In 2023, most startup investments went down, but areas focusing on clean technology and sustainability didn’t face as much of a decline.

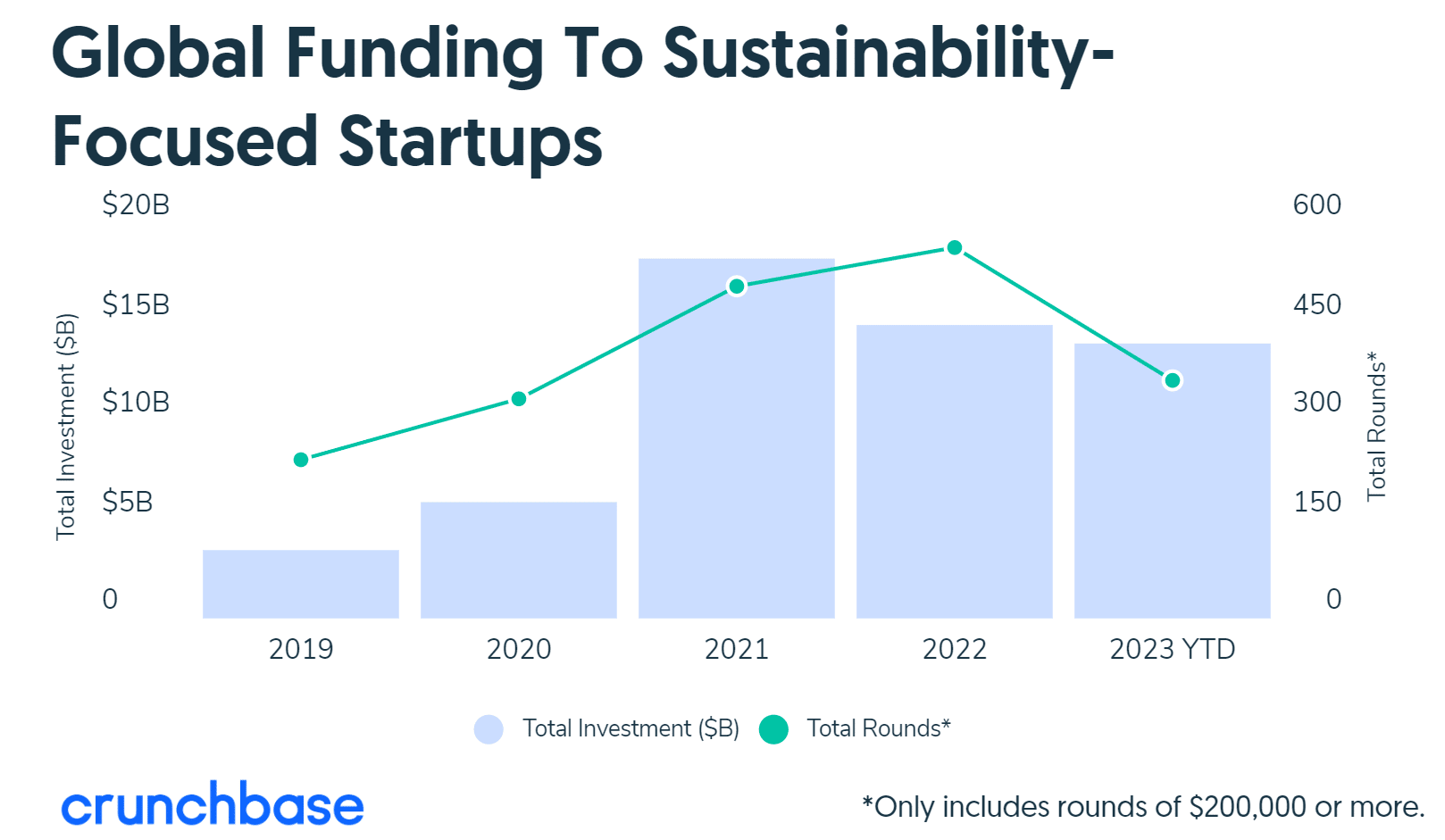

According to data from Crunchbase, around $13.9 billion was invested globally this year in companies working on things like recycling batteries and developing crops that conserve water. This investment amount is similar to what was seen last year.

Riding the Sustainability Investment Wave

Their analysis looks at the funding for global sustainability in 2023 compared to the past 4 years. The chart above shows the total amount of investments in billion dollars and total number of rounds (363).

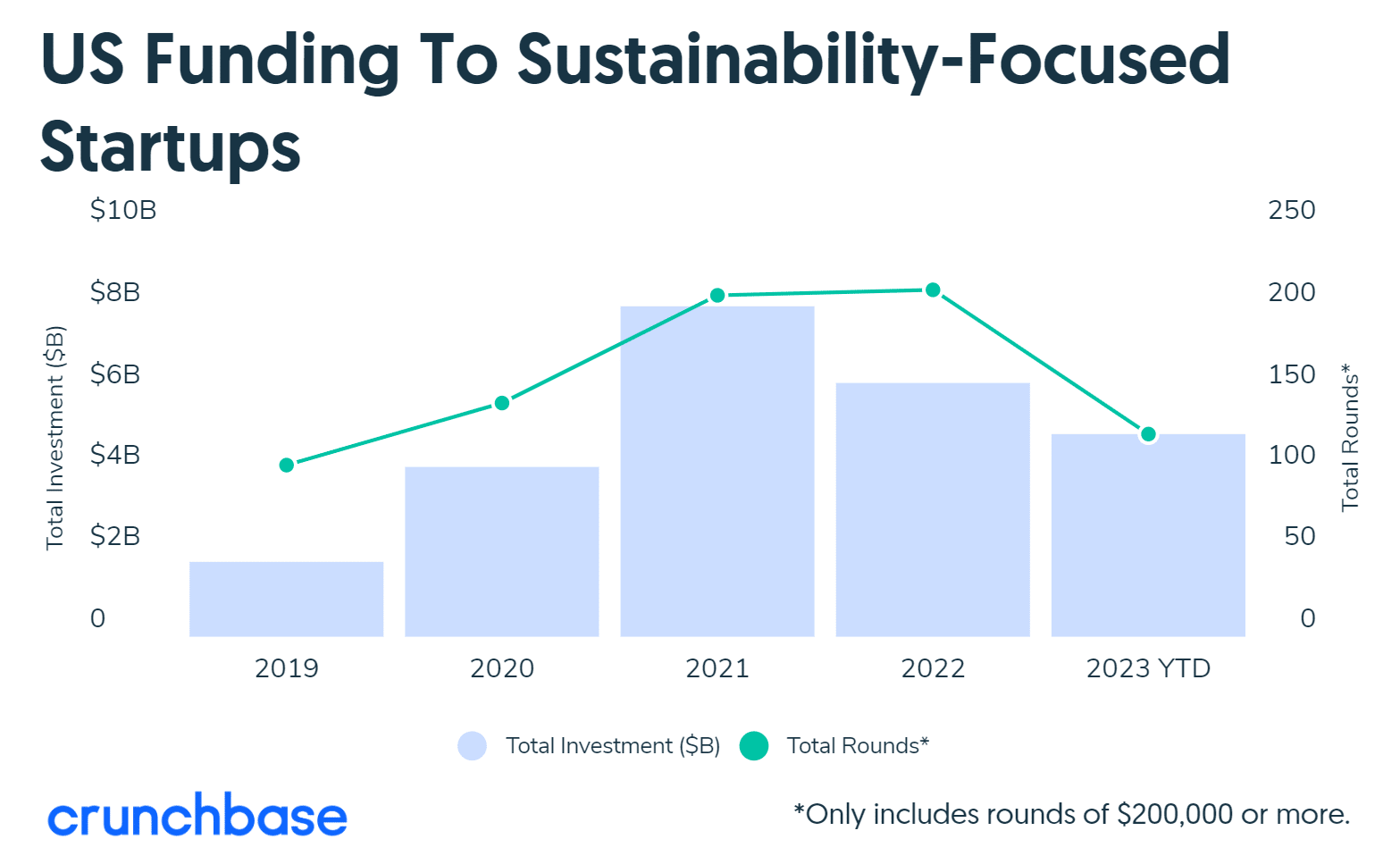

In the United States, funding specifically aimed at sustainability took a bigger step back this year, as shown below. However, investments in clean technology haven’t dropped as severely as in many other areas. And funds dedicated to this field are still actively supporting new projects.

The same trend was observed in VC funding for climate-tech startups specializing in carbon and emissions technology per PitchBook’s report. These companies received $7.6 billion in Q3 this year, exceeding the sector’s prior record by almost $2 billion.

Both funding trends defy the overall downward trend in fundraising.

Sectors That Got the Most Money

A lot of money this year went into supporting companies working on batteries. Specifically, companies in the battery space received the most significant amount of funding. Some of these companies even received $1 billion or more in financial support.

Several startups top the list with the most funding.

For instance, a French company focusing on making low-carbon batteries, Verkor, bagged over $2 billion through loans and investments. Another well-known company, Northvolt, producing lithium-ion batteries, raised over $1 billion via a convertible note. A battery recycling company based in Nevada, Redwood Materials, was able to attract $1 billion.

Apart from batteries, there’s also been a noticeable increase in interest towards capturing and storing carbon to combat climate change. This heightened investment is driven by alarming climate data suggesting severe consequences if atmospheric carbon levels continue to rise.

Numerous new companies aiming to remove and store CO₂ have received funding this year. Some of these startups are working on creating eco-friendly concrete to reduce the carbon emissions associated with its production. CarbonCure Technologies and C-Crete Technologies are popular examples.

Some companies are locking away CO₂ in soil and the oceans. Loam Bio and Charm Industrial, which both store carbon in soil, raised >$100 million each. Meanwhile, Ebb Carbon ($23M) and Captura ($12M) captured investors’ eyes with their innovative ocean-based removal technologies.

This surge in funding reflects the recognition that, despite the slow progress in adopting clean energy sources, there’s an urgent need for alternative solutions.

According to an IPCC report, strategies to limit global warming to 1.5°C often involve human-led efforts to remove carbon dioxide. And that’s despite the fact that these methods involve uncertain risks.

Alongside advancements in carbon capture, investments in climate-related software have continued. While there are fewer large-scale funding rounds exceeding $100 million compared to 2021 and 2022, there remains a steady flow of investments in software aimed at promoting sustainability.

In 2023, many of the most active investors in clean technology have become even more involved.

