China, didn’t join the agreement.

Yet, the U.S. along with other countries decided to have a separate pact to end using public money on global projects that use coal. Doing so will divert about $18 billion each year from fossil fuel projects to clean energy projects.

Real Deal with G7 Coal-Fired Power Generation at Home

However, the pledge to restrict tax money on fossil fuel projects is not affecting what nations do at home.

For instance, Japan, China, and South Korea didn’t sign the COP26 agreement. These three countries make up almost half of the international financial support for fossil fuel projects.

Still, cutting the flow of investments to unabated coal-fired power plants is vital not only for the G7 but for the entire world to meet climate goals.

In particular, there must be no more fossil fuel development after 2050 for the world to reach net zero emissions by that year.

The good side is that even if the shift to clean and renewable energy is slow, some governments have made some progress in scaling back dependence on coal-fired power generation.

Take for example the case of the U.K. This G7 member proposed a windfall profits tax in the form of a 25% surcharge on “the extraordinary profits the oil and gas sector is making.” This tax policy will raise 5 million pounds aimed to help pay for the cost of living in the UK.

Meanwhile, the British government also proposes a huge tax deduction to entice oil and gas companies to invest in projects in the country. This deduction would double tax relief for businesses that invest in the UK, covering 91% of those investments.

Other G7 countries are also citing similar actions to eventually phase out coal-fired power plants by 2030.

Canada reinforced the need to shift to clean energy sources and support for developing countries to phase out coal. Its promise involves $1 billion in funding for the Climate Investment Funds Accelerated Coal Transition initiative.

Steven Guilbeault, Canada’s Minister of Environment and Climate Change stated that:

“The world cannot wait – we must continue to mobilize and deliver action. G7 leaders have clearly said that securing energy security and fighting climate change are mutually reinforcing goals.”

It’s crucial that G7 leaders seek ways to ramp up the shift to cleaner energy.

But reducing global emissions, in the long run, places the developing nations in dire need of big funding to adopt greener and cleaner ways to do business than relying on fossil fuels.

Climate activists have been asking U.S. oil major companies to consider total emissions reduction but shareholders’ vote this year seems to be waning.

In their annual meeting this year, a majority of Chevron and other firms’ shareholders voted against a proposal to have overall emissions reduction targets.

Major oil and gas producers have come under mounting pressure to cut greenhouse gas emissions and do more to fight climate change.

Climate-related shareholders’ proposals at the oil majors centered on two main issues: emissions reduction targets and methane emissions.

But major oil firms this year flipped the script and won over investors with their climate change plans. They’re worried about energy security and fuel prices outweighing environmental resolutions.

Many of them have set targets for reducing their direct and indirect emissions (Scope 1 and 2 emissions). But they tend to ignore action plans to cut down their Scope 3 emission targets.

This is evidenced by shareholders’ votes in major oil companies falling short to force the firms to cut their overall emissions.

Shareholders Vote on Chevron Emissions Reduction Targets

Shareholders of Chevron voted against the proposal calling for the firm to set more rigorous targets to reduce GHG emissions.

As per Chevron’s preliminary report, only 33% of the investors voted for the proposal. This is a significant change in the firm shareholders’ stand on this matter.

Last year, 61% of shareholders voted in favor of a similar emissions reduction proposal.

Chevron’s CEO, Michael Wirth, told shareholders that the firm plans to focus on reducing the carbon intensity of its operations. He said,

“We aim to lead in lower carbon intensity oil, products, and natural gas, and to advance new products and solutions that reduce the carbon emissions of major industries.”

The oil major also said its 2022 capital spending will be more than 50% higher than in 2021. This includes the company’s announced acquisitions earlier this year.

The votes come as historic profits by oil majors like Chevron eclipse concerns about the climate crisis. Similar proposals at other oil firms also failed to win enough shareholders’ votes.

Investors Vote Against Scope 3 Emissions Reduction

A climate activist group “Follow This” asked U.S. oil companies to directly reduce their GHG emissions. The company won a court order last year requiring Shell to cut its emissions.

Yet in London, support for Shell’s climate plan declined 10% points to only under 80%. And support also fell for a resolution brought by Follow This to only 20.3% of votes cast, down from about 30% last year.

Shell urged shareholders to reject the resolution saying that:

“The Company has set ambitious targets in line with the 1.5°C goal of the Paris Agreement… Its strategy supports an orderly transition, one that maintains the supply of oil and gas where it is still needed… and that accelerates the shift to low- and zero-carbon energy.”

ExxonMobil also shows the same trend in shareholders’ position on the firm’s emissions reduction plan.

Shareholders voted down a resolution from Follow This to set targets for reducing its customers’ (Scope 3) emissions.

Only 28% of the votes that were cast supported the proposal. If approved, the proposal would have reduced the sales of fossil fuels. It will also make Exxon set and report its targets for cutting overall GHG emissions.

Exxon CEO Darren Woods said that the firm is expanding investments in fossil fuel production. This is to minimize a global energy shortage and the rising prices for consumers. Woods said:

“We don’t believe scope 3 targets are an effective way to manage total society emissions… Access to reliable energy is foundational to our daily lives.”

Investors’ votes at ConocoPhillips Co. and Occidental Petroleum Corp. also failed to support the climate proposal this month.

58% of shareholders in ConocoPhillips have voted for a proposal by Follow This last year. But the support has also reversed with only 39% of favored the group’s proposal to set total reductions targets.

Likewise, Occidental Petroleum Corp. shareholders rejected the same proposal during its annual meeting this year. In fact, shareholders voted 83% against setting more rigorous targets for emissions reduction.

Investors in all five oil companies have cast their votes on the total emissions reduction proposal and the majority of them decided to go against it.

