You most likely know the climate benefits of storing carbon and removing gigatons of it from the atmosphere to limit climate change.

But we also bet that you don’t clearly understand how much carbon storage provides value to meeting climate goals.

That’s understandable because there’s currently no single framework for thinking about the climate benefits of temporary carbon storage. Temporary means less than a century of carbon storage.

Several factors affect how carbon accounting is done such as the time horizon over which value is calculated.

Most people equate the benefits of carbon storage with the impacts of CO₂ emissions. For instance, different years of storage (10 yr, 50 yr, or 100 yr) are used for representing offset credit to justify the emission of a tonne of CO₂.

But there’s a growing interest in one family of carbon accounting methods called tonne year accounting (also referred to as “ton-year” accounting). It values carbon storage based on its duration.

Firms use this method to bundle short-term carbon storage into carbon offsets designed to offer permanent climate solutions.

Unfortunately, various tonne year accounting methods provide different interpretations. This makes it harder to know what’s the real value of temporary carbon storage.

This article will explain how tonne year accounting works and what assumptions it should have when valuing temporary carbon storage.

There are also some examples of the most prevalent methods to know their differences.

Breaking the Tonne Year Accounting Process into Steps

Tonne year accounting is a family of methods for measuring how many tonnes of CO₂ stored physically equals to avoiding CO₂ emission in the first place.

In other words, it quantifies the climate impacts of carbon emissions with two things:

- The amount of CO₂ involved and

- The time CO₂ stays in the atmosphere.

This accounting method claims that a larger amount of CO₂ stored for a shorter period of time can claim equivalent climate outcomes. And the same also goes for a smaller amount of CO₂ stored for a longer period of time.

Here’s how tonne year accounting works in five basic steps.

#1. Specify a unit

The very first step to do is to specify a unit that considers both the number of tonnes of carbon stored as well as the time over which they’re stored.

- Concept defined: a tonne year refers to 1 metric ton (MTCO₂) of carbon dioxide held somewhere for 1 year.

For instance, a mangrove tree that holds 1 MTCO₂ for 5 years provides 5 tonne years of carbon storage. But if that same tree can hold 2 MTCO₂ for 10 years, then it delivers 20 tonne years of carbon storage.

#2. Choose a time horizon

The second step is to know how to value the costs and benefits of storing carbon that happen in the future. This is possible by deciding on a time horizon. Doing this is a normative or typical choice rather than scientific.

The shorter the time horizon, the more valuable temporary carbon storage will seem.

#3. Get the tonne year cost of emission

After specifying the unit and choosing the time horizon, you can now calculate the climate impact of emissions in tonne years.

- If an emission “costs” X tonne years, then tonne year accounting suggests that you can get carbon storage providing X tonne years of benefit to offset that mission.

When CO₂ stays in the atmosphere permanently, the impact of emissions in tonne years will be:

quantity of CO₂ emitted x time horizon chosen

So, if there’s 1 MTCO₂ emitted for 100 years, that’s equal to 100 tonne years.

But atmospheric CO₂ concentrations aren’t affected by emissions alone. In practice, knowing the cost of emissions has to take into account also the parts of the global carbon cycle that remove CO₂ from the air.

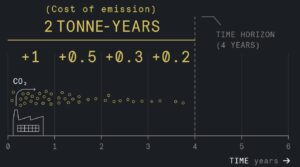

For example, if 1 MTCO₂ is emitted and removed from the atmosphere by natural processes over 4 years.

In the first year, the 1 MTCO₂ equals 1 tonne year of emissions impact. In the next year, there’s only 0.5 MTCO₂ that results in another 0.5 tonne years of impact.

Following the same logic, impacts for year 3 and year 4 are 0.3 and 0.2 tonne years respectively as shown below. Summing all the impact over the 4-year time horizon results in a total cost of 2 tonne years.

#4. Calculate the tonne years of carbon storage solution

This is important when comparing the tonne year cost of emissions with a temporary storage project.

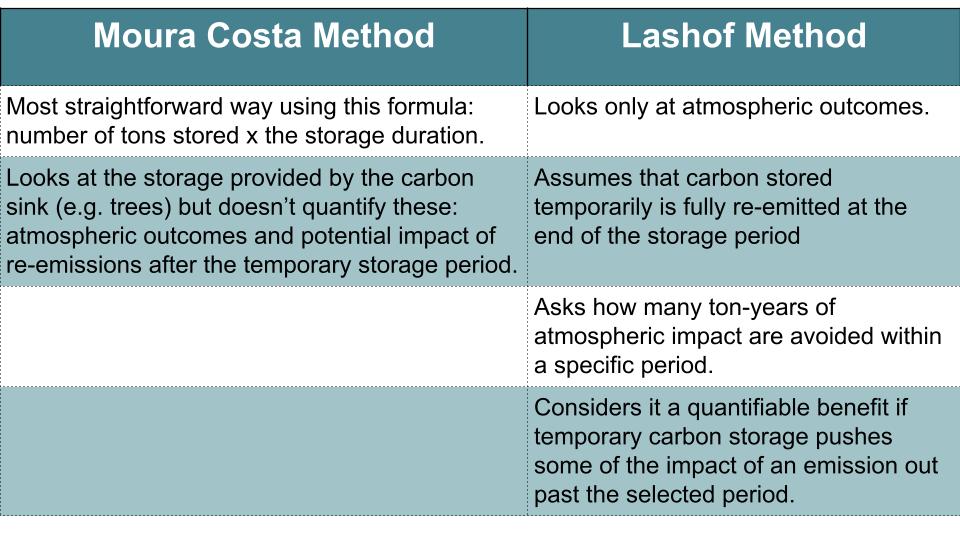

There are various methods for calculating this benefit, but the two most common models are the Moura Costa and Lashof methods.

Here’s how the two methods differ in coming up with the carbon storage benefit calculation.

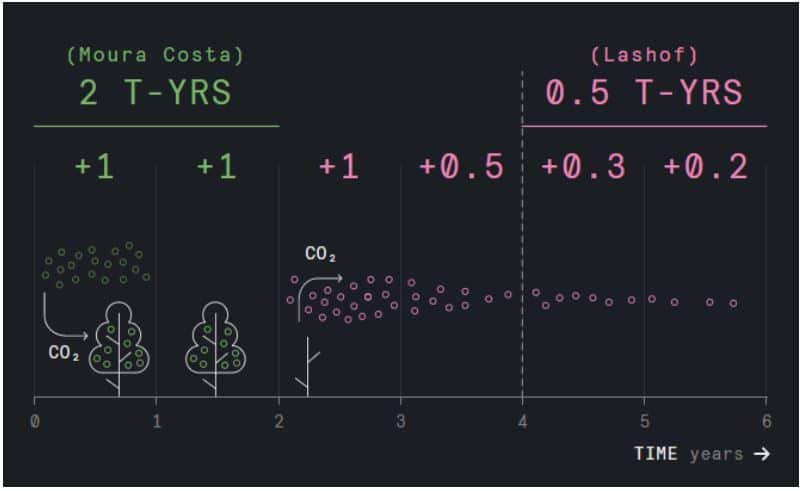

The figure below shows how the two approaches differ in getting the benefit of temporary carbon storage in 4 years. Moura Costa calculates 2 tonne years while Lashof only has 0.5 tonne year benefit.

#5. Determine how much storage is needed for offsetting

The last step in a tonne year accounting process is determining how much temporary storage you need to offset your emission. This is crucial when making an equivalence claim.

- The answer is in an equivalence ratio: tonne year cost of emissions / tonne year benefit of temporary storage.

Using the above formula, the results vary in two methods with a 2 years time horizon.

Moura Costa accounting: 2 tonne years / 2 tonne years = 1 (equivalence ratio). This means storing 1 tCO₂ for 2 years can offset 100% of the emission.

Lashof accounting: 2 tonne years / 0.5 tonne years = 4 (equivalence ratio). It means only 25% of the emission can be offset by the project.

The results are significantly different, yet emitters can apply either accounting method and use it in determining the carbon offset that temporary storage provides.

Both of them can even be regarded as an offset equal to 1 MTCO₂, which can be an issue when offsetting emissions.

Linking Tonne Year Accounting to Climate Impact

Tonne year accounting is used to calculate the correct equivalence ratio and relate it to the climate impacts that the entire world is experiencing.

Unlike the simplified example calculation provided above, this one calls for a more realistic situation on the effects of emissions on the atmosphere. This means considering the changes in the global carbon cycle due to emitting more carbon.

- Naturally, oceans and other carbon sinks take up the extra CO₂ when their concentrations go up. This lowers the cost of the emission.

But instead of taking into account all those natural processes, tonne year accounting methods simplify things by treating emissions as a function of time represented in curves.

Those curves make it easier to know the impact of carbon in tonne years without using complicated modeling.

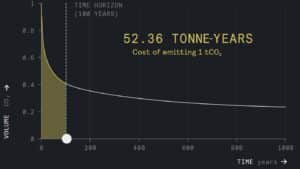

Rather than going through all the formulas used earlier, tonne year accounting lets you get the cost of emitting 1 tCO₂ by integrating the time horizon under a CO₂ emission curve. Refer to the figure below.

As shown above, tonne year accounting estimates the amount of extra heat trapped in the atmosphere due to emission. This leads to damaging climate effects such as rising sea-levels.

Alternatively, temporary carbon storage reduces warming. If the reduction balances out with the added emission, then tonne year accounting may claim the corresponding equivalence.

However, when balancing or offsetting climate impacts, the accounting method must take into account the timeframe when comparing tonne year results.

Though you can use a 10-year horizon, it may not represent the real climate impact of carbon. It can last for a much longer time in the atmosphere than 10 years.

Not to mention that there are other climate outcomes affected by emitting CO₂ at a given time. They particularly include the critical global warming limits of 1.5 or 2 degrees.

In a sense, storing 1 MTCO₂ today but re-emitting it many years later will only kick the can down the road.

Once the temporary storage ends, how should an emitter take this into account towards long-term climate goals?

Sadly, tonne year accounting can’t address the concern. It simply takes into consideration the added heat trapped in the atmosphere – also called cumulative radiative forcing. For other climate impacts, this assumption does not apply.

Also notably, the Moura Costa method results in physical equivalence claims that don’t add up. It allows for the claim that temporarily storing 1 MTCO₂ justifies the emission of more than 1 MTCO₂ (1.91 MTCO₂).

That is not a defensible outcome; hence, it may not be useful in making equivalence emission claims.

Analysts prefer to use the Lashof accounting instead as it shows a defensible result when considering the cost of emission in tonne year as well as its benefit.

Making Sense of All the Elements with Examples

Regardless of the method, Moura Costa or Lashof, changing the input parameters can affect the value of temporary carbon storage.

- For example, if the time horizon chosen is 1000 years, the cost of an emission is about 310 tonne years.

Lashof calculates that 1 MTCO₂ stored for 1 year will result in about 0.235 tonne year benefit. So, for the equivalence claims, you need to store about 1319 MTCO₂ for 1 year (310.161 / 0.235 = 1319.45).

Lowering the time horizon to 100 years, storage also reduces to 128 tCO₂ under Lashof accounting.

To make things clearer, we take the case of a company called NCX.

An independent analysis reveals that the NCX accounting method is identical to the Lashof method but with one critical difference – a 3.3% discount rate.

Applying the discount rate makes the accounting process more complex. The primary goal of tonne year accounting is to generate the physical equivalence claims. So, using a discount rate invalidates this claim.

Both temporary carbon storage and emitting CO₂ result in quantifiable changes to the Earth’s energy balance. This means we must compare them directly without discount rates.

By applying a discount rate, the entity makes an economic equivalence claim instead of a physical equivalence claim. So, if they market their credits as generating equivalent climate impacts, it may raise questions.

- That is because using a discount rate allows for more climate impacts tomorrow in exchange for temporary climate benefits today.

Right now, carbon markets assume that all carbon credits justify ongoing CO₂ emissions on a physical equivalence claim.

For instance, an entity releasing 10 MTCO₂ needs to buy only 10 offset credits to negate the climate impacts of its emissions.

In such a case, using tonne year accounting with discount rates becomes inconsistent. So, whoever sells credits on this basis has to make its equivalence claims clear and transparent.

The tendency is for firms to overestimate the physical value of temporary carbon storage. If so, they issue more carbon credits than the climate benefits those credits can support.

NCX’s current accounting method does exactly that. A reconsideration may be necessary to avoid complications and proper accounting of an offset’s physical equivalence claim.

Key Takeaways

To wrap things up, here are the major points we can say about the use of tonne year accounting.

The different tonne year methods allow varying quantities of temporary carbon storage to be marketed as equivalent to 1 MTCO₂. So assumptions must be clear – time horizon or use of a discount rate.

It is only useful for equivalence claims about climate damages due to extra energy trapped in the atmosphere.

Equivalence claims made by some tonne year methods don’t match climate impact. They’re not useful in establishing climate-equivalence claims or issuing carbon offsets.

Application of discount rates within tonne year accounting can blur the real climate impacts of temporary carbon storage.

Temporary storage has a non-zero value, but it’s important to be open and transparent about both the risks and benefits that come when valuing it.

Overall, more work is necessary to establish a coherent framework for valuing temporary carbon storage.