This is notable because a small group of investors focused on climate-related projects typically lead in terms of the number of deals they make and the total funding they provide. Familiar names in this sector, like Lowercarbon Capital, Temasek, TPG Rise Climate Fund, and Breakthrough Energy Ventures, have been particularly active.

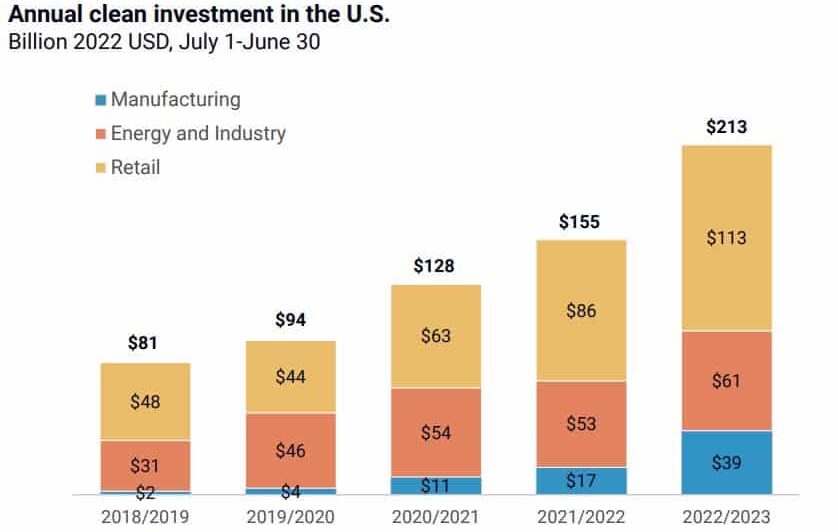

In the U.S. alone, a new database tracking the country’s decarbonization journey, Clean Investment Monitor, reported that a total of $213 billion was invested in clean technologies and infrastructure from July 2022 to June 2023.

It seems unlikely that these investors will reduce their involvement in the following year. This is because urgent climate change forecasts strongly drive their investments, and these forecasts are becoming increasingly alarming. While this isn’t a positive thing, it does serve as a strong motivator for continued investment in climate-related efforts.

As 2023 comes to an end, the Biden administration is highlighting the significant announcements made regarding clean energy manufacturing and clean power since President Joe Biden took office. These announcements have been supported by new laws focused on tackling climate change.

Despite the current high levels of oil production and strong exports of liquefied natural gas, the officials emphasize their commitment to reducing carbon emissions and transitioning away from fossil fuels.

An official particularly highlighted the need to globally shift towards cleaner energy sources. This is the agreement among nations that participated in the COP28 climate summit.

Unleashing the Power of Clean Energy

Since President Biden assumed office in January 2021, private companies have announced investments exceeding $500 billion in “21st century” industries such as semiconductors and electronics.

The figure includes about $360 billion invested in clean energy manufacturing, batteries, electric vehicles, among other sectors. Of this, around $132 billion is for new clean power projects, as stated in the official White House release.

Moreover, the forecasted total for clean power announcements this year, $58 billion, rose by 152% compared to 2021, $23 billion.

The Inflation Reduction Act (IRA) of 2022 largely spurred these investments. The regulation provides tax incentives for clean energy resources and electric vehicles over a decade.

In particular, clean energy manufacturing investments have jumped by over 170% in the past year because of these initiatives, according to the National Economic Council Director Lael Brainard.

The administration’s approach to investing in America’s clean energy future led to this significant surge in investments and job creation.

A separate report mirrored the same trend. Per data from the Clean Investment Monitor database, developed by Rhodium Group and MIT’s Center for Energy and Environmental Policy Research (CEEPR), clean energy is increasingly becoming one of the biggest industries in the U.S.

The CIM data reveals that from July 2022 to June 2023, clean investments amounted to $213 billion. Putting that in perspective, the figure is more than the annual GDPs of 18 U.S. states combined.

The database also found that retail got the most funding, with $113 billion where EVs received the biggest share. Specifically, ZEVs has the fastest growth, with an estimated $70 billion investment over the past year.

Since the IRA took effect in August 2022, there have been significant advancements in solar module manufacturing.

The White House presentation also reported announcements of >100 gigawatts (GW) of solar module manufacturing capacity. This capacity could potentially produce enough solar panels to power approximately 10% of homes in the country. The investment represents over $13 billion.

The growth trend extends to wind power production and related manufacturing. The combined onshore and offshore wind energy capacity is anticipated to reach 300 GW in 2030, marking a 43% rise from the EIA’s 2021 projection.

Since the IRA’s enactment, plans have been announced both for onshore wind and offshore wind projects. They include opening of new facilities, reopening of idle ones, or expansion of existing manufacturing facilities.

Same with other industry trends and reports, the White House also touted massive investments made in EV and battery production. The amount has reached a staggering $150 billion since 2021, with additional $39 billion for new energy storage projects.

It does make sense that ZEVs and batteries are getting the spotlight in clean energy investments. The IRA tax incentives promote the manufacture of EV batteries (48C) and clean energy storage (45X).

Apart from IRA, there are two other laws advancing investments in this emerging sector: Infrastructure Investment and Jobs Act 2021 and CHIPS and Science Act 2022.

The effectiveness of these climate-related policies in ramping up the transition to a clean economy will be crucial in achieving the country’s net zero goals. The nation aims to reduce carbon emissions by 50% to 52% below 2005 levels in 2030.

Paving the Way for Sustainable Growth

According to Brainard, the US is on track to reaching its 2030 emissions target.

Industry experts also believe that the legislation helps in scaling up the pace of clean investments in America.

While the current administration officials acknowledge challenges, they affirm their commitment to ensuring the certainty of IRA tax credits. Biden’s senior clean energy adviser, John Podesta, particularly said that:

“We’re obviously committed to ensuring that 10-year certainty [of IRA tax credits] comes through.”

Amidst a monumental year for clean energy investments and manufacturing advancements, the Biden administration underscores its commitment to transitioning the U.S. away from fossil fuels. With over $500 billion investments in clean energy sources, the nation is making substantial strides toward its climate goals.

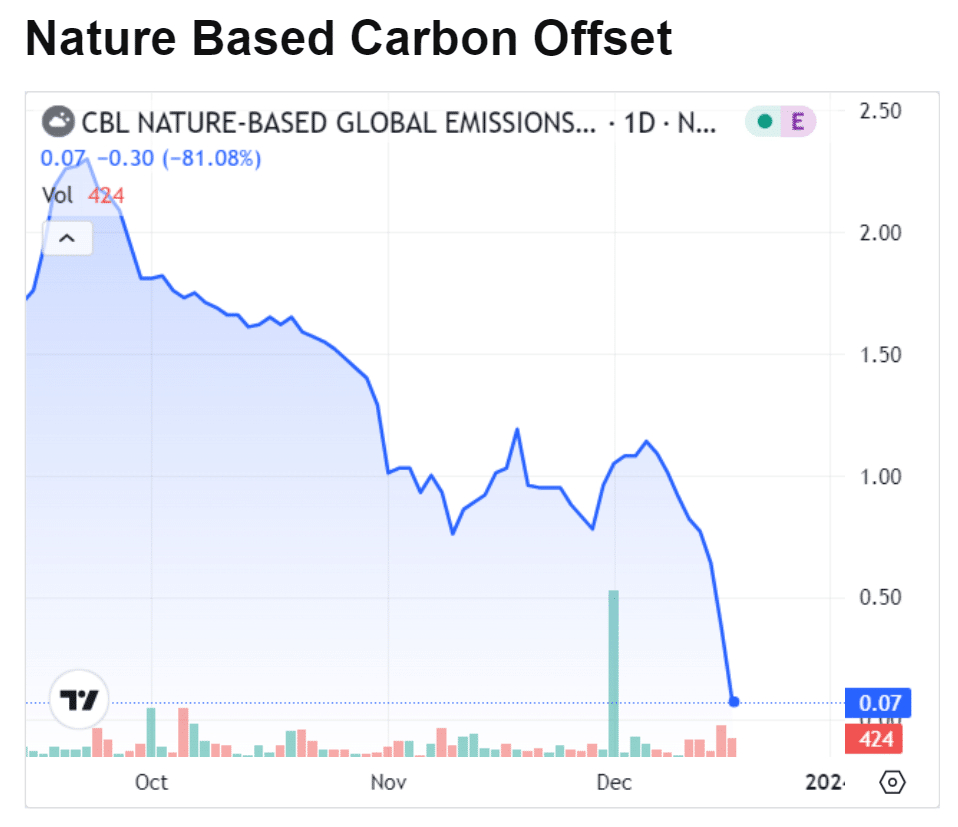

Voluntary carbon credits have faced a significant downturn in prices, casting the market under increased scrutiny. But compliance prices are set to soar, with Germany raising it to 50 euros while Canada also plans to increase in 2024.

Expectations were high that the recent COP28 conference would address concerns on carbon credit reliability by establishing regulatory measures. Yet, the attempt fell short, leading to carbon prices dropping to their lowest levels, particularly Nature Based Carbon Offsets (NGEO).

The Meltdown of NGEO Carbon Prices

Amid rising commitments to reach net zero emissions, companies have been purchasing carbon credits to offset their emissions. However, the market is currently experiencing a breakdown.

NGEO prices plummeted to a massive 81% in trading to its lowest level ever, at just $0.07.

Over the last 2 years, there has been a drastic drop in demand for credits, causing a sharp decline in prices.

The diminishing demand is attributed to the absence of standardized regulations governing carbon markets. Recent news and studies have raised concerns about the reliability of the system, emphasizing the lack of rules.

Carbon markets essentially enable the offsetting of carbon emissions through tradable entities – carbon credits. Each credit represents the removal or reduction of carbon dioxide from the atmosphere, achieved through actions like tree planting.

There are two types of carbon markets: mandatory and voluntary.

Mandatory or compliance markets are regulated by governments or international bodies using instruments like carbon taxes to regulate energy-intensive industries. On the other hand, voluntary markets allow companies and individuals to trade credits without compulsion. It is this voluntary sector that is currently under scrutiny.

Compliance Prices Set to Surge

Things in the compliance sector are taking a different turn. Germany, in particular, recently approved their aim to increase carbon prices by more than previously planned.

The country voted to raise a carbon levy on fossil fuels used in housing and transportation. The German government initially agreed to raise prices to 40 euros a ton in 2024. But the price is now set to reach 45 euros beginning next month, a 50% jump from its current price.

