The nickel market experienced downward price pressure in 2024, but 2025 is expected to add more complexities. As demand for critical minerals intensifies and global processing capacity expands, major players in the nickel supply chain will face challenges in predicting prices.

Let’s explore what market research forecasts about the nickel this year.

Asia Powers Nickel Growth as Surplus Shrinks

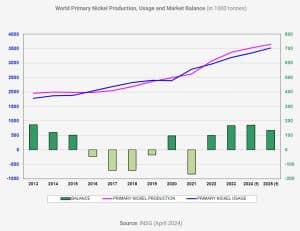

The International Nickel Study Group (INSG) updated its nickel market forecast explaining that the surplus will narrow to 135kt in 2025, with production increasing to 3.649 Mt and demand growing to 3.514Mt.

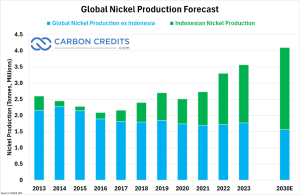

Narrowing down to Asia, nickel production is set to rise to 3.002Mt in 2025 where Indonesia and China will be the major contributors to growth.

- Indonesia: Production will rise from 1.600Mt in 2024 to 1.700Mt in 2025.

- China: Output is expected to grow from 1.035Mt in 2024 to 1.085Mt in 2025.

These increases highlight Asia’s dominance in global nickel production, with Indonesia and China continuing to strengthen their positions as key players.

However, 2025 presents an interesting twist! Recently, Bloomberg reported that Indonesia is considering cutting its nickel mine quotas by nearly 40% in 2025. According to Macquarie Group Ltd, the Indonesian government’s proposed restrictions on nickel mining could reduce global supply by more than a third, potentially driving up nickel prices.

These cuts are expected to lower production from 272 million tons in 2024 to just 150 million tons in 2025. Already, Indonesia’s mining limitations have caused supply strains, leading to record nickel ore imports from the Philippines, the world’s second-largest producer, in 2024.

Rising Demand and Nickel Deficits in 2025

Nickel is essential for battery production, especially in high-energy-density batteries used in electric vehicles (EVs). Yet, the market faces a growing imbalance. A recent Benchmark analysis explained the key trends and risks shaping the future of energy transition materials, focusing on nickel.

It highlights,

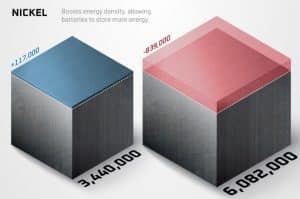

- By 2034, nickel is expected to face a deficit of 839,000 tonnes—nearly 7X larger than today’s surplus. This shows the urgent need to tackle supply shortages.

The report further explains that approximately $514 billion in investment is required (with $220 billion allocated to upstream projects) to meet global battery demand by 2030.

Of this, nickel alone needs $66 billion—the highest of all critical materials. Without these investments, sustaining the rapidly expanding EV market could become significantly challenging

Challenges in the Nickel Market

Benchmark further explained how the nickel market is grappling with slow project development. While gigafactories and processing plants can start operating within five years, mines often take 5 to 25 years to develop. This mismatch creates a “supply-demand disconnect” that threatens the EV supply chain.

Western nations are also trying to reduce reliance on China, which dominates refining and manufacturing due to lower costs and lenient environmental rules. Shifting production to Western countries, however, increases costs and requires stricter environmental compliance.

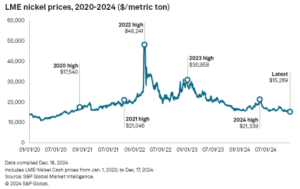

Furthermore, the nickel market had its own share of woes in recent years due to oversupply and weak demand. Nasdaq revealed, a brief price surge in early 2024 but it fell sharply by year-end. As 2025 rolled in, nickel traded between $15,000 and $15,200 per metric ton which analysts say to be the lowest since 2020.

- CHECK OUT: LIVE NICKEL PRICES

Closing the Supply-Demand Gap

Nickel’s role in the energy transition demands immediate investment in mining. Without sufficient raw materials, even the most advanced gigafactories won’t meet EV production goals. Addressing this resource clinch is crucial to stabilizing the supply chain.

Looking ahead, managing price risks, and ensuring steady nickel supplies will remain critical. Stakeholders must navigate these challenges while seizing opportunities in the evolving market for energy transition materials.

Amid the shifting nickel market, Alaska Energy Metals Corporation (AEMC) is leading efforts to boost U.S. nickel independence. Its flagship Nikolai project in Alaska contains valuable resources of nickel, copper, cobalt, and platinum group metals, all crucial for renewable energy and electric vehicles.

UK and Saudi Arabia Forge Critical Minerals Partnership

In the latest developments, Mining.com revealed that Britain will partner with Saudi Arabia to secure critical minerals like copper, lithium, and nickel which are all essential for EVs, AI systems, and clean energy technologies. The agreement aims to strengthen supply chains, attract investment, and create opportunities for British businesses.

Saudi Arabia, valuing its untapped mineral reserves at $2.5 trillion, seeks to position itself as a global hub for mineral trade. For the UK, this partnership supports its industrial strategy focused on economic growth, job creation, and national security.

The deal coincides with ongoing UK-Gulf Cooperation Council (GCC) free trade agreement negotiations. British Industry Minister Sarah Jones will lead a trade mission to the Future Minerals Forum in Riyadh, showcasing UK companies like Cornish Lithium and Beowulf Mining. Jones emphasized the importance of securing mineral supplies to advance AI, clean energy, and technological innovation in a competitive and uncertain global landscape.

As demand for nickel continues to rise, securing the necessary $66 billion in investments will be crucial for meeting the challenges ahead in 2025. However, the market’s future will depend on addressing supply gaps and adapting to shifting global dynamics.

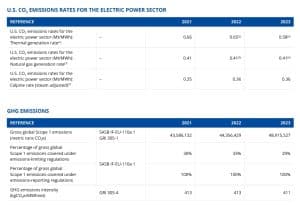

Source: Constellation

Source: Constellation Source: Calpine

Source: Calpine

source: NASDAQ

source: NASDAQ source: NASDAQ

source: NASDAQ source: NASDAQ

source: NASDAQ

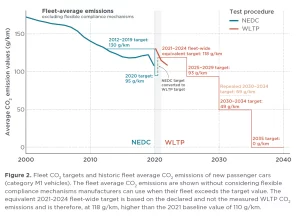

Source: ICCT

Source: ICCT Source: ICCT

Source: ICCT