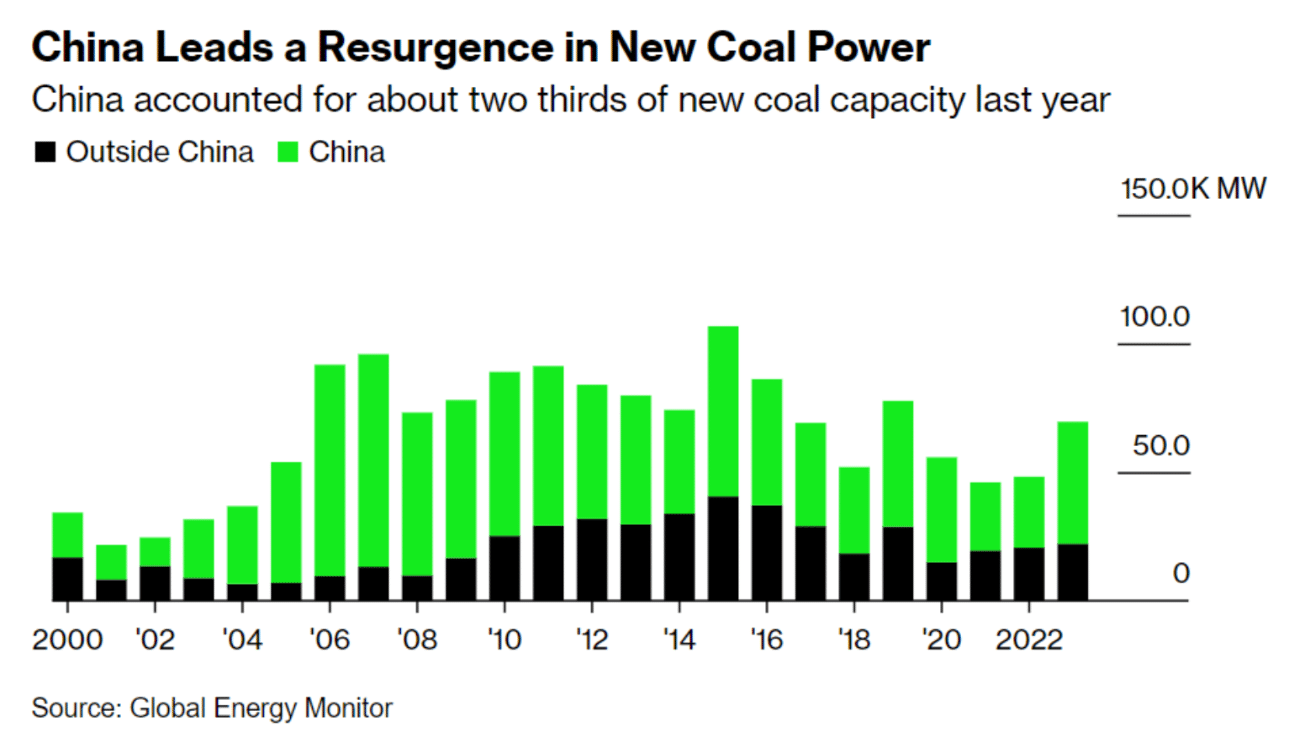

In a significant development for the global energy landscape, China has led a surge in coal-power capacity, driving the world’s total to a record high in 2020, according to a new report from Global Energy Monitor. This increase was primarily fueled by new plants in China, which accounted for about two-thirds of the expansion, with Indonesia and India following closely behind.

The Current State of Coal Consumption

The coal fleet expanded by 2% to 2,130 gigawatts, a remarkable increase driven by a decrease in retirements worldwide. This trend was particularly prominent in China, where the country initiated the construction of 70 gigawatts of new coal plants in 2020. That’s nearly 20x more than the rest of the world combined.

The report, titled “Global Coal Plant Tracker 2021: The World’s 1000 Largest Coal Plants,” highlights the significant role China plays in the global coal market.