That figure will further rise to 50 euros in 2025. This new carbon price is part of the German’s nation deal to mitigate a budget crisis. It will also help fund Germany’s climate and transformation fund.

Over in Canada, the federal government also decided to bring up the carbon tax from $65 per tonne this 2023 to $75 in 2024.

Canada’s carbon price jumped by the most this year, going from $50 to $65 a tonne of carbon emissions. And this will continue at the rate of $10 a year increase until it reaches $170 per tonne in 2030.

A BloombergNEF report projected that the total value of carbon credits issued and sold for companies to achieve their decarbonization goals could reach $1 trillion by 2037. Under stricter supervision, where companies can only purchase vetted carbon credits, offset prices could surge to over $250 a ton.

Some key players cautioned about the voluntary market’s reliance on bilateral transactions for inexpensive credits, which may jeopardize its future.

They stressed the need for transparency, clear quality definitions, and easier access to high-quality supply, warning that upcoming years could mirror the challenges seen in 2022.

Hopes were pinned on a resolution in this regard during the COP28 conference. The climate summit was intended to address the issue, yet it proved unsuccessful.

The Paris Agreement’s Article 6, outlining rules for carbon trading, was anticipated to provide a solution. But countries failed to adopt these standards at the recent COP28 conference in Dubai.

As compliance prices set to surge in the near term, voluntary carbon credits, particularly the NGEO, face a crisis due to plummeting prices and lacking regulations. The COP28 conference failed to provide resolutions, leaving uncertainties around market reliability. Hopes are now betted on clearer regulations and greater transparency to stabilize these crucial markets amid mounting climate commitments.

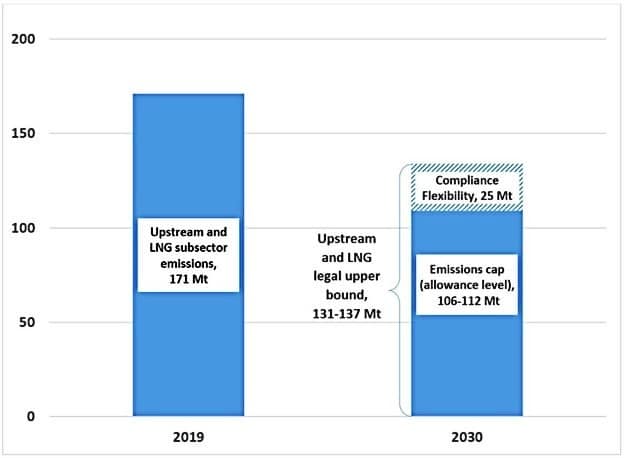

The Canadian government has introduced a new rule to limit greenhouse gas emissions from the country’s oil and gas companies. Federal ministers aim to cap emissions between 35% to 38% of the levels seen in 2019 by the year 2030.

According to Environment and Climate Change Canada (ECCC), this draft regulation will likely allow emissions totaling around 106 to 112 megatons of carbon dioxide equivalent (CO2e).

During the COP28 webcast in Dubai, Environment Minister Steven Guilbeault highlighted that the sector is the biggest emitter in Canada. He emphasized that while emissions in other sectors are decreasing, the oil and gas sector continues to pollute more.

Few days ago, Canada also revealed new regulations seeking to reduce methane emissions from the oil and gas sector. It aims to cut at least 75% methane emissions over 2012 levels by 2030, which will be a crucial part of the entire cap.

Methane is responsible for about 30% of the oil and gas sector’s total GHG emissions.

Estimated and projected oil and gas sector emissions (Mt CO2e) in 2019 and 2030

Source: Canada.ca

Canada’s Emission Cap: Oil & Gas Balancing Act

The draft framework aims to reduce emissions while keeping Canada competitive in the world market. It sets a limit on the amount of pollution the oil and gas industry can make.

However, the rule doesn’t restrict how much the oil and gas companies produce. It was created after discussing with industry, Indigenous groups, provinces, territories, and others.

It also allows some flexibility, letting the sector emit up to about 20% to 23% below 2019 levels. This cap will help Canada cut emissions and move towards net zero by 2050.

Canada’s greenhouse gas emissions in 2020 reached 672 megatons of CO2e, as per federal data. Of this, the oil and gas sector contributed 178 megatons of CO2e, making up 26% of the total emissions. Transportation followed closely, accounting for 159 megatons or 25% of the emissions.

The said sector, responsible for 28% of Canada’s pollution in 2021, emitted 201 million metric tons in 2019. That’s 20% higher than 2005.

Minister Guilbeault emphasized the need for immediate actions to meet the collective goal of achieving carbon neutrality by 2050. He also noted that:

“We look forward to industry talks to get this draft framework right. This is a challenge of our time and also a great opportunity.”

The federal government is also considering implementing a national cap-and-trade system to limit GHG emissions further. Proposed regulations will also establish reporting and verification processes, with a gradual phase-in of the planned system from 2026 to 2030.

Interested parties, including the industry and stakeholders, have until February 5, 2024, to submit comments and input regarding the draft. The finalized regulations are anticipated to be issued by early 2025.

Federal Natural Resources Minister Jonathan Wilkinson highlighted the importance of considering the competitiveness of oil and gas producers in Alberta, British Columbia, Saskatchewan, and Newfoundland and Labrador.

However, specific details regarding this aspect’s role in shaping the regulations were not elaborated upon during the webcast.

Controversy and Opposition Surrounding the Cap

The draft allows companies to buy and trade a certain number of emissions allowances, also called carbon offset credits. They can either buy carbon offsets or contribute to a fund that reduces emissions.

While the draft regulations aim for reducing harmful emissions from the most polluting sector, opposition abound.

The Canadian Association of Energy Contractors opposes the move, fearing it will negatively impact workers and small to medium-sized businesses. The association’s leader, expressed concerns about higher energy costs and job losses due to the cap.

Similarly, Alberta Premier Danielle Smith criticized the federal government, calling the emissions cap an “intentional attack on Alberta’s economy”. She had invoked an act allowing the province to override federal clean-electricity regulations in opposition.

The Alberta government issued a regulation in 2016 that puts a cap of 100 million MT for the province’s oil sands producers. At present, Alberta’s total GHG emissions stand at about 70 million MT, according to information on the provincial government website.

For another director, the cap on Canada’s GHG emissions will affect junior producers with <20,000 b/d output. They’ll be casted.

The cap-and-trade system will regulate direct GHG emissions, including those indirectly related to oil and gas production and carbon storage. Thus, it would cover various facilities such as offshore operations and LNG plants.

The Environment Minister stressed that companies making substantial profits should invest in Canadian jobs and communities. However, no new government funding was announced, despite Canada’s previous pledge of $9.1 billion in tax credits for carbon capture systems.

Canada’s proposed regulations to cap emissions in the oil and gas sector mark a pivotal step toward addressing climate change. The draft rule intends to reduce pollution without hampering production. Despite debates and concerns from industry leaders about potential economic impacts, the government is emphasizing the urgency of climate action and inviting feedback until early 2024.

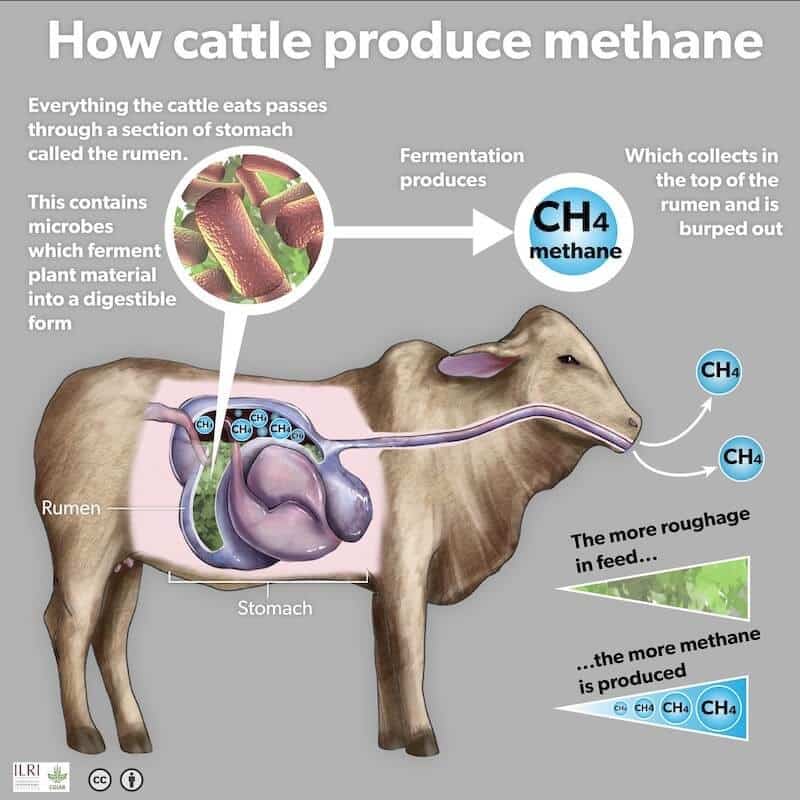

The Canadian government is taking steps to greenhouse gas emissions, especially from cows’ burps, a significant source of methane. Environment and Climate Change Canada (ECCC) is proposing incentives for beef cattle farmers to lower methane emissions by improving diets and management practices.

This initiative encourages changes in cattle diets, feed efficiency improvements, and strategies that minimize methane release.

The Farmers’ Battle: Cutting Cow Burps

Government spokesperson Oliver Anderson highlighted the aim to reward farmers using feed additives to diminish cow-produced methane. He noted farmers’ previous contributions in lowering methane per unit of milk through improved livestock genetics.

The proposed eligible activities include altering cattle diets, adding specific ingredients to boost animal performance, and employing growth promoters. Tim McAllister from Agriculture and Agri-Food Canada suggested that modifying cattle diets, like adding grain and oil, could help cut methane emissions while improving feed efficiency for meat production.

ECCC Minister, Steven Guilbeault, also noted farmers have been the champions of climate action through sustainable agricultural practices. He further added that:

“This [draft protocol] is an opportunity for farmers to implement practical solutions to reduce agricultural methane emissions, generate revenue, and harvest a greener future for all.”

