Disseminated on behalf of Sierra Madre Gold & Silver Ltd.

Sierra Madre Gold & Silver is building a strong position in Mexico’s growing precious metals industry. The company is creating long-term value through smart growth, low costs, and balanced exposure to both gold and silver. With gold prices at record highs, Sierra Madre is turning opportunity into steady progress.

Its main operation, the La Guitarra Mine Complex, reached commercial production in January 2025 after being acquired from First Majestic Silver. Alongside this, the company holds the Tepic Project, expanding Mexico’s gold and silver frontier. By combining efficient mining with new exploration, Sierra Madre is proving that gold’s value still shines bright in today’s market.

Gold’s Strength in a Changing World

Gold remains a trusted safe-haven asset in uncertain times. Central banks are buying more gold, and geopolitical tensions are pushing demand higher. JP Morgan expects gold prices to average $3,675–$4,000 per ounce by mid-2026. State Street Global Advisors sees gold holding above $3,000/oz, showing that strong prices are here to stay.

The Demand and Supply Side

As per the World Gold Council, in Q2 2025, total gold demand reached 1,249 tonnes, up 3% year-over-year. Its value surged 45% to a record US$132 billion, driven by strong investment demand. Gold-backed ETFs, bars, and coins saw the biggest gains amid geopolitical tensions and trade uncertainty. Central banks added 166 tonnes to reserves, though at a slower pace than in previous quarters.

On the supply side, total gold output also rose 3% to 1,249 tonnes, with mine production hitting a Q2 record of 909 tonnes.

This environment supports Sierra Madre’s growth strategy. The company is using these high prices and Mexico’s low operating costs to boost production and deliver stronger returns to shareholders.

Driving Gold Growth at La Guitarra

The La Guitarra Mine Complex is Sierra Madre’s key asset. Located in Mexico’s historic Temascaltepec district, it currently produces 500 tonnes per day. The company plans to double that to 1,200 t/d to 1,500 t/d by late 2027.

In April 2025, Sierra Madre started underground mining at the high-grade Coloso vein within the La Guitarra property. This new zone should increase gold output and improve overall grades. At the same time, the company is upgrading its milling systems to raise recovery rates and lower costs.

Tepic Project: Expanding Mexico’s Gold and Silver Frontier

The Tepic Project adds exciting exploration upside. It sits in Mexico’s Sierra Madre Geologic Province and hosts low-sulfidation epithermal gold and silver mineralization. Multiple zones stretch over one kilometer long and 200 meters wide.

Once the flagship project of Cream Minerals, Tepic has a historic resource estimate outlined in a 2020 Technical Report. Past drilling covered 31,537 meters across 149 holes. However, with a 76% core recovery rate, grades may have been underestimated.

Recent exploration shows the Dos Hornos breccia veins remain open both along strike and at depth. This finding suggests strong potential for expanding resources in future drilling phases.

Core Drilling Highlights

Location and Infrastructure Benefits

Tepic is just 22 km from Tepic City, the capital of Nayarit, and 120 km from Puerto Vallarta Airport. The project has excellent access to roads, power, and local services. A skilled mining workforce and nearby fabrication shops make operations easier and more cost-efficient.

The project covers 2,612.5 hectares across five mining concessions and is 100% owned by Sierra Madre. Being in a mining-friendly region of Mexico gives the company a stable environment to advance this asset.

Strong Gold Production and Steady Revenue

Sierra Madre’s production results show steady progress and solid performance:

- Q2 2025 gold sales: 1,096 ounces.

- H1 2025 gold sales: 2,118 ounces; production totaled 2,049 ounces.

- Average realized price: $3,271/oz in Q2 and $3,058/oz for H1.

- Gold recovery: around 78% during the first half of 2025.

Gold revenues reached $3.59 million in Q2 2025, up from $2.89 million in Q1. For the first half of 2025, gold generated $6.48 million in total revenue. Cash costs per silver-equivalent ounce sold were $23.32, showing strong cost control.

As the Coloso mine continues to deliver higher-grade mineralization, Sierra Madre expects better margins and lower costs in the coming quarters.

Financing Growth and Exploration Plans

In mid-2025, Sierra Madre raised C$19.5 million (US$19.5 million) through a private placement. The funds are being used to:

- Expand throughput at La Guitarra.

- Launch a +20,000-meter exploration program across 59 km of structures mapped to date.

- Target new high-grade zones in the East District.

This financing strengthens the company’s ability to expand production and extend mine life while continuing to explore new areas.

Moving on, Sierra Madre has also begun underground development at the Nazareno silver-gold mine in the La Guitarra complex, Estado de Mexico. The team has delivered over 700 tonnes of mineralized material, not included in the current resource estimate, to the Guitarra mill. Workers are blasting existing workings and advancing the sill drive to test long-hole mining feasibility in the closely spaced veins.

Reconciliation with the 2023 Nazareno resource model shows silver grades 40% higher and gold grades 30% higher than estimated, signaling strong potential to expand the resource.

Taking Advantage of Record Metal Prices

Gold is trading above $4,000 per ounce, giving Sierra Madre a strong tailwind. Its mix of gold and silver exposure provides a natural balance – gold supports financial stability, while silver adds growth potential.

Analysts also believe that Silver is expected to face a structural deficit for the seventh straight year, due to rising demand from the clean energy and technology sectors. This gives Sierra Madre’s dual-metal strategy even more value in the current market.

Two Metals, One Strong Strategy

Sierra Madre’s dual focus sets it apart. Gold anchors the company’s stability as a safe-haven asset, while silver brings growth potential through its industrial uses — from solar panels to electric vehicles.

With a combination of efficient operations, strong assets, and focused execution, Sierra Madre is redefining what a modern Mexican mining company looks like one that blends stability with growth potential.

- FURTHER READING: Silver’s New Role in the Clean Energy Era – and What It Means for Sierra Madre Investors

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Sierra Madre Gold and Silver Ltd. (“Company”) made a one-time payment of $25,000 to provide marketing services for a term of one month. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2024, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

For more information on the Company, investors should review the Company’s continuous disclosure filings available on SEDAR+ at www.sedarplus.ca.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

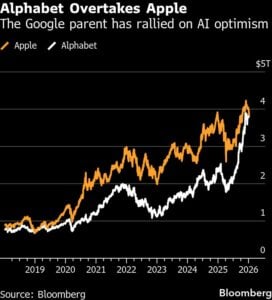

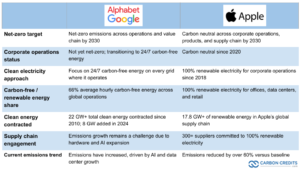

Surpasses Apple in Value: But How About Their Climate Ambitions and Progress?")

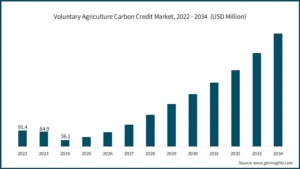

Methane reduction projects tied to rice farming are quickly growing. Some forecasts show these initiatives could grow by nearly 38% through the early 2030s. This highlights their rising importance in the agricultural carbon credit market.

Methane reduction projects tied to rice farming are quickly growing. Some forecasts show these initiatives could grow by nearly 38% through the early 2030s. This highlights their rising importance in the agricultural carbon credit market.