The country’s aggressive expansion of coal-power capacity is a stark contrast to the trend of retiring coal plants in many developed countries, such as the United States and the European Union.

The increase in coal-power capacity has significant implications for global energy markets and climate policy initiatives.

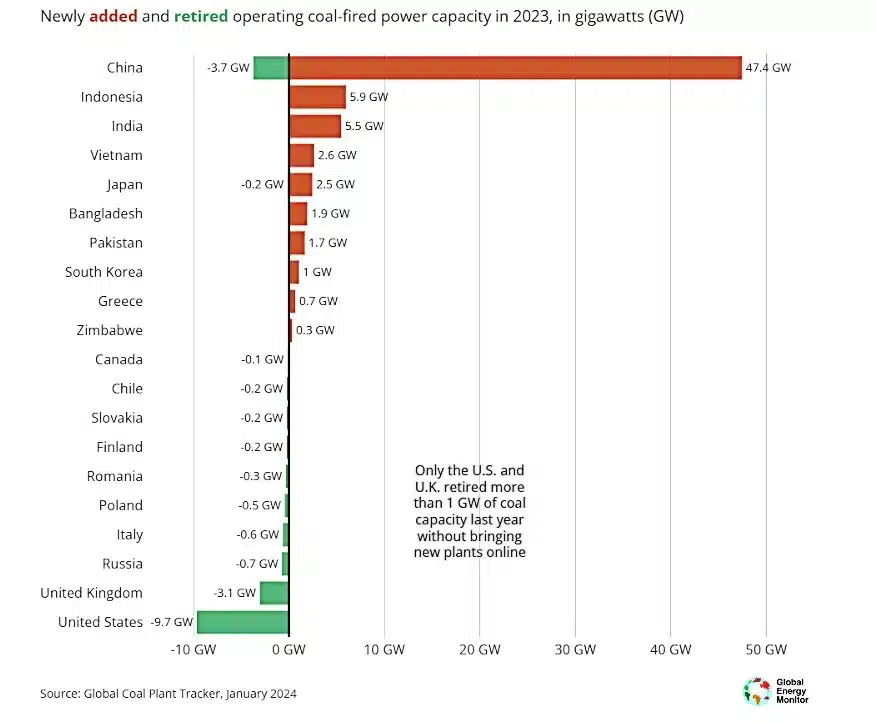

According to Global Energy Monitor, about as many countries opened new coal plant units as shut units down in 2023. Yet overall, more capacity is added than retired.

Here are 8 key points from the coal report:

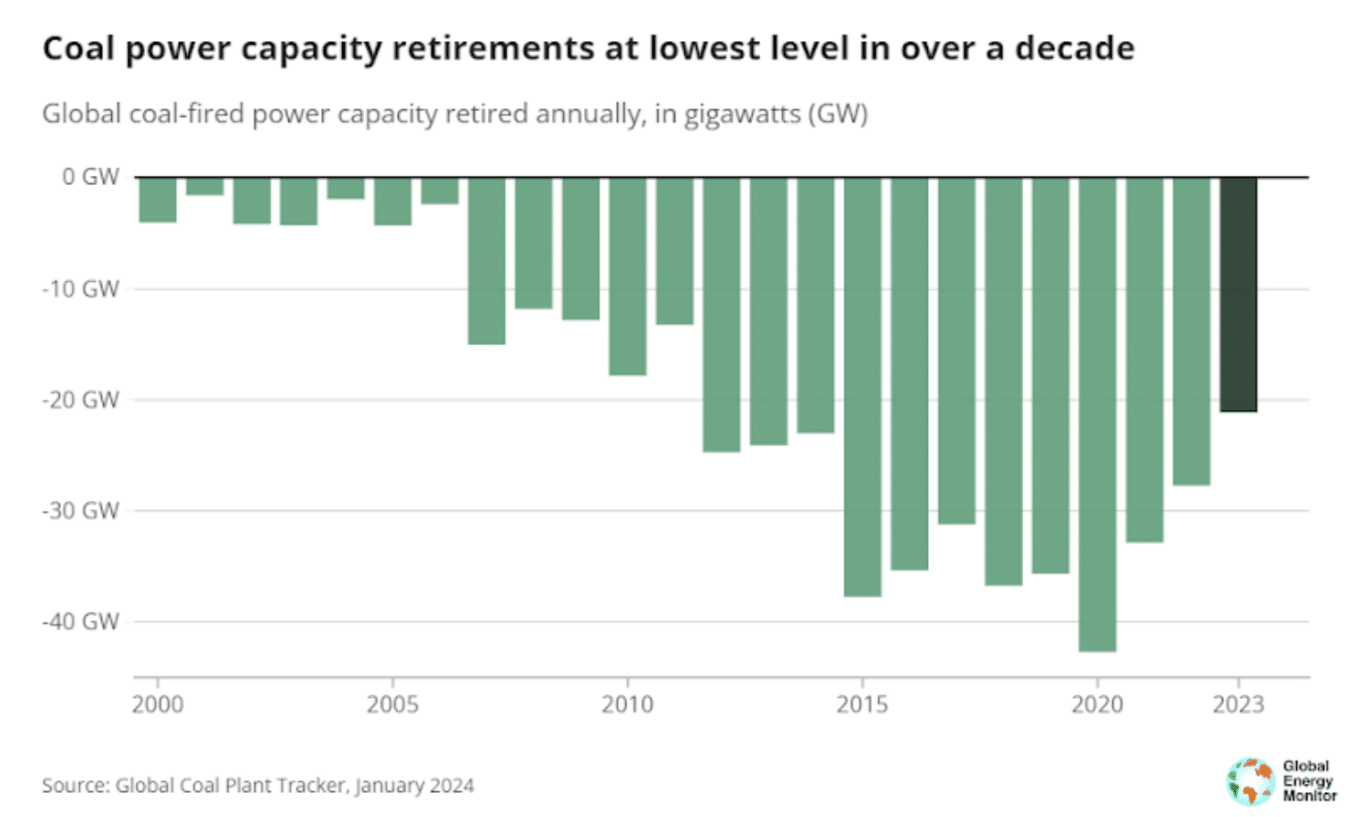

- Global operating coal capacity grew by 2% in 2023, with China driving two-thirds of new additions. However, this accelerated growth in coal capacity may be short-lived, as low retirement rates in 2023 that contributed to coal’s rise are expected to pick up speed in the U.S. and Europe, offsetting the blip.

- Heightened capacity additions will also be tempered if China takes immediate action to ensure it meets its target of shutting down 30 gigawatts (GW) of coal capacity by 2025. Countries with coal plants to retire need to do so more quickly, and countries with plans for new coal plants must ensure these are never built.

- Otherwise, meeting the goals of the Paris Agreement and reaping the benefits of a swift transition to clean energy will be difficult. Coal’s fortunes this year are an anomaly, as all signs point to reversing course from this accelerated expansion.

RELEVANT: Global Team Develops World’s First “Coal-to-Clean” Carbon Credit Program

- The data for the report comes from GEM’s Global Coal Plant Tracker, an online database updated biannually that identifies and maps every known coal-fired generating unit and every new unit proposed since January 1, 2010 (30 MW and larger). This data serves as a vital international reference point used by organizations including the IPCC, IEA, and the UN.

- According to the IEA, global coal demand is predicted to decline by 2.3% in 2026 compared to 2023 levels. And that’s even without stronger clean energy and climate policies. This decline is driven by the major expansion of renewable energy capacity coming online in the three years to 2026.

- More than half of the global renewable capacity expansion is set to occur in China, which currently accounts for over half of the world’s demand for coal. As a result, Chinese coal demand is expected to fall in 2024 and plateau through 2026.

- The shift in coal demand and production to Asia is accelerating, with China, India, and Southeast Asia set to account for three-quarters of global consumption in 2023, up from only about one-quarter in 1990. Consumption in Southeast Asia is expected to exceed that of the U.S. and the EU in 2023.

- The three largest coal producers globally – Indonesia, China, and India – are expected to break production records in 2023, pushing global output to a new high. However, to decrease emissions at a rate keeping with Paris Agreement goals, relentless coal use would need to fall much more quickly.

China’s Pivotal Role and the Shift in Coal’s Global Leadership

China’s growth in coal capacity highlights its focus on fulfilling energy needs for economic and industrial expansion, despite global efforts to cut greenhouse gas emissions. The interplay between increasing coal capacity and the shift toward cleaner energy will significantly influence the worldwide energy scenario.

The role of China and other key players in this process will be crucial in determining the pace and scope of the shift towards a more sustainable energy future.

The report further highlights a significant shift in global leadership regarding coal policies, particularly within the G7 and G20 nations. The G7 countries, which accounted for 23% of the world’s operating coal capacity in 2015, have reduced their share to 15% in 2023.

The reduction is underscored by the completion of new units in Japan. This marks the end of coal construction within the G7, although proposals still exist in Japan and the U.S.

Meanwhile, the G20 nations hold 92% of the world’s operating coal capacity, with Brazil, the current G20 chair, witnessing a decrease in pre-construction capacity, leaving only two projects remaining in Latin America.

This geographical shift in coal policies and projects underscores a broader global trend toward reducing reliance on coal. Moreover, it will have significant implications for international energy markets and climate policy initiatives.

Coal Plant Proposals and Retirements

The dynamics of coal plant proposals and retirements provide a nuanced view of the global coal industry’s future. In 2023, while 69.5 GW of coal power capacity was added, only 21.1 GW was retired, leading to a net increase in global coal capacity.

This trend is particularly pronounced outside of China, where new proposals totaled 20.9 GW, led by countries like India, Kazakhstan, and Indonesia.

Despite a general trend toward decommissioning, these developments indicate a complex global landscape where certain regions continue to explore new coal projects.

This ongoing activity suggests that while the global momentum is towards reducing coal dependency, achieving this goal requires concerted efforts across all nations, particularly those with significant new proposals.

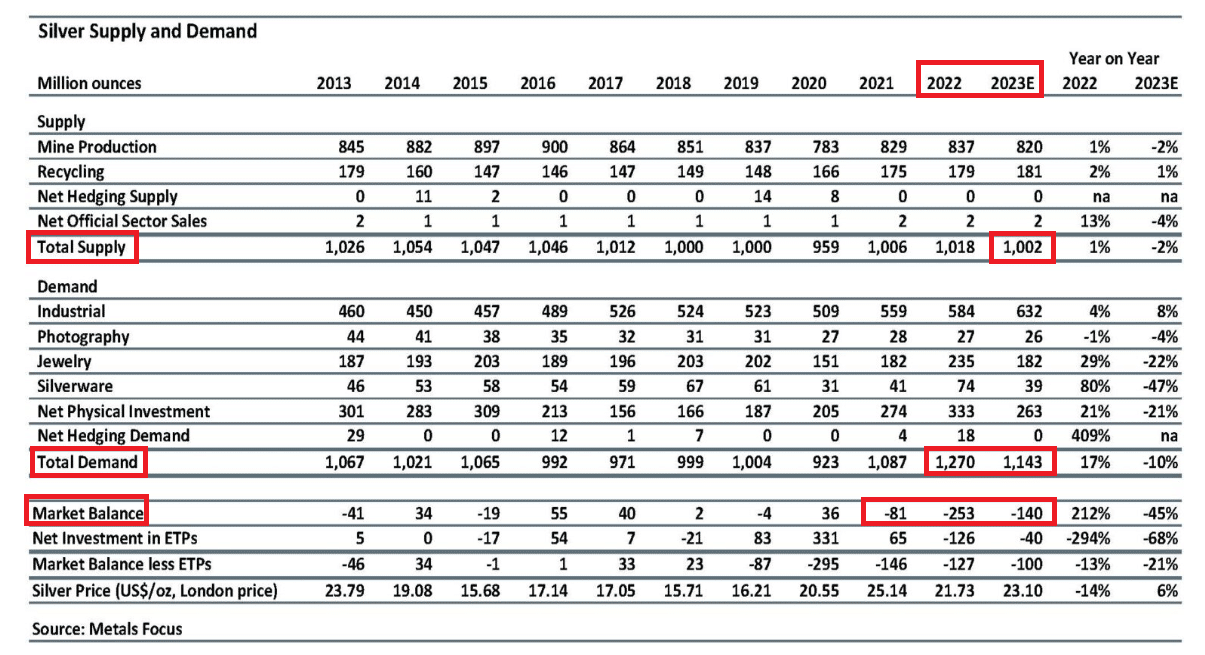

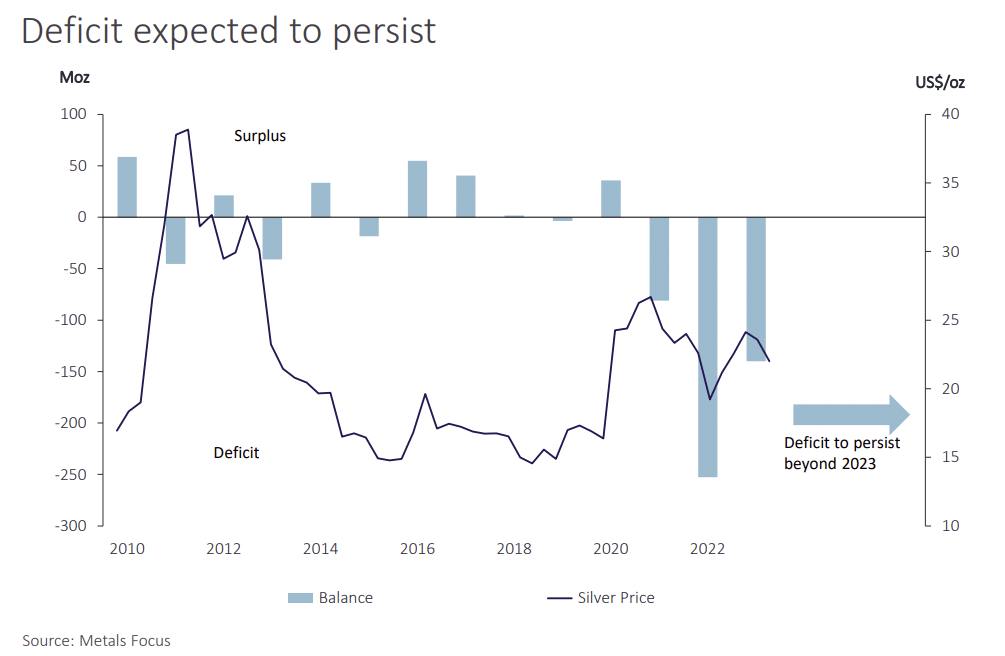

The forecast suggests that the imbalance between supply and demand in the silver market is not a short-term phenomenon but rather a structural issue that is likely to endure in the coming years. This underscores the ongoing importance of silver in various industrial applications and highlights the challenges in meeting the growing demand for this precious metal.

The forecast suggests that the imbalance between supply and demand in the silver market is not a short-term phenomenon but rather a structural issue that is likely to endure in the coming years. This underscores the ongoing importance of silver in various industrial applications and highlights the challenges in meeting the growing demand for this precious metal.