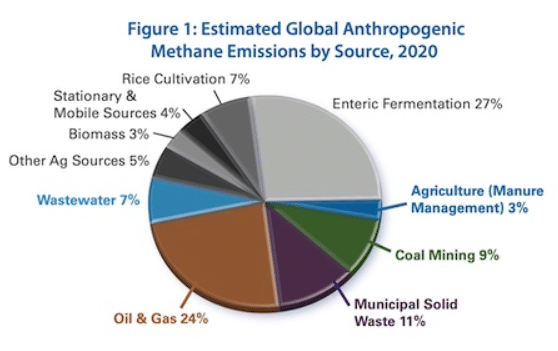

In 2021, agriculture accounted for 31% of Canada’s total methane emissions, primarily from enteric fermentation in beef and dairy cattle. Enteric fermentation is a digestive process that generates methane. Methane is released when cows burp as part of their natural digestion.

According to the American Society for Microbiology, enteric fermentation is responsible for 27% of global methane emissions in 2020.

Source: asm.org

The Math Behind Cows’ Methane Emissions

Cows, through the process of digestion, contribute significantly to methane emissions.

Image source: American Society for Microbiology

According to research, an average amount of methane produced by 2 cows a year is 504 pounds. In comparison, one car emits around 11,500 pounds of carbon dioxide.

To put that in context, methane is 28x more potent than CO2 at trapping heat in the atmosphere. That means, each year, two cows release as much GHG as one car driven 10,000 miles.

In Canada, it accounts for about 45% of total agricultural emissions.

Methane, responsible for around 13% of the country’s overall GHG emissions in 2021, primarily comes from three sources:

Oil and gas (38%),

Agriculture (30%), and

Waste or landfills (28%).

The majority (96%) of methane emissions from enteric fermentation come from cattle. While various animals can release methane through digestion, cattle are the primary source in the country.

The Canadian government further aims to reduce nitrous oxide emissions, another GHG originating from manure or animal feed.

To address methane emissions, the REME proposes incentives for farmers to adjust cattle diets, manage feed consumption, and reduce emissions.

These measures will be further refined based on stakeholders feedback before a final version is released in the coming summer. Agricultural practices will be adjusted to balance nutrient needs while minimizing the cost of implementing changes.

Additionally, Canada is targeting methane reductions in the oil and gas sector, aiming for a 75% reduction according to a newly released draft plan by the ECCC.

These regulations aim to reduce emissions by 217 megatonnes (CO2 equivalent) from 2027-2040. This would result in social and economic benefits totaling $12.4 billion from avoided global damages.

REME: Canada’s Emission Reduction Plan

The Government of Canada developed the REME protocol in collaboration with agricultural experts. Their goal is to ensure it offers practical ways for farmers to earn revenue through emissions reductions.

REME is ECCC’s draft fourth protocol under Canada’s Greenhouse Gas (GHG) Offset Credit System. The system encourages project developers to create innovative projects that reduce GHGs compared to business-as-usual practices.

Proponents of offset projects can produce carbon credits if their projects meet the requirements of the Canadian GHG Offset Credit System Regulations and an applicable federal offset protocol.

The REME protocol draws on input from technical experts and incorporates best practices from provinces like Alberta. It is also part of Canada’s comprehensive efforts to decarbonize the agricultural sector.

For instance, the Agriculture and Agri-Food Canada announced investment of $12 million in the Agricultural Methane Reduction Challenge. This funding aims to support innovators in developing cost-effective and scalable solutions to reduce enteric methane emissions from cattle.

Canada is steering towards a greener agricultural future by addressing methane emissions from beef cattle. The REME initiative reflects the government’s commitment to incentivize emissions reductions and empower farmers in mitigating climate change. Through these innovations, the country aims to provide sustainable solutions while aligning with global climate goals.

In the realm of clean energy, uranium-powered nuclear plants often take a back seat to solar and wind, yet they stand as the second-largest low-carbon electricity source globally. Nuclear energy operates emission-free, mitigating carbon dioxide and curbing harmful air pollutants. It’s not just an alternative; it is pivotal to global clean, sustainable energy transition – the key for net zero emissions.

In this article, we’ll explore the uniqueness and the driving forces behind the resurging interest in nuclear energy. This means delving into the uranium sector, an emerging bullish market and why it’s crucial for a net zero world.

Moving Away From Coal With Nuclear Energy

Transitioning from coal to cleaner energy sources is a pivotal step in addressing climate change.

For centuries, coal was the cornerstone of the industrial revolution, but its combustion accounts for over 40% of global carbon emissions. It’s also responsible for 75% of electricity generation emissions in 2019, as per the International Energy Agency (IEA)’s data.

To align with the Paris Agreement’s objectives of curbing global warming below 1.5°C, phasing out coal is imperative.

The shift toward clean energy involves pivoting from high-emission sources to low-carbon alternatives to mitigate climate impacts. This energy transition aims to eliminate reliance on fossil fuels, amplifying renewable options such as hydro, solar, wind, and nuclear power.

An excellent example of this transition is Ontario, which has been coal-free since 2014, primarily harnessing nuclear and hydro energy to power its grid sustainably.

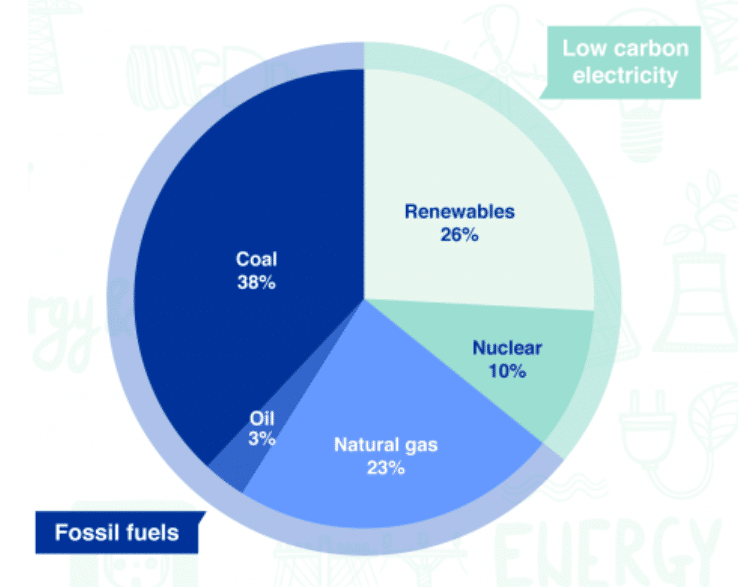

Both coal and nuclear power plants operate using steam-driven turbines to generate electricity. Despite coal accounting for roughly ⅓ of global electricity generation, nuclear energy stands out for its capability to provide consistent baseload power, effectively supplementing intermittent renewable sources like solar and wind.

World Total Electricity Production by Energy Source

Source: International Atomic Energy Agency

Back in 2003, Ontario pledged to phase out a quarter of its electricity generation by decommissioning nearly 9000 MW of coal capacity. To achieve this, the province refurbished nuclear units and integrated a mix of renewables and natural gas. Doing so allowed the Canadian province to successfully attain over 90% carbon-free electricity.

It’s a testament to the feasibility of transitioning away from coal toward cleaner, more sustainable energy sources like nuclear.

The adaptability of nuclear power plants in adjusting output according to demand and the availability of other energy sources adds resilience and stability to the grid, particularly in supporting variable renewables.

The recent report by the United States’ Department of Energy on nuclear power highlighted the potential to convert over 250 GW of coal capacity in the U.S. into nuclear power, effectively doubling the existing nuclear capacity.

Moreover, the DOE’s analysis revealed various benefits for communities near the coal plants considering such a transition. This includes the creation of 650 jobs, generating $275 million in economic activity, and an 86% reduction in GHG emissions.

Deputy secretary, Andrew Griffith, noted that the expertise and skills learned from operating coal plants could be adapted to nuclear power. He further underlined that this potential extends beyond just integrating into the electricity grid, as some reactor concepts can also offer applications in industrial heat.

The agency also emphasized the multi-dimensional benefits that nuclear power could offer for the energy transition.

Nuclear as Clean and Sustainable Energy Source

When the term “clean energy” is mentioned, most individuals tend to immediately think of solar panels or wind turbines. However, nuclear energy, often overlooked in these discussions, stands as the second-largest source of low-carbon electricity globally, trailing only hydropower.

To understand the cleanliness and sustainability of nuclear energy, consider these three key points:

Zero Emissions and Air Quality Protection:

Nuclear energy is a zero-emission clean energy source. It operates via fission, splitting uranium atoms to generate energy. The resulting heat drives turbines for electricity production without emitting harmful byproducts present in fossil fuels.

In 2020, the United States avoided over 471 million metric tons of carbon dioxide emissions through nuclear energy, surpassing the collective impact of all other clean energy sources combined.

Small Land Footprint:

Despite generating substantial carbon-free power, nuclear energy requires minimal land compared to other clean sources. A standard 1,000-megawatt nuclear facility in the U.S. operates on slightly over 1 square mile.

In comparison, wind farms require 360x more land area, while solar plants demand 75x more space to produce equivalent electricity. In other words, millions of solar panels or hundreds of wind turbines are needed to match the power output of a typical nuclear reactor.

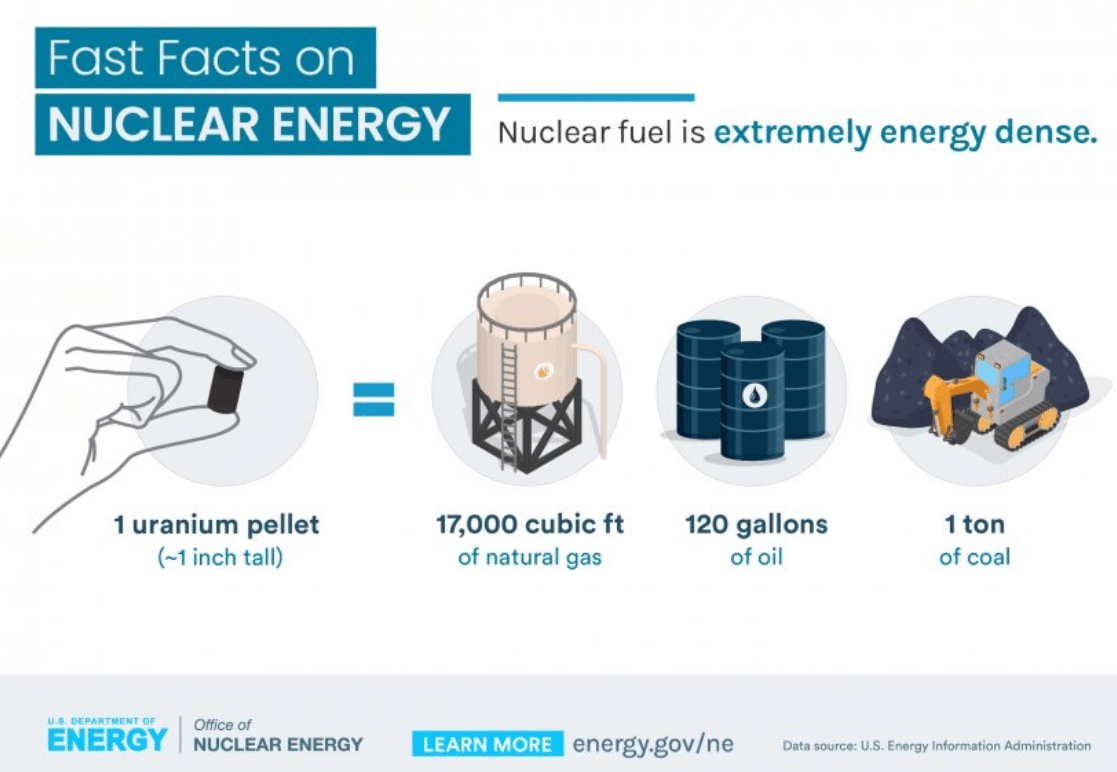

Extremely High Energy Density with Minimal Waste:

Nuclear fuel boasts an incredibly high energy density, nearly 1 million times greater than traditional energy sources. Consequently, the volume of used nuclear fuel isn’t as extensive as commonly believed.