Carbon credit standards certifier, Verra, announced that it will ban the tokenization of retired carbon credits by crypto companies.

Verra released a statement elaborating its position on how carbon credit tokenization should occur:

“Verra will, effective immediately, prohibit the practice of creating instruments or tokens based on retired credits… on the basis that the act of retirement is widely understood to refer to the consumption of the credit’s environmental benefit.”

The largest carbon standard also intends to explore the possibility of “immobilizing” carbon credits. The purpose of this new proposal is to boost the transparency and traceability that market players demand, according to Verra.

Carbon Credits Tokenization Scaling Up

Carbon credits are bought by companies to offset their carbon emissions. And Verra is by far the biggest body that verifies and certifies carbon credits.

Many blockchain and crypto platforms that offer tokenization use Verra registered carbon credits. They mark those credits as ‘retired’ on the registry before tokenizing them to avoid double-spending.

The Verra Registry started certifying voluntary carbon credits in October 2020. One year after, the Toucan protocol was launched and tokenized about 22 million tons of carbon credits.

KlimaDAO also offers tokens to enable users to offset their carbon footprint. It uses tokenized credits from Toucan, Moss, and C3.

New tokenization initiatives are still being launched and this week a blockchain startup Flowcarbon co-founded by WeWork Adam Neumann raised $70 million. The Deutsche Börse Group also invested in the carbon trading platform AirCarbon Exchange.

Responses to Verra’s Announcement

Market players positively welcomed Verra’s decision to stop tokenization based on retired carbon credits. Its proposal to create tokens based on immobilized credits also stirred positive responses.

As per Verra, immobilizing carbon credits is a possibility,

“provided that this can be done in a way that prevents fraud and upholds environmental integrity.”

Toucan Protocol, whose tokens represent around 2.4% of Verra’s total carbon credits, is supportive of the proposed change. It creates the BCT or Base Carbon Tonnes tokens.

BCT is a standardized contract reflecting VCS-certified credits with a 2008+ vintage. Before being tokenized into BCT, Verra’s credits are retired by Toucan Protocol.

Toucan issued its own response:

“Even better, connecting our registries in this way opens the door to a process where tokenized credits could be transferred back from a blockchain onto their source registry.”

Toucan also believes this approach would enable all carbon credits to gain the benefits of tokenization on a public blockchain. These include:

The immediate global settlement

Double-spend protection

Transparent traceability

Enhanced market access

Connections to Decentralized Finance (DeFi) applications.

Toucan further added that:

“Beyond these benefits, connecting on-chain and off-chain registries would allow credit prices on each market to maintain parity. This would dramatically reduce the price risk of one-way tokenization.”

Another major carbon blockchain company Klima DAO responded to Verra’s decision, by stating:

“The move by Verra to open up discussions on credible pathways for carbon credit tokenization is considered a broadly positive move forward for the Web3 carbon space.”

The group also requested Verra to offer a higher degree of collaboration with the on-chain carbon market when setting up the new product. Klima DAO added:

“immobilizing credits off-chain when they are bridged presents an elegant solution to the double-spend problem.”

Moss Earth’s (creator of the MCO2 token) CEO Luis Adaime stated that Verra’s move was an improvement on the status quo:

“It is not a prohibition, just a different way of doing it. New tokens will just have to incorporate data on the projects and vintages… And then keep the underlying credit “immobilized’ instead of “retired”.

He further said that Verra is only being open to blockchain usage recognizing that tokenization is here to stay. In fact, the certifier intended to launch a public consultation about this matter.

Other market players also commented on a positive note about Verra’s proposal.

A carbon trader welcomed the improvement promised by Verra’s announcement saying:

“Creating another status makes the distinction between retired credits and credits that are brought on-chain a bit clearer for people outside the crypto/blockchain community.”

Also, a carbon project developer and trader noted that:

“More transparency in the crypto space means more (and better) buyers and the increased possibility of selling.”

Right now, there’s plenty of end-user demand being met. So most market participants think Verra’s decision won’t make a huge impact on the voluntary carbon market.

Here’s how things will change with Verra’s new proposal for carbon credits tokenization.

At the moment, bridging companies are buying the credits in large quantities from the market and retiring them afterward. They would then mint the credits to make tokens and resell them. Buyers of tokens can burn their credits when they offset them for their emissions.

Under the new proposal, the crypto firms would buy credits in large volumes, mint them, sell them, and retire them only when the buyer of the tokens decides to burn them… Or use them for offsetting purposes.

In effect, credits and tokens would coexist on Verra’s registry and on the blockchain until they are offset.

Are you wondering how much carbon dioxide you release into the air? Then you may want to know what is your carbon footprint.

Every time you do something that burns fossil fuels, you emit carbon into the atmosphere. If you’re driving a car, flying in a plane, eating something, or only watching TV, you’re emitting carbon.

Your home or the building you’re living in also factors into your personal emissions.

Some people emit more carbon dioxide than others. But your individual carbon footprint is a part of the total emissions released into the air. It all adds up.

So, it’s crucial that we know our individual carbon footprints and how we can reduce them. It will help the world’s quest to reverse the disastrous climate change effects.

This guide will help you know how much CO2 you’re emitting and what are the ways you can do to reduce it.

What’s Your Individual Carbon Footprint?

According to WHO, a carbon footprint is a measure of the impact your activities have on the amount of carbon dioxide released into the air.

These CO2 emissions are through the burning of fossil fuels and are expressed in tons. They also include emissions including other GHGs like methane and chlorofluorocarbons (CFCs).

Globally, the average individual generates about 4 tons of CO2 each year. But each person in the U.S. produces about 16 tons of carbon in a year. In other countries, averages vary a lot with higher emissions found in developed nations.

Yet, the average global CO2 footprint a year has to drop to 2 tons by 2050 for the world to have the best chance of avoiding a critical 1.5℃ rise in temperature.

And cutting the individual carbon footprint to only 2 tons won’t happen overnight.

But it’s possible through small changes in daily actions such as eating less meat or line drying clothes.

Transportation and household energy use are the biggest parts of an individual’s carbon footprint.

For example in the U.S., about 40% of total emissions during the 1st decade of the 21st century were from those sources. They’re the primary carbon footprint of individuals over which they have direct control over it.

Secondary carbon emissions usually refer to the consumption of goods and services. Food production includes this, for instance.

Take for example the case of producing a bottle of water a person drinks. Its carbon footprint includes the emissions released during its manufacture. Add to this the emissions of shipping the product.

Hence, your own carbon footprint is a vital means to understand the impact of your actions on global warming. This is why it’s important to measure and keep track of your emissions if you want to help fight the climate crisis, at least on an individual level.

So, how do you know what’s your personal carbon footprint?

How to Measure Your Own Carbon Footprint

You can figure out how much your actions generate GHG by using a carbon footprint calculator.

There are plenty of various tools created for calculating carbon footprints for individuals. But they’re different from the ones used to calculate carbon emissions by businesses and other entities.

Emissions by companies are often measured using a more complicated, scientific approach. And most businesses need to follow certain regulations to offset their emissions.

Calculating the offset they need to reduce or avoid footprint usually involves buying carbon credits. They’re permits given to companies in relation to their emissions.

Carbon offset credits have been on the rise due to the urgent need to mitigate climate issues. Large businesses are using them to address their big carbon footprint.

Here’s our complete guide to understanding how the emissions offset scheme with carbon credits works.

A carbon footprint calculator for an individual considers the GHG you emit at home. It may also include the emissions you contributed when traveling.

This calculator allows you to compare your footprint with national and global averages. There are a couple of online CO2 footprint calculators you can use.

In the U.S., there’s the Environmental Protection Agency. For those in the UK, as well as for others from different nations, the WWF calculator is helpful. While the one from the United Nations is useful for people from all parts of the globe to use.

Not all online calculators are the same. But they’re asking for similar pieces of information from you to calculate your individual carbon footprint.

Example questions are:

What is the size of your household,

What your diet is,

How often you dine out,

How much do you drive using different transport vehicles,

The frequency of your flight,

What kind of energy you’re using at home,

How much energy you’re consuming,

Your recycling practices, etc.

In essence, they’re asking for details about your household, travel, and lifestyle. The images below show some samples of the personal carbon footprint results generated by the calculators.

UN footprint calculator resultsWWF footprint calculator results

The result you’ll get after providing the information may not be 100% accurate.

That’s understandable though as there are a lot of factors affecting the standard values the calculators are using. Plus, the numbers you may provide are only estimations and not the exact amount you actually used.

Take the emissions of eating meat, for instance. While eating meat emits higher carbon than vegetables, it still depends on where you buy the meat. If you buy it locally, then it has fewer emissions.

Not to mention that the estimations you give and calculated don’t account for goods and services that come with them. So, what matters is to get your average individual carbon footprint.

Using those online calculators is a good way to start understanding your personal emissions. And from there, you can work on how to improve and reduce your carbon footprint.

How to Reduce Carbon Footprint?

As we can suggest from the situation above, it’s not easy to get your exact emissions. But you need to make estimations to have something to base your reduction efforts on.

Your car may pollute less than the average value used. Or perhaps the meat you buy is less polluting as it’s sourced from your locality. Yet, the fact remains that they’re major emission sources.

Hence, it’s still possible to reduce your footprint in a more accurate way by using numbers that reflect your local reality.

Organizations tackling climate issues recommend ways on how people can cut their footprint.

The WHO, in particular, suggests some areas where you can reduce your individual carbon footprint. They tell on what behaviors are sustainable in cutting down emissions. Here are some examples you may consider.

Areas for Reducing Carbon Footprint

Transportation: Suggested Actions/Behaviors

Avoid polluting car journeys – each liter of fuel burnt emits over 2.5 kg of CO2

Favor walking, cycling or using public transport, especially trains

If you are driving, share the ride with others and don’t speed as it uses more fuel and thus releases more carbon

You can offset your flight footprint by paying extra for offset credits, or partaking in digital carbon exchanges

Energy Use: Suggested Actions/Behaviors

Pay attention to the temperature of your house – a 1ºC less lowers your footprint (and your bill) by up to 10%

Set your devices so that they’re turned on only when you’re home, and mind their settings to be in the right temperature level

Use energy-efficient lights like LED and turn them off when not needed

Unplug cellphone chargers even if not connected to phones as they still drain electricity

Enhance home insulation to get rid of using more devices

Opt for a greener electricity supplier (uses renewable energy) to help promote low carbon sources

Food: Suggested Actions/Behaviors

Lessen your consumption of animal products

Eat locally-produced foods – they generate less pollution

Recycle or compost organic waste to avoid methane emissions by decaying this waste in landfills – in the EU, this kind of emission accounts for ~3% of GHG emissions.

Waste Management: Suggested Actions/Behaviors

Reject what you don’t need and reduce what you need

Reuse or repurpose wastes as many times as possible

Avoid buying new bags to bring your shopping items home by bringing your own shopping bag

Pick products with little or no packaging – it will cut down production emissions

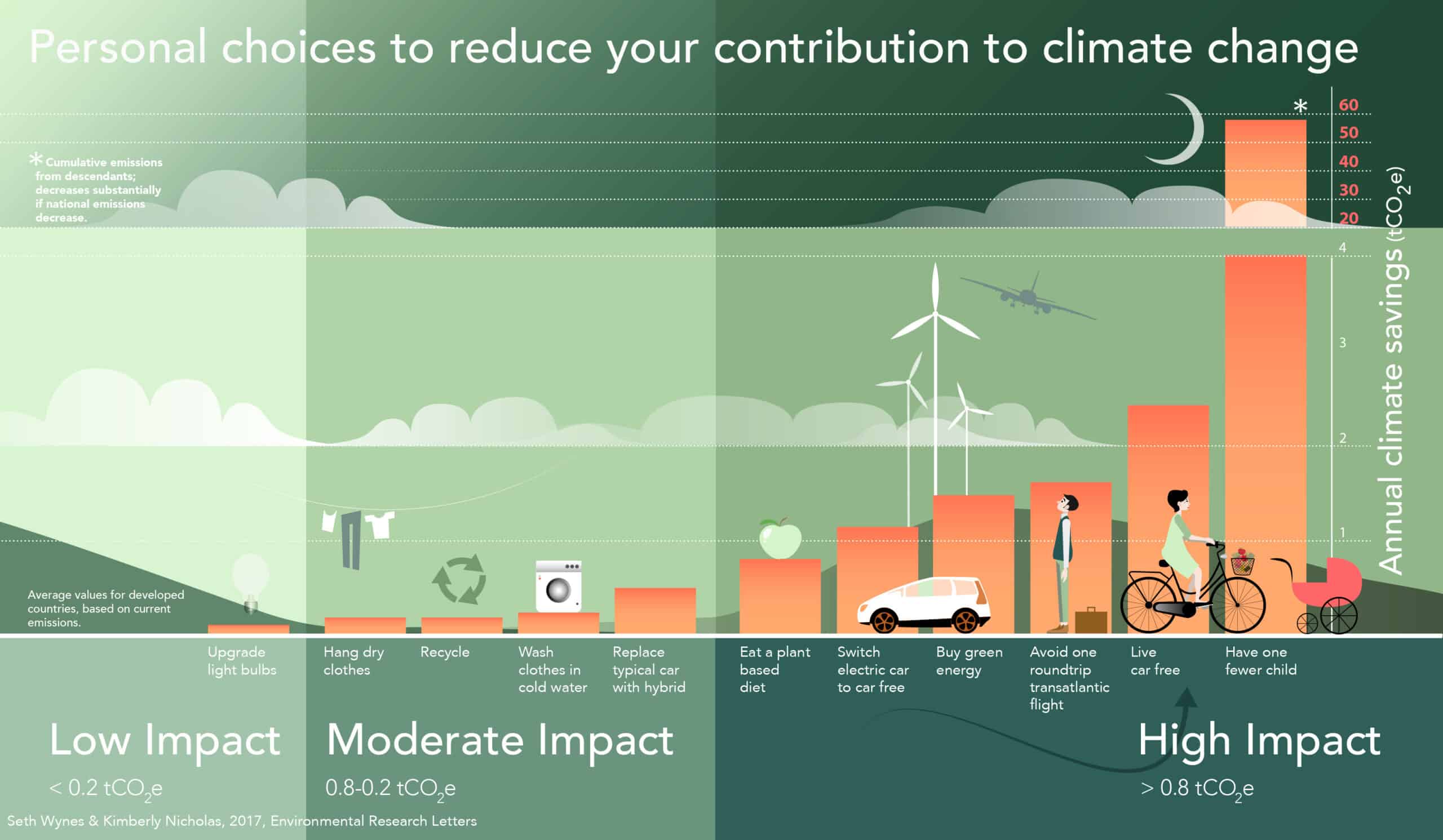

Personal choices that can significantly help mitigate climate pollution such as:

Eating a plant-based diet

Avoiding air travel

Living car-free

Choosing to have smaller families

The image below illustrates some ways to cut down a personal CO2 footprint.

Why do Individual Efforts to Fight Climate Change Matter?

Many people want to know what they can do individually to help tackle climate issues. In such a case, they need to know how their actions can have the biggest possible impact.

Climate change is a problem for the entire planet. In essence, climate science tells us that having a good future on Earth depends on reducing the total carbon footprint by about 90% by 2050.

The best time to act would have been years ago. Yet the next best time is now. And the sooner we take action to cut footprint, the more options we have to win the fight.

Hence, the actions you make today to cut your personal carbon footprint will make a huge difference in the future. It will add up to other individuals’ efforts of reducing their own emissions.

The European Union plan to tap its carbon market for €20 billion ($21.4 billion) by selling 250 million Market Stability Reserve (MSR) credits. The funds will go towards helping ease the transition to phase out Russian fossil fuels while respecting the emissions cap.

The 20 billion-euro plan won’t compromise the EU’s long-term green goals, as per the emissions trading system’s (ETS) architect.

The revelation of the plan caused carbon prices to fall as investors criticized the EU for such a move. They said that it shows a lack of political predictability from the bloc and may weaken its Market Stability Reserve (MSR).

MSR is a supply-control mechanism that helps drive emissions costs to record levels.

But for Jos Delbeke, a former European Commission (EC) climate official and ETS architect, the EU’s proposal to sell around 10% of carbon credits held by MSR is justifiable.

EU’s Plan to Sell 250M Carbon Credits from MSR

The EU’s plan is a defendable way to raise climate funds according to Delbeke.

He said that the release of the MSR shows that the EU is willing and able to deal with the issues and trade-offs that the energy transition calls for. He further said:

“It’s a “wholly defendable way” of raising funds amid exceptional circumstances while respecting a cap on pollution.”

The 10% percent translates to about 250 million carbon credits or permits that allow a certain amount of carbon emissions.

Carbon credits are used by companies to offset their emissions. For every carbon credit bought, one metric ton of carbon is offset through an environmental project like reforestation.

The attack on Ukraine by Russia, Europe’s major gas supplier, drove the EU to rethink its energy policies amid grave concerns of supply shocks.

Hence, the bloc decided to ditch its dependency on Russian fossil fuels via its REPowerEU plan. And that will cost the region some €20 billion or $21.4 billion in carbon credits auctions.

These measures need a mix of EU laws and recommendations to the EU’s 27 member states.

This bold climate policy requires 210 billion euros in extra investments by 2027 and 300 billion euros by 2030 to meet the EU’s 2030 climate target.

The investments will also slash Europe’s fossil fuel import bill and include the following components:

86 billion euros for renewable energy,

27 billion for hydrogen infrastructure,

29 billion euros for power grids, and

56 billion for energy savings and heat pump

Opposing Views on REPowerEU Plan

At the end of last year, the EU’s MSR held 2.6 billion carbon credits. The proposal won’t affect the reserve’s purpose to reduce surplus carbon permits and boost market resilience, as per the EC.

Under the proposal, there’ll be amendments to the regulation on the MSR. In particular, it will release carbon permits until the end of 2026 when auction sales hit €20 billion.

The European Investment Bank will perform the sales.

But others are uncertain about the plan’s impact on the market.

The head of carbon markets at a financial service company noted that:

“The key of the whole MSR system is raising trust and credibility in the system; without MSR we would have notional floor prices.”

Likewise, the director of carbon research from Refinitiv stated that:

“The issue now is that people believe that the auction revenues are used for other things than for what it was supposed to do… And the market is triggered by this.”

The price of EU carbon credits was down about 10 euros compared with levels before revealing the plan to sell the permits.

Yet, prices quadrupled over the past two years on expectations that the EU will tighten its climate policies.

Meanwhile, other commentators said that tapping MRS reserved carbon credits will risk the EU’s climate architecture and plunder its ETS.

But then again Delbeke defended that such language is not helpful and is based on a misunderstanding of the purpose of the MSR. He added that,

“The spike in EU ETS prices is boosting costs for EU companies… And “a moderate increase” in the supply of allowances [carbon credits] in the shorter term would be a relief.”

The EC president, Ursula von der Leyen, also justified the EU’s plan to sell MSR carbon credits reserves. She said that RePowerEU will help the bloc save more energy and speed up the phasing out of Russian fossil fuels. And most importantly, it will kickstart investments on a new scale.

While for Mette Quin, EC’s deputy director of carbon markets,

“We have done the assessment and we know that we need 250 million allowances [carbon credits] to be auctioned to meet the REPowerEU goals. The raise of energy prices has a much bigger impact, and the carbon price is only a small fraction of it.”

What does ESG mean? What is the definition of ESG and why invest using its criteria?

Investors have been asking these questions wondering if ESG is the same as CSR. Or how it compares with socially responsible investing and impact investing.

If you also want to know what ESG means, this guide provides a comprehensive definition of the concept. It will also help you understand why using ESG criteria in making investments is all worth it.

ESG Definition and Meaning

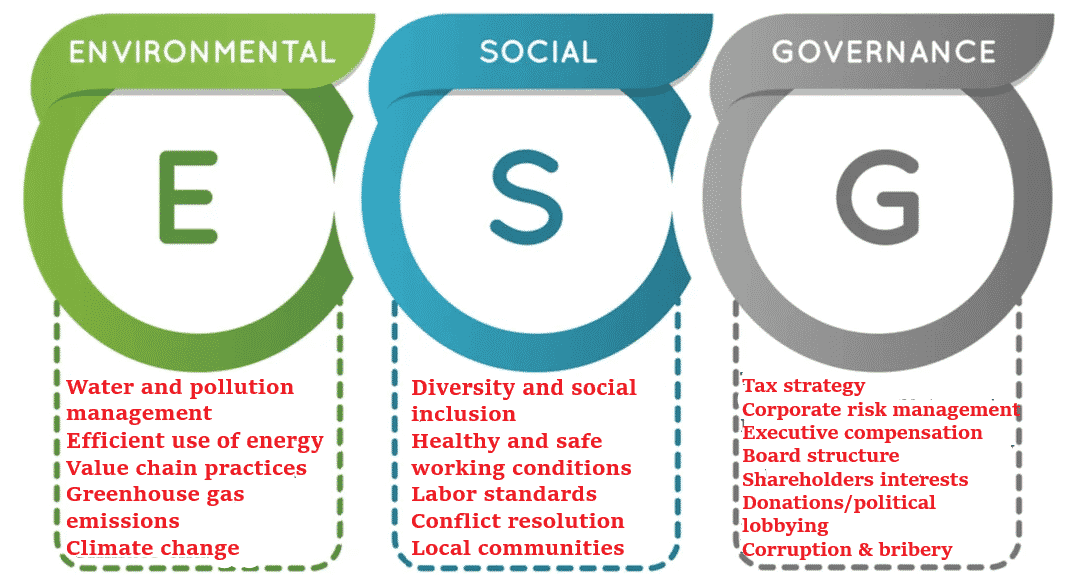

ESG is an acronym for Environmental, Social, and Governance. It refers to the three major criteria used to measure the sustainability of an investment in a business or project.

ESG is a generic term used by investors to assess the behavior of companies and predict their future financial performance. Most socially responsible investors check companies out using ESG criteria to screen investments.

For instance, it’s used to ensure accountability and management of a firm’s carbon footprint. And the number of funds invested using the ESG criteria has been growing so much since the start of this decade.

It’s expected to rise even more as the world shifts to a low carbon economy in response to climate change.

ESG vs. CSR: What’s the difference?

Most often the definition of ESG is taken the same as the concept of CSR – corporate social responsibility. While both terms are quite similar, they’re two different concepts.

CSR is a way of managing a company that accounts for the impact its business activity has on various stakeholders. These include its clients, employees, suppliers, investors, society, and other affected groups.

CSR is all about integrating ecological and social concerns into a firm’s business activities. At the same time, adopting a long-term vision over short-term values.

Yet both concepts care not only about profits, finances, and governance. They also consider the people and the planet to promote sustainability.

Most companies are including their CSR in their ESG reports. Reporting their ESG each year has been the practice for all large businesses, especially for the major airlines.

Those who don’t report their ESG metrics may find it hard to attract investors’ attention.

Responsible investors assess firms using the definition of ESG criteria to screen investments. They can also use it to assess risks in making their investing decisions.

So, let’s find out how companies act on the three ESG criteria: environmental, social, and governance by breaking down each one of them.

ESG Criteria: The Environmental Factors

In essence, environmental factors are about a company’s impact on the environment. They’re based on the idea that business activities can pose risks to the environment.

This criterion looks into how a business acts as a steward of the natural environment. Examples of a firm’s environmental factors can include:

Waste and pollution management

Efficient use of energy

Value chain practices

Greenhouse gas emissions

Climate change

To fulfill this ESG factor, it’s not enough for businesses to only deal with the adverse impact of their activities.

Instead, they need to have a proactive approach that promotes the sustainability of natural resources.

The most pressing environmental concern right now for all businesses is climate change. And so, the common elements of ESG environmental definition include these key actions:

Almost all large businesses today include climate change in their annual ESG reports. In particular, this environmental component often details the company’s strategies for reducing its carbon footprint.

Common climate change strategies include nature-based solutions like avoiding deforestation. While other measures involve offsetting GHG emissions using carbon credits.

The major goal of this ESG factor is to improve profitability without harming the environment. Thus, investment decisions consider any environmental risks a business has. And investors favor projects that show care for the planet.

ESG Criteria: The Social Factors

A firm that follows this part of the ESG definition respects the rights of its employees and of other people affected by its activities. These include clients, business partners, and the local community people.

In other words, social factors have to do with how the company treats and values people as well as meeting the social inclusion criteria. This ESG criterion also involves concerns about employment conditions to protect workers’ welfare.

Overall, it’s all about the impact that a company has on its employees and on society as shown by these practices:

Diversity and social inclusion policies that avoid discrimination

Healthy and safe working conditions

Labor standards across supply chains: fair wages and human rights protection

As a result, firms that integrate social factors into their programs and projects tend to witness better outcomes. For instance, they’ll have high workers’ morale, increased productivity, and lower turnover.

Businesses with socially-responsible ESG practices also find it easier to do their activities. That’s because they don’t face social pressure from people who give them social license to operate.

ESG Criteria: The Governance Factors

This final ESG criterion focuses on corporate culture, policies, and governance. It is about making the responsibilities, rights, and expectations of stakeholders clear so that interests are met.

Values like managers showing commitment to fighting unethical or unfair practices are a strong part of the culture, for instance.

To assess this ESG factor needs clear governance policies and rules. Common examples under which this can be assessed include:

Tax strategy/Fiscal and procedural transparency

Corporate risk management

Executive compensation

Donations and political lobbying

Corruption and bribery

Board structure and brand independence

Protecting shareholder interests

The great benefits of having these governance policies can cover a lot of things. And the biggest one is marrying shareholders’ interests with management to avoid financial pitfalls.

Overall, here are the three ESG criteria combined together.

ESG Criteria: Why use it when investing?

ESG definition and standards are becoming a notable consideration in today’s investment world.

This is because the ESG criteria deal with issues that are vital when measuring the impacts of investment other than financials. Plus, they also have a huge bearing on the rate of return and long-term risk of investment portfolios.

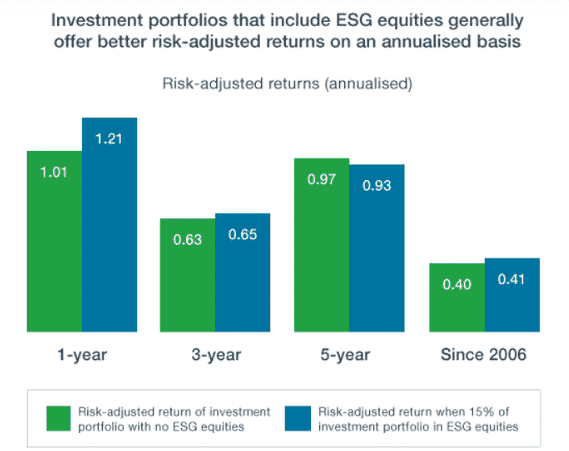

In fact, studies found that investors who choose ESG-screened investments enjoy a ‘double dividend’. This refers to having a lower risk plus a better rate of return or the ratio of income from an investment over cost.

Moreover, ESG investing may end up helping investors build a better investment allocation. It means integrating ESG sustainability factors results in lower risks.

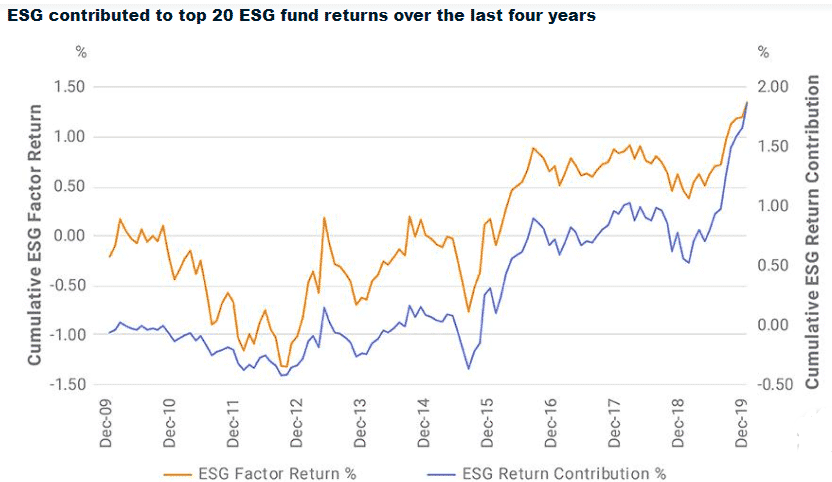

For ESG-focused investing, this means that even if returns are similar, the same return the investor can have in taking less risk. The charts below support this point.

Source: Bloomberg

The graph above reveals that investments with ESG equities offer better returns for the level of risk taken in most cases.

The chart below shows that the top 20 ESG funds enjoyed rising return contributions due to better ESG performance (ESG factor return).

Source: MSCI

Different reasons explain why is that so. Others say that businesses that embrace ESG standards tend to face lower costs of capital and have greater transparency.

While some believe that ESG reduces the risk as investors put their money in projects with a higher chance of success in the long run.

So traditional investors are now becoming more interested in ESG investing framework, too. And many had started using the ESG criterion on environmental aspects to favor investments that reduce carbon emissions.

Using ESG Funds to Reduce Carbon Emissions

ESG factors are a subset of non-financial performance indicators like managing carbon footprint. And this has been the case for many years since the bad effects of climate change were felt.

In fact, a manager of a global investment company wrote that:

“The big picture is that in the next few decades the global economy is going to transform to a low-carbon economy… And it will be one of the biggest investment events of our lifetime.”

A survey of hundreds of investors with over $700,000 confirmed such a claim. Most investors revealed interest in pumping their money into climate-related investments.

Indeed, projects that produce carbon credits are growing globally to cut down emissions. In fact, it’s now valued at over $850 billion and will grow to $22 trillion by 2050.

ESG investing and carbon credits both aim to align climate goals with sustainable investments. Carbon credits are tradeable permits given to companies to offset their GHG emissions. They’re a market-based mechanism for companies to cut their emissions.

In general, one credit equals one metric ton of allowed carbon dioxide emission.

Investing in carbon credits is a popular option for businesses to collectively fight climate change by slashing emissions.

As noted earlier, climate change and GHG emissions are ESG themes under the environmental aspect. But why use ESG funds to invest in carbon credits?

Here are some compelling reasons why:

Empower businesses and investors to address their climate impact

Put a price on carbon emitted into the air, which incentivizes firms and people alike to further reduce emissions

Enable companies to manage their carbon impact cost-effectively

Bring environmental and economic benefits to local communities where projects take place

Provide income stream for project developers by making emission reduction projects more viable

All these reasons are valid under the definition of ESG and its criteria. So no wonder why ESG-focused investors are lining up in climate-related projects that produce carbon credits.

Alphabet, Microsoft, and Salesforce collectively committed $500 million to a carbon removal program as members of the First Movers Coalition.

The three tech giants are a part of the First Movers Coalition, a technology coalition that aims to decarbonize industry and transport.

During the World Economic Forum in Davos, the coalition added carbon dioxide removal (CDR) to their programs.

The WEF partnered with the US Special Presidential Envoy for Climate John Kerry and over 50 global firms. These companies pledge to invest in innovative green technologies.

In particular, Alphabet, Microsoft, and Salesforce pledged to buy $500 million in carbon removal by 2030. Whereas Boston Consulting Group has promised to remove 100,000 tonnes of carbon by 2030.

Meanwhile, AES, Mitsui O.S.K. Lines, and Swiss Re have each committed to 50,000 tons (worth $25 million) of carbon removal.

The governments of India, Japan, Sweden, Denmark, Italy, Norway, Singapore, and Britain have also joined the group.

The First Movers Coalition Carbon Removal Program

Since its formation at COP26, First Movers brought together firms across carbon-intensive sectors. They range from big businesses that transport goods to renewable energy firms that use steel to build structures.

The coalition seeks to commercialize clean technologies using advanced purchase commitments for commodities. It provides a platform for various companies to make such commitments in this decade.

This then sends the strongest demand signal in history for technologies needed for reaching net zero emissions by 2050.

The coalition has committed to delivering impact in six major sectors by 2030:

These hard-to-abate sectors are responsible for about 30% of global emissions. And this figure can even rise to 50% of emissions by 2050 if the world won’t do anything about it.

This is where the First Movers Coalition comes in to do something about it.

Børge Brende, President of the World Economic Forum said:

“The coalition’s members are truly the ‘First Movers’ who are focused on scaling disruptive innovations that pave the way for long-term transformation… rather than the lower-hanging fruit of short-term process efficiency gains.”

The Coalition now has more than 50 members with a total market cap of $8.5 trillion (10% of the value of the Fortune 500). So far, it has committed around $10 billion already, or about 1% of its members’ value.

Under the First Movers’ carbon removal program, firms are making pledges to buy carbon removal, either by the ton or putting up certain sums of money.

The carbon removed must be verified and members must show that it can be stored for over 1,000 years.

Scaling Up Carbon Removal Technologies

According to the group’s press release:

“If enough global companies commit a certain percentage of their future purchasing to clean technologies in this decade, this will create a market tipping point that will speed up their affordability… It will also drive long-term, net-zero transformation across industrial value chains.”

John Kerry echoed the coalition’s point saying:

“The purchasing commitments made by the First Movers Coalition represent the highest-leverage climate action that companies can take… This is because creating the early markets to scale advanced technologies materially reduces the whole world’s emissions, not just any company’s own footprint.”

He further said that the addition of the First Movers carbon removal program will tackle the biggest challenge of the climate crisis.

That’s cutting the emissions from sectors where there’s no toolkit available yet to replace fossil fuels.

The latest IPCC report says that with very slow progress on emissions efforts, limiting warming to 1.5⁰C will now depend on carbon removal schemes.

First Movers CDR program is an effort to help abate rising temperature.

Through the Coalition, the tech giants work with many other private sector members. These include Mærsk, Amazon, Apple, Bank of America, FedEx, Ford Motor, Trafigura, Vattenfall, Volvo Group, Western Digital, and a lot more.

Other supporting partners include Breakthrough Catalyst, Carbon Direct, Frontier, and the South Pole.

Right now, a handful of startups are removing carbon from the atmosphere using various techniques. Paying these firms to do the job is currently quite pricey, costing hundreds of dollars per ton.

And that adds up fast when talking about a company that emits millions of tons of carbon each year into the air.

But Alphabet, Salesforce, and Microsoft’s early investments could help bring prices down by signaling there’s going to be a market for CDR.

Last April, the Frontier Group also made a similar but bigger commitment that Alphabet is also a part of. The scheme will be buying $925 million of carbon removal. Frontier includes other tech giants like Meta and Shopify as well as McKinsey.

Flowcarbon, a blockchain-enabled carbon credits trading firm, has raised $70 million.

Flowcarbon is an NYC-based climate tech company that operates at the intersection of carbon and crypto. Its main goal is to help speed up climate change solutions by tokenizing carbon credits. And by leveraging Web3, it aims to protect the earth’s natural carbon sinks.

The former WeWork CEO Adam Neumann co-founded the blockchain startup. Its first major funding round is for building market infrastructure in the voluntary carbon market (VCM).

The $70M funding consists of two parts.

The $32 million is from the funding round led by venture capital giant Andreessen Horowitz (a16z) – Other major contributors are Samsung Next and Invesco.

The other $38 million is from the firm’s sale of its “Goddess Nature Token” (GNT).

Flowcarbon’s Blockchain Technology for Carbon Credits

The climate tech firms will tap into the growing VCM to help companies offset their GHG emissions to fight against climate change.

In particular, the funding is for developing a protocol that tokenizes carbon credits. The aim is to drive investment in projects that remove carbon from the air.

Flowcarbon’s blockchain technology seeks to bring carbon credits on-chain. It will democratize access to offsets and incentivize high-impact climate change projects.

The current VCM is criticized for a couple of things. It’s fragmented, not transparent, hard to access, and there are doubts over the quality of some carbon credits.

Critics said that traders are converting older, lower-quality carbon credits into virtual assets.

And to help address the issues, Flowcarbon tokenized carbon credits through its two-way bridge, allowing credits to be on and off-chain.

By tokenizing credits, developers will gain cheaper financing earlier in their project’s life. It allows them to sell their credits forward to buyers who’ll enjoy more transparency.

Also, buyers from all backgrounds can join the Flowcarbon blockchain-backed market of carbon credits. The firm’s CEO, Dana Gibber said:

“Our mission is to provide the financing necessary to scale projects that reduce or remove carbon from the atmosphere… In particular nature-based projects.”

Nature-based projects may include reforestation, conservation, or nature restoration efforts.

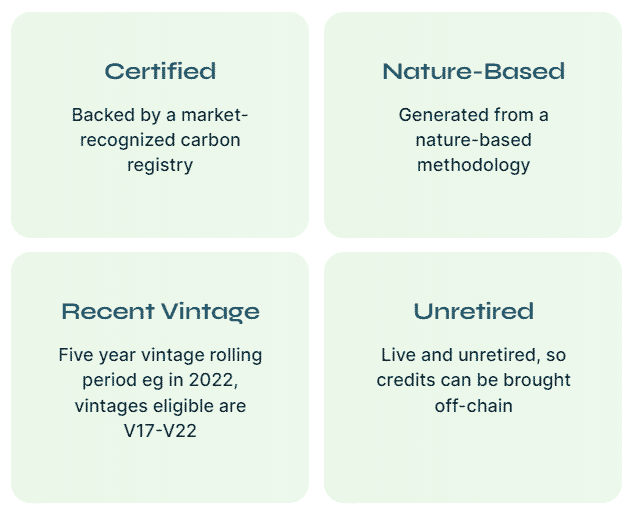

Flowcarbon’s Goddess Nature Token

The firm’s flagship token GNT is a bundle token. This means it’s fungible and can be retired, redeemed, or unwrapped. Each carbon credit in Flowcarbon’s GNT is:

Bundling credits can help in liquidity and will allow for greater trading volumes than in a traditional carbon trading platform. This reduces the trading risks.

Also, renowned registries pre-certify all carbon credits before they become tokens. They include Verra, Gold Standard, Climate Action Reserve, and the American Carbon Registry.

The bundling process of GNT also enables token holders to unwrap and remove a credit from the bundle. They can then choose to sell the unwrapped credit off-chain for physical delivery.

The analysts said that the more expensive nature-based credits will soon be all that is left. And they trade between 2 and 4 times the price of energy credits.

Lastly, a little 2% fee for Flowcarbon’s blockchain tech for carbon credits will help developers save money. The cost of selling credits via the traditional offtake agreement is around 30%.

Blockchain-enabled carbon credits by Flowcarbon are a part of a wider movement where other companies are also active. It joins other players in the carbon-to-crypto world.

IBM also worked with Veridium Labs four years ago on a carbon credit-related token.

Toucan, Regen, and Moss also aim to improve transparency and accessibility to the carbon credit market.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy