As the world gears up for the upcoming UN climate summit, COP29, in Baku, Azerbaijan, the G-20 governments face the challenge of crafting more ambitious climate plans. These plans must balance bold climate commitments with economic realities like budget constraints, a cost-of-living crisis, and the push for energy independence. The situation is further complicated by recent election outcomes.

However, not all G-20 countries are moving at the same pace. The latest Climate Policy Factbook by BloombergNEF, commissioned by Bloomberg Philanthropies, evaluates G-20 progress in three crucial policy areas:

- Fossil-fuel subsidies,

- Carbon pricing, and

- Climate-risk policies.

Here’s our key takeaways from the report.

Fossil-Fuel Subsidies Surge Despite Climate Goals

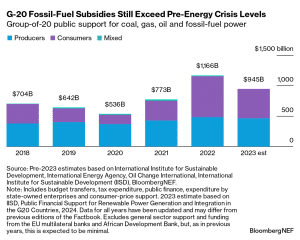

In 2022, G-20 countries provided a staggering $1.1 trillion in fossil-fuel support, the highest in over a decade. This spike was driven by the global energy crisis, as governments aimed to shield consumers from soaring energy costs.

However, $500 billion of this went to producers and utilities, some of which reported record profits.

Despite global climate goals, the G-20 is expanding its coal power capacity. From 2019 to 2023, coal-fired capacity grew by 3%, adding up to 2 terawatts (TW) of operational capacity, with another 0.6 TW in development. Coal remains the largest contributor to climate change.

The distribution of fossil-fuel support by type has remained largely unchanged in recent years. Although coal represents a small portion, its share is significant due to the high overall fossil-fuel support in 2022. G-20 governments allocated $49 billion to coal, the most emissions-intensive fuel.

Remarkably, OECD members reduced coal capacity by 22% since 2019. Conversely, non-OECD economies increased their coal capacity by 6%.

Country Progress

Australia is showing improvement by reducing coal-fired capacity and lowering fossil-fuel support in 2022. Meanwhile, China and Japan are labeled as making insufficient progress while Canada and the UK were downgraded to “mixed progress.”

Preliminary 2023 data suggests fossil-fuel subsidies fell to $945 billion, a 19% decrease from 2022 but still above pre-crisis levels. Reforming these subsidies is politically sensitive, as it could raise consumer prices.

Canada offers a potential pathway by defining and eliminating inefficient fossil-fuel subsidies.

Carbon Pricing Gains Traction, But Is It Enough?

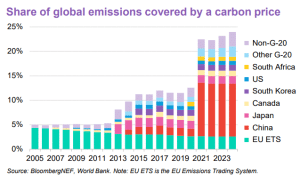

Carbon pricing is becoming more widespread across the bloc. It now account for about 25% of global greenhouse gas emissions and 29% of G-20 emissions through taxes or trading schemes, per BNEF analysis. This share is expected to grow as more programs roll out.

Currently, 14 G-20 economies, including the EU, have economy-wide carbon pricing mechanisms. Russia and the US have subnational schemes, while South Africa remains the only African Union member with a carbon tax in place.

While some G-20 countries, like Australia, China, and South Africa, have seen rising carbon prices, others, particularly in Europe, experienced declines. Only the EU’s Emission Trading Scheme (ETS) currently operates within the price range necessary to limit global warming to 2°C by 2030.

Expanding Carbon Markets

Canada, France, Germany, and Mexico lead the pack with multiple national-level carbon taxes or markets.

Brazil, India, and Turkey are designing compliance carbon markets while Indonesia and Japan are considering additional carbon pricing programs. And all EU members will see another carbon market with the 2027 launch of the road transport and buildings ETS.

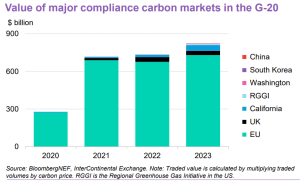

Notably, China’s carbon market, the largest globally by covered emissions, is set to expand to aluminum, steel, and cement sectors. The EU ETS leads in traded value, driven by higher prices and trading volumes, whereas Canada and California are on track to meet their targets by the end of the decade.

Carbon Market Valuations

The combined value of G-20 compliance carbon markets exceeded $800 billion in 2023, BNEF Factbook shows. Price increases across these markets stemmed from policy reforms aligning with climate goals, though trading volumes dipped in some due to economic impacts from Russia’s invasion of Ukraine.

As G-20 members strengthen their carbon markets, they create powerful incentives for emission reductions and sector-specific adaptation. As such, they can contribute significantly to the transition toward a low-carbon global economy.

Climate-Risk Policy: Who’s Leading and Who’s Lagging

G-20 members are at varying stages of implementing climate-risk regulations. Some, like the EU, Brazil, and the UK, lead the charge with comprehensive frameworks.

However, others, including Argentina, Saudi Arabia, and Russia, lag behind, lacking even basic regulations. Other remarkable recent developments in this area include:

- Turkey and the US made notable strides in climate-risk policy.

- Nine G-20 countries have adopted or are developing regulations aligned with the International Sustainability Standards Board (ISSB).

The ISSB framework promotes consistency in climate-risk reporting. However, its effectiveness could be undermined by local variations and relatively low stringency.

What COP29 Means for G-20 Climate Action

The G-20’s progress is uneven, with some countries advancing robust policies while others remain stuck in outdated systems. COP29 presents a crucial opportunity for world leaders to reassess their commitments and bridge these gaps.

Based on BNEF’s Climate Policy Factbook data, to accelerate the transition to a low-carbon economy, countries must:

- Phase out fossil-fuel subsidies, starting with inefficient ones.

- Strengthen carbon pricing mechanisms to provide real incentives.

- Implement stringent climate-risk policies to build a more resilient economy.

Ultimately, meaningful climate action requires global cooperation and bold leadership, particularly from the G-20, which holds the key to the planet’s future.