Putting that in perspective: all the used nuclear fuel produced by the U.S. nuclear energy sector over 6 decades could fit within the dimensions of a football field at a depth of less than 10 yards.

This waste can potentially be reprocessed and recycled, although this isn’t currently practiced in the U.S. However, emerging advanced reactor designs aim to operate on used fuel, offering promising solutions.

Consider the following facts. They underscore the significance of nuclear energy in the realm of clean and sustainable power generation.

Source: https://www.energy.gov/

Uranium Bull Market is Emerging

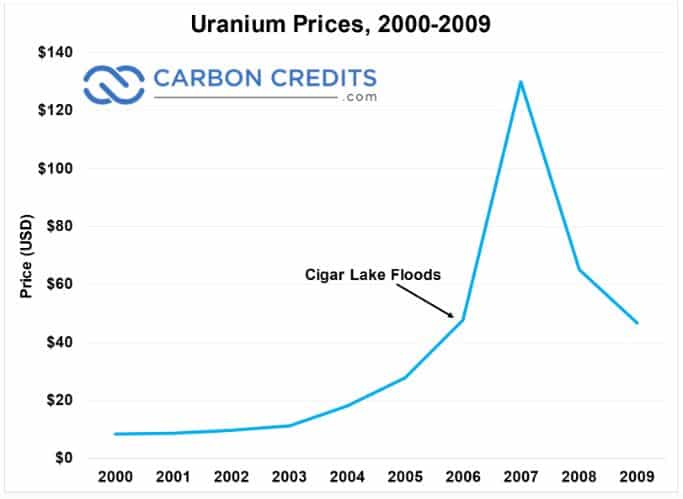

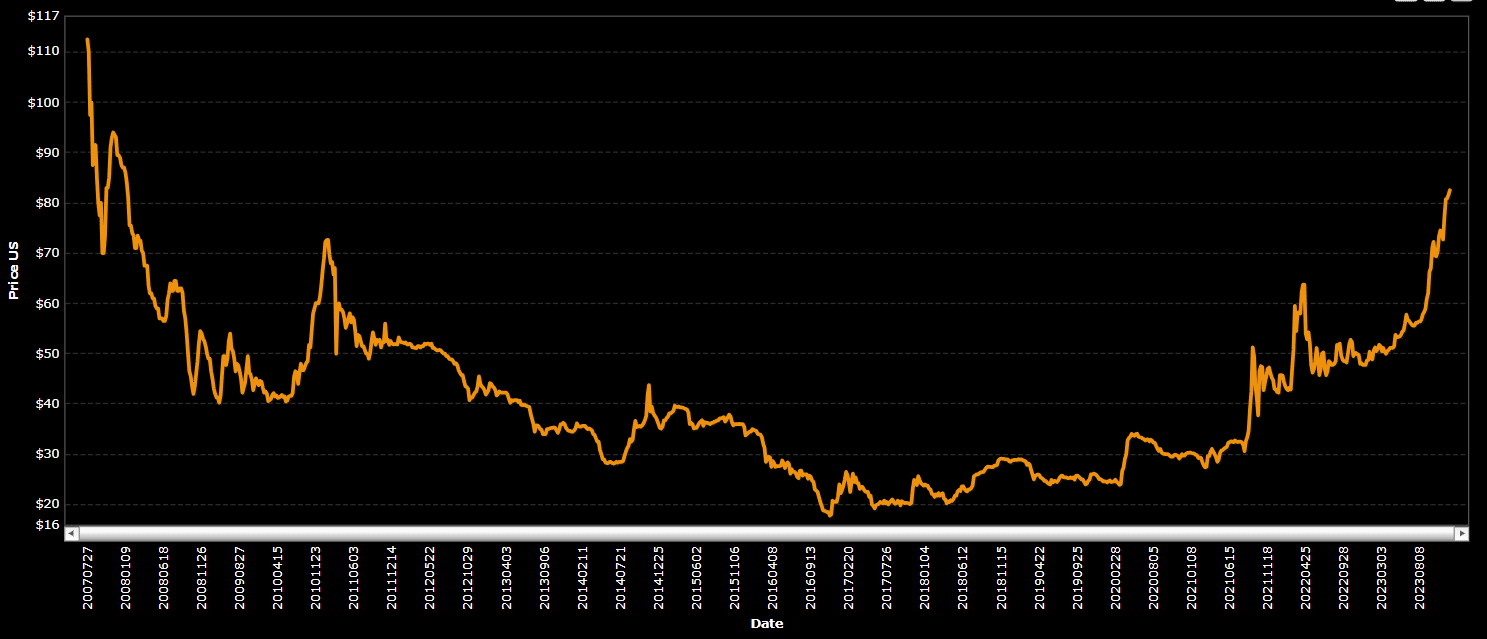

Delving into the current market scenario, it helps to consider the historical context of the past decades.

Going back to the ‘60s and ‘70s, these were the pivotal periods when nuclear power stations were extensively built. These years marked the initial rise in demand coinciding with the emergency of nuclear technology.

Unfortunately, a series of accidents, Three Mile Island and Chernobyl, led to nuclear downturn that put many projects on hold. This downturn persisted for about two decades.

Fast forward to the early 2000s, the climate change challenges start to kick in, particularly the increasing greenhouse gas emissions. This moment was dubbed the Renaissance of nuclear energy when new projects were revealed. Consequently, this resulted in a spike in 2007 as shown in the chart.

Then there has been a gradual but consistent uptick in uranium prices since 2019. Notably, this trend showed investors’ interest resurging due to the perceived potential in uranium investments. And a few days ago, uranium spot prices hit a 15-year high at $85 per pound.

Analysts even forecast more increases in prices, confirming that a uranium bull market is approaching, if it hasn’t come already. This makes GoldMining Inc (GLDG)’s uranium project even more valuable. As one of the companies making waves in the uranium market, GoldMining Inc brings exposure to one of the most exciting uranium exploration regions in the world.

How Does Uranium Help Achieve Net Zero Emission?

Uranium plays a significant role in the quest for achieving “net zero emissions“. It boasts a feature lacking in some renewable energy sources – capacity to provide reliable baseload energy production.

While solar, renewables, and hydroelectric power receive continued investment due to their eco-friendliness, they face challenges in delivering consistent energy output. For instance, solar energy is inactive at night, and wind turbines remain idle when there’s no wind. Recent occurrences, such as lower wind speeds in the United Kingdom resulting in decreased turbine energy production, have forced a shift to natural gas.

Although natural gas is a cleaner energy source compared to coal or oil, its carbon footprint remains notably higher. Surprisingly, a substantial portion of the world still heavily relies on coal for electricity generation.

In the United States, for instance, 19% of energy production persists from coal. Even in China, despite significant strides in reducing reliance on coal from 70% to 57% over a decade, there’s a fervent drive to further diminish this figure. This fuels China’s leadership in expanding nuclear capabilities as an alternative to coal.

Regardless if it’s coal or natural gas, it doesn’t matter. Nuclear is nearly 100% more effective than any other energy technology at reducing carbon emissions.

These developments resonate strongly with investors, particularly in the context of Environmental, Social, and Governance (ESG) considerations. Many investors view nuclear energy as a low-carbon means of energy production, aligning with ESG principles. The rising importance of ESG considerations has sparked newfound interest in evaluating nuclear energy’s place within this framework.

Overall, the reliability and low-carbon nature of nuclear energy underscore its significance in pursuing cleaner and dependable energy solutions. There’s simply no reaching net zero without nuclear, and so uranium, too.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: GLDG.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

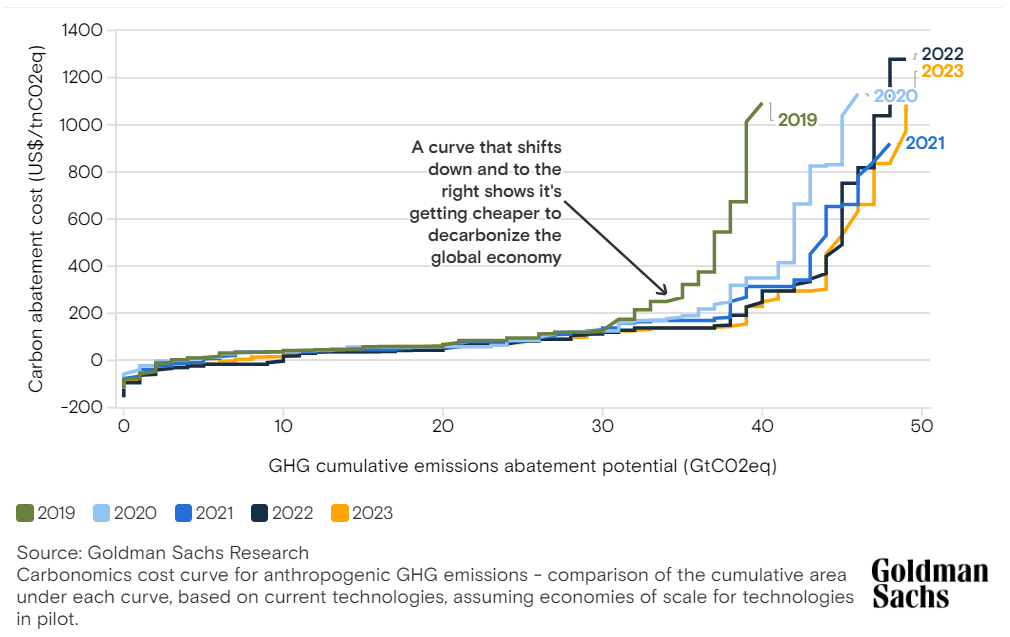

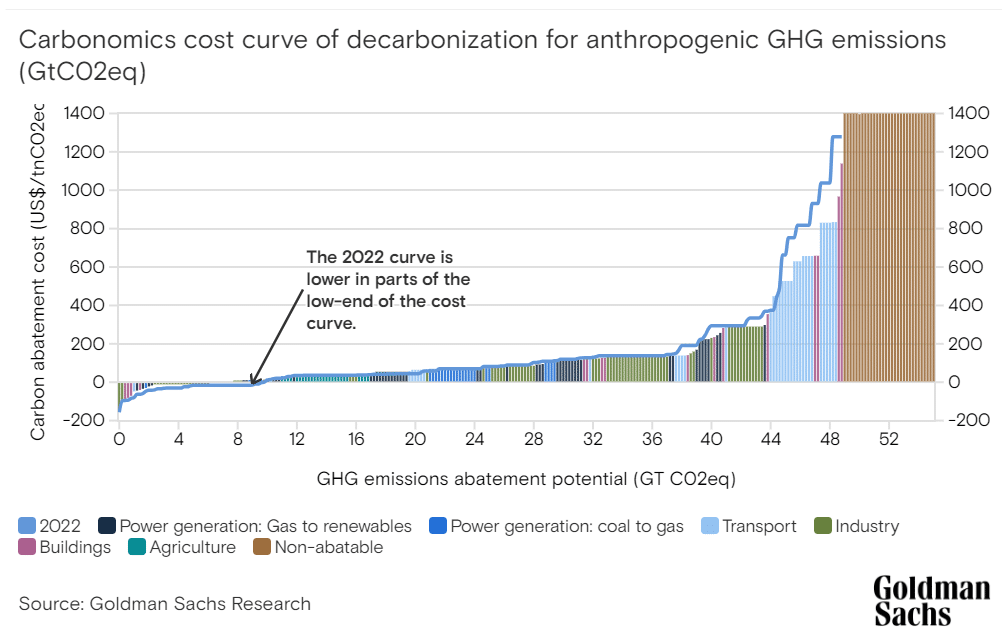

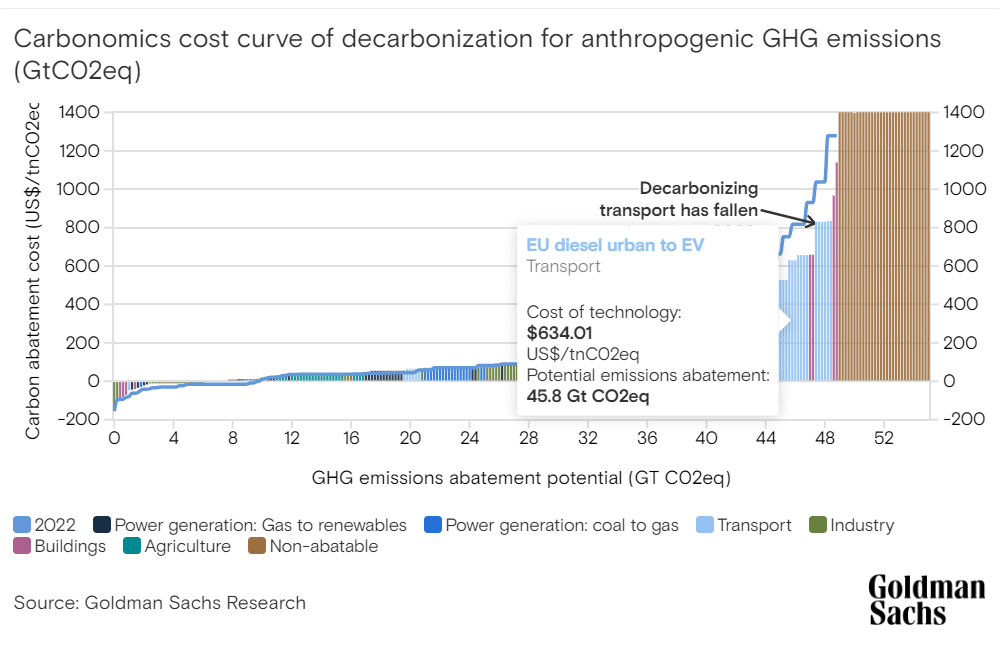

According to Goldman Sachs Research, the push to bring the global economy to net zero emissions is reaching a turning point. Certain clean technologies like solar and batteries have experienced shifts in their costs in 2023; some become more costly while others become more financially accessible, enhancing the affordability of decarbonization.

Riding the Cost Waves: 2023’s Clean Tech Shifts

Goldman Sachs’ analysis of the Carbonomics cost curve for 2023 reveals the influence of reduced energy prices coming from fossil fuels. This can consequently increase the cost of renewable energy sources.

Moreover, rising interest rates have also made construction expenses for projects most costly such as offshore wind energy. On the other hand, declining battery costs and the benefits of scaling up production of electric vehicles have made these technologies more economically viable.

Michele Della Vigna, leading Natural Resources Research in Europe, the Middle East, and Asia at Goldman Sachs Research, highlights a pivotal shift in the affordability of clean technology. He stated that:

“From here on, the deflationary forces [solar and batteries] are likely to win, and this brings back an affordability to the decarbonization path that not only accelerates it but makes it more attractive to the consumer.”

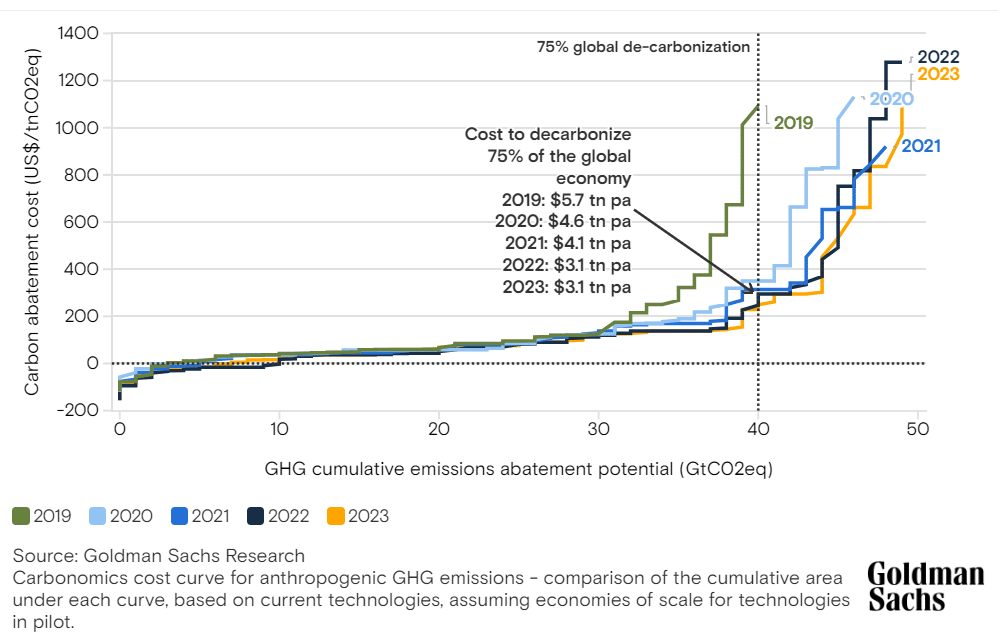

As per their analysis, the result shows a consistent flattening of the cost curve since 2019. The 2023’s curve suggests that the cost to remove 75% of planet-warming emissions remains the same from 2022.

The 2023 results also show an increase in costs in the lower half of the cost curve. This is largely due to increasing interest rates and cost inflation. While the impact of these factors overall is limited, they drive 25% increase in the renewable power sector.

Additionally, a significant improvement in battery costs for the transport sector made the high cost decarbonization more affordable. The sector gets 30% cheaper with improved batteries, lower raw material costs, and simpler cell-to-vehicle integration.

Looking ahead to 2024, a significant aspect to monitor will be the level of policy support for decarbonization. Though policy support reached $500 billion through the Inflation Reduction Act (IRA), political uncertainties and delays in certain areas may cause project delays.

Still, Della Vigna expects increased investment from the financial and corporate sectors. This surge in investment will focus on areas of decarbonization that are becoming more accessible and cost-effective. Solar installations and electric vehicles, in particular, stand out in their analysis.

However, the investment and spending currently in place may not be enough to achieve climate goals, Della Vigna added. If the goal is to keep global warming well within 1.5 degrees Celsius, then the world remains off course.

He noted that over the past year, global emissions have risen by 1%, reaching an all-time high. Coal demand has surged by 3%, and there has been a substantial $1 trillion worth of direct incentives for hydrocarbons. These trends don’t align with the pathway to achieve the 1.5-degree scenario.

Moreover, the world is now at the midway point between the 2015 Paris agreement and its 2030 targets. Summing up all the government commitments to decarbonization, the outcome leads to flat, not declining, emissions.

But for the 1.5-degree scenario, emissions would need to decrease by more than 50% by 2030. This stark contrast highlights the significant deviation from the required path to meet the climate objectives.

The Game-Changing Announcements at COP28

When it comes to the recently concluded COP28 climate conference in Dubai, there are three announcements that have the most impact to the market, per Della Vigna:

First is the growing green capex in the Gulf Coast region, estimated by Goldman Sachs Research to be over $600 billion over the next decade.

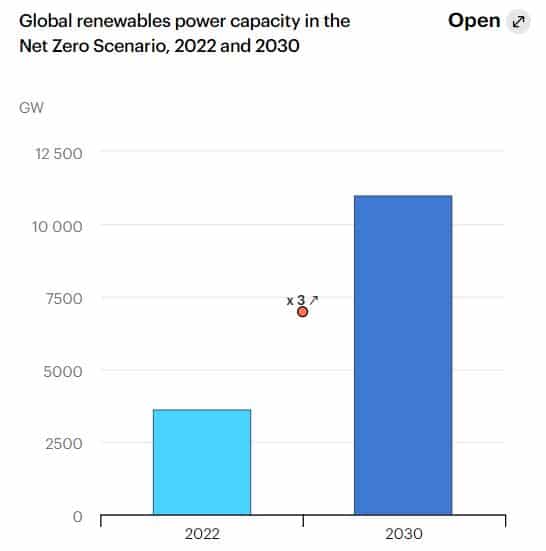

Next is the commitment to ramped up renewable power generation, which can improve affordability of clean technologies. The IEA’s updated Net Zero Roadmap shows that tripping global installed renewable energy capacity to 11,000 GW by 2030 will achieve the most emission reductions.

Last is the Oil and Gas Decarbonization Charter formed by 50 companies, targeting zero methane emissions and ending routine flaring by 2030.

Goldman Sachs’ 2023 Carbonomics analysis reveals a pivotal moment in global net zero journey. Fluctuating costs in clean tech pose challenges—lower fossil fuel prices raise renewable energy expenses while rising interest rates affect construction. Yet, falling battery costs and EV expansion boost viability while solar and batteries driving affordability accelerates decarbonization.

For the first time in over half a century, the US has granted permission for a novel nuclear reactor, signalling a growing openness among regulators toward diverse methods of generating power from nuclear fission.

California-based startup Kairos Power secured a construction permit from the Nuclear Regulatory Commission (NRC) for its Hermes demonstration reactor in Tennessee.

In contrast to current commercial reactors that use water for cooling, Kairos’s technology employs molten fluoride salt as a coolant.

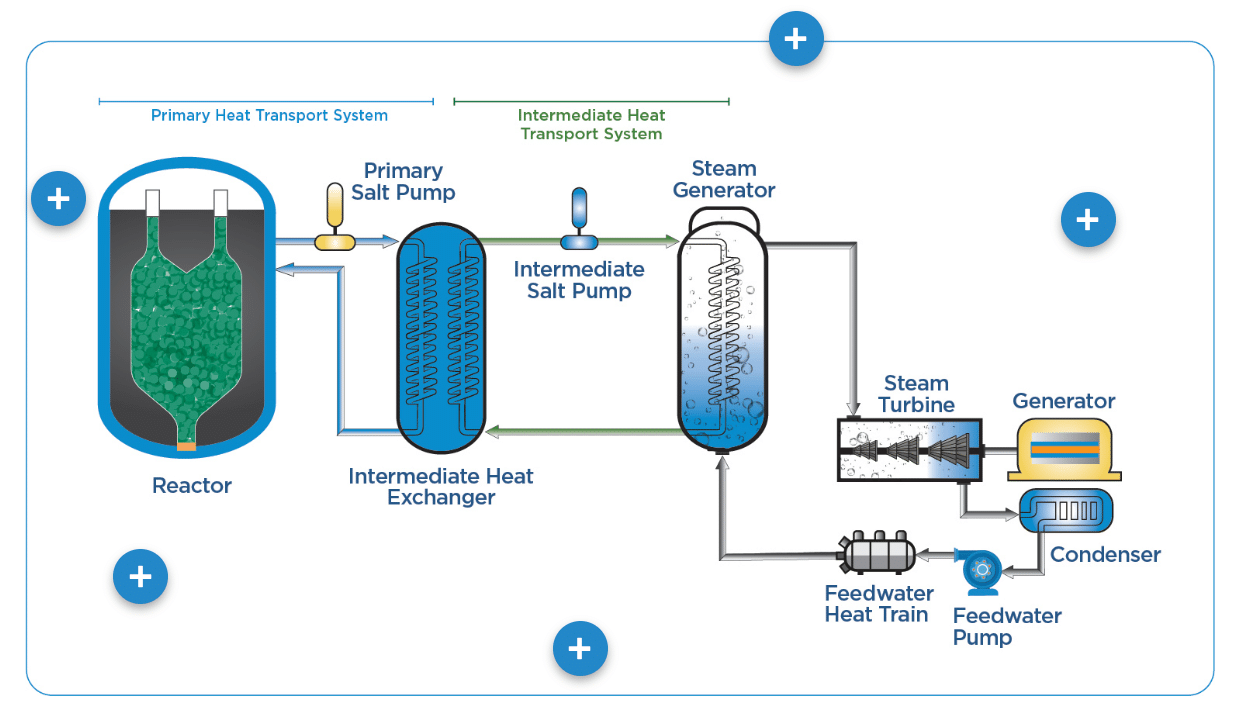

How Traditional Nuclear Reactor Works

The main function of the reactor centers on controlling nuclear fission, a process where atoms split and release energy.

Reactor fuel primarily contains uranium, processed into ceramic pellets and enclosed in sealed metal tubes known as fuel rods. These rods, often bundled together, form a fuel assembly.

A typical reactor core houses hundreds of these assemblies, varying with power capacity.

Within the reactor vessel, the fuel rods are submerged in water, serving as both coolant and moderator. The moderator slows down the neutrons generated by fission, sustaining the chain reaction. The heat generated by fission converts water into steam, driving turbines that generate clean electricity.

All commercial nuclear reactors in the U.S. are light-water reactors, employing ordinary water as both coolant and neutron moderator. Over 65% of U.S. commercial reactors are pressurized-water reactors (PWRs), circulating water under high pressure within the reactor core to prevent boiling.

Amidst the global drive to accelerate nuclear power deployment in the battle against climate change, regulatory processes have historically hindered the approval of new reactor designs.

According to Mike Laufer, Kairos Power’s CEO, the NRC has the potential to approve unconventional approaches. He also said in an interview that the regulatory pathway “doesn’t have to be a barrier.”

Kairos is one of numerous companies striving to market designs that can be manufactured in facilities and set up on-site. The company claims it to be swifter and more cost-effective compared to the conventional large-scale reactors available today.

How Kairos Reactor Technology Works

Kairos Power’s innovative reactor uses molten fluoride salt as a coolant, a departure from conventional water-cooled nuclear reactors. These salts have remarkable chemical stability and exceptional heat transfer capabilities at very high temperatures.

Image from Kairos Power website

Studies conducted on U.S. reactor designs confirm the compatibility of molten fluoride salts with standard high-temperature structural materials. This is to ensure reliability and a prolonged service life, thus further enhancing commercial viability.

The reactor employs fully ceramic fuel that maintains its structural integrity even under extremely high temperatures.

The U.S. National Laboratories have successfully demonstrated fabrication and testing methods for these fuels.

By using pebble-type fuel, Kairos Power reactors enable online refueling for reliability and operational availability.

Moreover, the reactor adapts a model-to-learn approach to optimize the transition to clean energy. This adaptive strategy promises cost reduction while allowing development of innovative nuclear technologies that can revolutionize the global energy landscape.

Kairos advanced reactor is a type of small nuclear reactor (SMR). The International Atomic Energy Agency (IAEA) defines ‘small’ as under 300 MWe capacity. Present-day large conventional reactors typically boast around 1,000 megawatts of capacity.

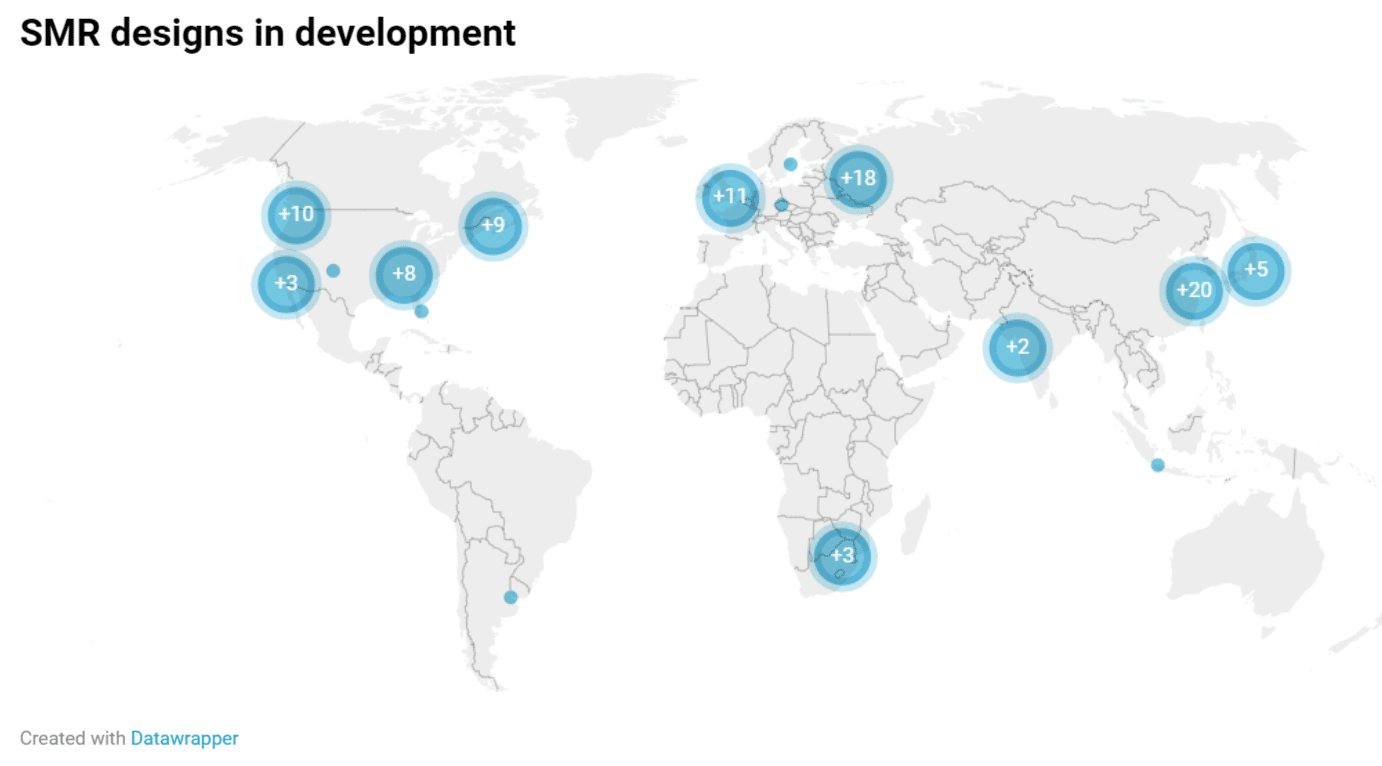

The New Era of Nuclear Power

SMR development is taking place in Western countries with growing private investment. The involvement of these small investors indicate a significant shift happening from public-led and -funded nuclear R&D to private-led. The goal is to deploy affordable clean energy sources without harmful carbon emissions.

Source: world-nuclear.org

In 2020, the Department of Energy announced initial $30 million funding support for 5 US-based teams developing affordable reactor technologies. One of them is Kairos Power for their Hermes Reduced-Scale Test Reactor, a scaled-down version of its fluoride salt-cooled high temperature reactor (KP-FHR).

Kairos plans to begin construction on its $100 million initiative next year and anticipates completing the system by the end of 2026.

The objective is to showcase the viability of its design and the molten salt technology, potentially offering safety advantages over water-cooled systems. Laufer highlighted that the last non-water-cooled design approved in the US was back in 1968.

While Hermes itself won’t generate electricity, it’s considered as a precursor to the Hermes 2 project. This next phase would involve two similar reactors capable of producing a combined output of approximately 28 megawatts of electricity.

The NRC is currently evaluating the company’s application for a construction permit for this venture.

Kairos’s ultimate vision involves a commercial endeavor featuring two larger reactors with a capacity exceeding 100 megawatts. However, Laufer indicated that it’s premature to speculate on the timeline for developments beyond the initial Hermes plant. He further noted that:

“We’re developing a technology that will be highly scalable. Affordability is really about being able to scale up.”

With the recent regulatory approval for its Hermes demonstration reactor, Kairos ushers in a new era of cleaner, safer, and scalable nuclear power. This innovative approach holds promise for addressing climate change by leveraging efficient, affordable, and sustainable energy sources.

A draft sheds light on the ongoing discussions and proposals within the United Nations climate talks, COP28, emphasizing the urgency to establish a global agreement aimed at phasing out fossil fuels while ramping up renewable energy and efficiency measures.

The draft highlights the need to use more renewables like wind and solar power and reduced use of energy, but drops the direct mention of fossil fuel phase out.

Over a 100 countries came to Dubai to support the phase out. If the draft would not get widespread support, negotiators may have to debate again. The text brings the following notable aspects to the fore:

Exploring Bold Objectives for Renewable Energy & Efficiency

Last year’s COP27 marked a milestone as it was the first time a COP decision specifically addressed coal. But despite attempts by 80+ countries at COP27 to expand this to encompass all fossil fuels, their efforts were thwarted by a handful of opposing nations.

Building upon this foundation, COP28 introduced ambitious objectives: to triple renewable energy capacity and double energy efficiency enhancements by 2030.

That translates to 11,000 GW of renewable energy and an average annual rate of energy efficiency of 4.1%. This reflects a commitment backed by 123 countries in a recent pledge, outlining the immediate need for a rapid transition.

Source: International Energy Agency 2023 Net Zero Roadmap

However, concerns arose regarding a paragraph in the agreement advocating for scaling up abatement and removal technologies such as CCUS. The scientific community highlights the limitations of these technologies, e.g. scalability and affordability, in fighting climate change.

Weighing Options for Fossil Fuel Exit

The COP28 debate intensifies with two options presented for the phaseout of fossil fuels.

Option 1 emphasizes a straightforward approach: “An orderly and just phase out of fossil fuels”. Option 2 invites the potential to phase out “unabated fossil fuels” and “rapidly reducing use to achieve net-zero CO2 in energy systems by or around mid-century”.

Climate experts pointed out that separating the discussions on scaling up renewables and efficiency from fossil fuel phase out raises an issue. They said that parties need to unify these aspects into a cohesive strategy centered on replacing fossils with renewable alternatives.

Emphasis on accelerated coal phase out gains support but is not enough without addressing oil and gas, experts add. Failure to include all fossil fuels will be deemed ineffective and inequitable, underscoring the need for a comprehensive approach.

But the agreed option at COP28 only noted coal while leaving out oil and gas:

“…the IPCC suggests a pathway involving a reduction of unabated coal use by 75% from 2019 levels by 2030”.

One specific area that speaks of clearly moving away from fossil fuels is in the transportation sector. “Rapidly increasing the deployment pace for zero-emission vehicles” (ZEVs). This involves putting an end to fossil fuel-powered vehicles.

Several alternatives currently exist for ZEVs, including battery-powered vehicles and hydrogen-powered vehicles.

Still, there remains the need to broaden discussions beyond electric vehicles to include public and active transportation, too.

The Need for Financial Backing

When it comes to financial support, substantial money is a must to phase out fossil fuels. Interestingly, the current draft’s text specifying financial support only adopts the COP27 agreement, as seen below.

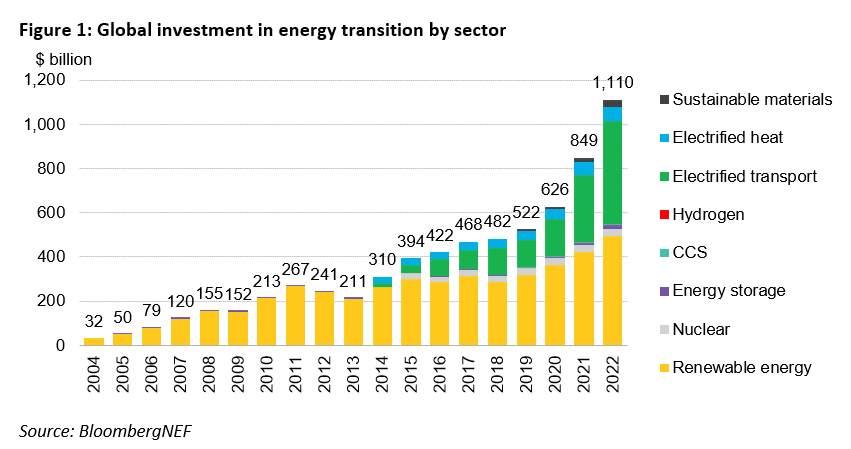

Earlier this year, BloombergNEF reported that global clean energy transition investment rose by 31% in 2022, at $1.1 trillion. Renewable energy and electrified transport sectors got the most funding.

While that’s quite an achievement, more funds are needed (>$3 trillion) until the decade’s end to reach net zero emissions. This means strengthening the current draft’s financial support package for a successful fossil fuel phase out.

Finally, there are suggestions to integrate energy transition considerations into Nationally Determined Contributions (NDCs) and long-term strategies under the Paris Agreement. This underlines the interconnectedness of climate goals and energy transitions.

As COP28 progresses, clearly addressing the fossil fuel phase out language will be critical in shaping an effective and equitable energy package the world needs to steer toward a decarbonized and sustainable future.

Uranium prices are a significant topic for investors, policymakers, and energy enthusiasts given its role in the global energy landscape. The uranium spot price is at 15-year high due to strong market demand and bullish long term outlook, confirming analysts’ forecast of a major sector rally.

As technology progresses, the demand for effective energy sources grows. Uranium holds a key position in generating nuclear power, making it a standout energy resource.

Basically, supply and demand dynamics do impact uranium prices. Rising nuclear power adoption also drives demand up while mining challenges and political tensions affect the supply side.

From 2019 onwards, the uranium market experienced a shortage in supply, depleting the surpluses accumulated since the Fukushima incident in 2011. This scarcity drove prices upward owing to limited availability.

Amid the soaring prices, mining uranium is costly; production expenses directly impact prices. Higher production costs set a price floor as miners avoid selling below production expenses.

National and global regulations also affect uranium markets. Stringent safety and environmental standards raise production costs, while policies supporting clean energy can stimulate demand.

The strong demand for uranium is further driven by its role in achieving net zero emissions and geopolitical risks. This prompted utilities to buy more than 150 million pounds of uranium in 2023, a record high since 2012.

It’s worthy to highlight that uranium prices aren’t just a number; it reflects the shifting global energy landscape. In addressing climate change and ensuring energy security, uranium continues to hold a critical role in the global energy mix.

Currently, there are 440 nuclear power plants across 33 countries, jointly contributing 10% of the world’s electricity supply. Moreover, plans are in place for an additional 90 nuclear reactors, while proposals exist for over 300 more.

The International Energy Agency stresses the necessity of doubling the size of the nuclear industry within the next two decades to meet net zero targets.

Right now, around 400 nuclear reactors are operational worldwide, highlighting the anticipated growth and importance of nuclear energy in the future energy landscape.

Decarbonizing the Global Energy Matrix

At the recently concluded COP28, a pivotal decision emerged: to triple nuclear energy capacity by 2050. It marks a substantial victory against emissions, which is not surprising.

Nuclear energy offers a high-output, low-carbon alternative to fossil fuels, a crucial step in reducing global warming.

A significant commitment has been made by the COP28 climate negotiators to boost nuclear energy by mid-century, aiding global decarbonization. The United States also joined the effort, signaling increased backing and potential funding for nuclear projects worldwide.

In addition to growing demand, there is also an influx of investment into the sector. Key players like Google and BNB Paribas are betting on nuclear, presenting a broader investment landscape in nuclear energy.

Finally, the International Atomic Energy Agency (IAEA) also fully supports the nuclear movement, bolstering confidence in nuclear power.

This significant shift signals a turn towards cleaner, more reliable, and cost-effective energy sources. With major nations like the U.S. onboard, significant government support and investment opportunities are anticipated in this growing market.

A comprehensive industry report also estimates that the global uranium market would reach an impressive $1,600 million by 2027. That represents a growth rate of over 7% from 2023.

Rising Uranium Prices’ Impact on Energy Shift

Nuclear is remarkably efficient, cutting CO2 emissions by nearly 100%, whether replacing coal or gas.

There would be net zero without nuclear. Understanding its price trends is pivotal, not only for the nuclear sector but also for the global energy direction.

While uranium prices are still below the all-time high of $136/lb. in 2007, there’s a strong optimism for record-breaking highs in the current bullish market. With rising investor attention, soaring demand, and focus on energy security, more increase in uranium prices is very likely.

Moving forward, multiple factors are poised to impact the uranium price, notably the role of nuclear energy in combating climate change globally. Corporate endeavors and government policies aimed at emission reduction play a pivotal role in this regard.

Despite criticism, nuclear power emerges as a credible option for providing consistent and substantial energy on a large scale as nations seek to curb carbon emissions.

We featured a very unique, fast moving company, GoldMining Inc (GLDG), and this price development is great news for their high-value assets. It’s one among the companies making waves in the uranium market.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: GLDG.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy