Australia and the United States have launched a $3.5 billion critical minerals partnership, marking one of the largest bilateral efforts to secure materials essential for clean energy and electric vehicles (EVs).

The agreement focuses on strengthening supply chains for minerals such as lithium, cobalt, nickel, and rare earth elements. These materials are vital for batteries, solar panels, wind turbines, and other low-carbon technologies.

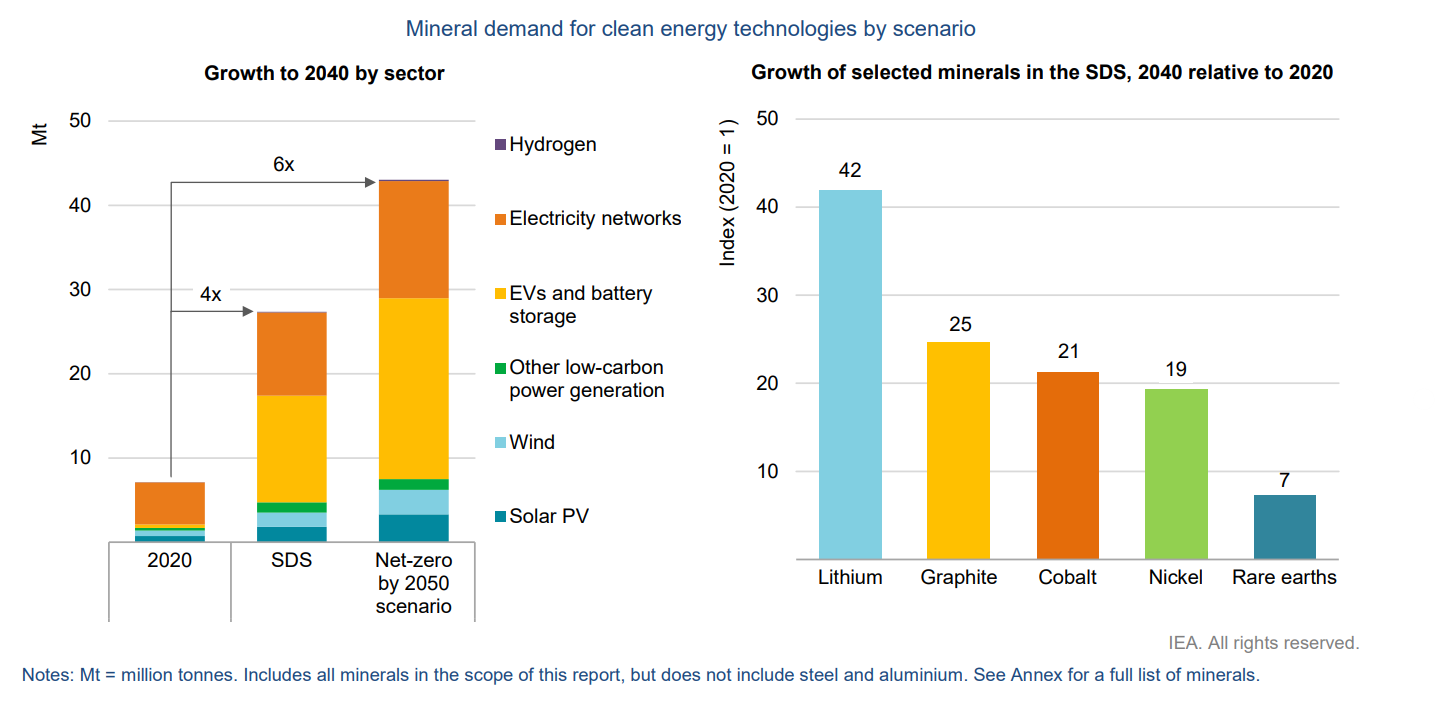

The deal comes as global demand for these minerals rises sharply. The International Energy Agency estimates that demand for critical minerals could quadruple by 2040 under net-zero scenarios. Lithium demand alone could grow more than 40 times by 2040, driven by EV adoption and battery storage.

Australia plays a central role in this supply chain. It currently produces about 55% of the world’s lithium, making it the largest global supplier. However, much of the processing still takes place overseas, creating supply risks for Western economies.

The new partnership aims to address this gap by boosting both extraction and domestic processing capacity.

Billions Back the Full Value Chain—from Mine to Market

The $3.5 billion investment will be deployed over seven years. The United States will give around $2.1 billion. This funding comes from the Defense Production Act and the Infrastructure Investment and Jobs Act. Australia will provide $1.4 billion through national financing programs.

The funding is designed to support the full value chain, from mining to refining to advanced research. The main areas of investment include:

- $1.8 billion for new mining projects and infrastructure upgrades

- $1.2 billion for processing and refining facilities

- $500 million for research, innovation, and sustainable extraction technologies

A key goal is to reduce reliance on external processing markets and build more resilient supply chains. This includes expanding refining capacity for lithium and rare earth elements, which are often processed outside producing countries.

The partnership is also expected to create economic benefits. Government estimates say about 15,000 direct jobs will be created. Additionally, around 30,000 indirect jobs will come from supply chains and related industries.

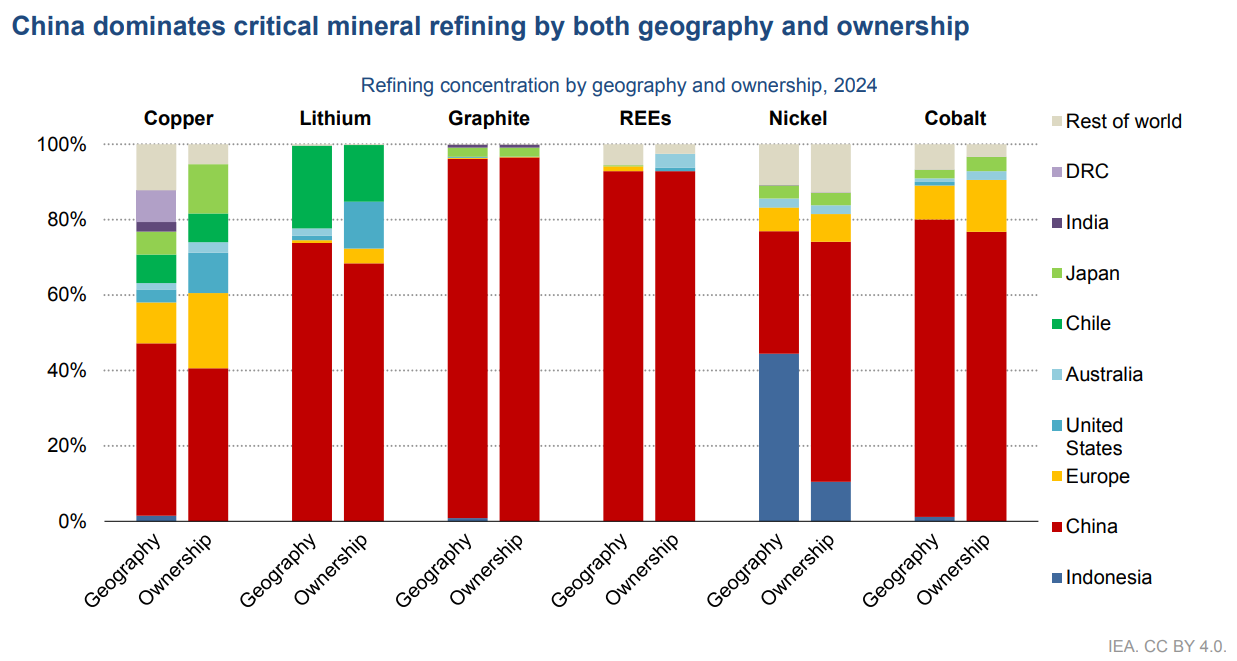

Breaking China’s Grip on Mineral Processing

The agreement reflects growing concern over the concentration of mineral processing in China. Currently, China dominates key parts of the global supply chain.

According to the International Energy Agency:

- China handles about 60% of global lithium processing

- It controls more than 80% of rare earth refining

- It also leads in battery component manufacturing

This dominance creates risks for supply security, pricing, and geopolitical stability. Disruptions in one region can affect global clean energy deployment.

By investing in alternative supply chains, Australia and the United States aim to diversify production and reduce these risks. The partnership could also encourage other countries to develop their own critical minerals strategies.

In addition, the deal may help stabilize prices for key materials. Volatility in lithium and nickel markets has impacted EV production costs. It has also delayed some renewable energy projects in recent years.

Supporting Climate Goals and the Energy Transition

The partnership has direct implications for global climate efforts. Critical minerals are essential for scaling clean energy technologies. Without a reliable supply, the pace of decarbonization could slow.

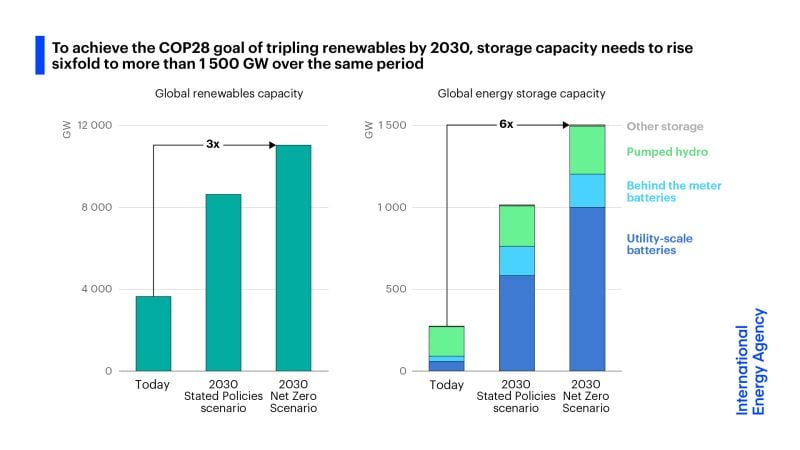

Battery storage is a key example. Energy storage systems help manage the variability of renewable energy sources like solar and wind. Expanding mineral supply will support the growth of these systems.

The IEA projects that global battery capacity must increase significantly to meet climate targets. Some estimates suggest energy storage capacity needs to grow more than sixfold by 2030 to stay on track for net-zero emissions.

The US-Australia alliance could help unlock this growth by ensuring stable access to raw materials. This, in turn, may reduce costs for batteries and renewable energy systems over time.

Both countries have also committed to improving environmental standards in mining. This includes reducing emissions, improving water management, and limiting land impacts. These measures are important because mining itself can be carbon-intensive.

Efforts to lower emissions in mineral extraction could also influence carbon accounting frameworks. As supply chains become more transparent, companies may need to track and report emissions linked to raw material sourcing.

ESG, Carbon Markets, and the New Mining Reality

The expansion of critical minerals supply chains is expected to influence carbon markets and ESG strategies.

As mining activity increases, so does the need to manage emissions. This could increase the need for carbon credits in the extractive sector. This is true for projects that cut or offset emissions from mining.

At the same time, improved supply chains for clean technologies may accelerate renewable energy deployment. This could support carbon reduction efforts across multiple sectors, including power generation and transportation.

The partnership may also lead to higher standards for responsible sourcing. Materials produced under strict environmental and social guidelines could command a premium in global markets.

This shift aligns with growing investor focus on ESG performance. Companies face growing pressure to show that their supply chains meet sustainability standards. This includes tracking emissions across Scope 1, 2, and 3 categories.

Over time, these trends could reshape how carbon credits are used. Companies may focus more on cutting emissions directly in their supply chains, rather than just using offsets.

Industry Scrambles to Secure the Next Wave of Supply

The announcement has received strong support from industry players. Major automakers and battery manufacturers are seeking secure and stable supplies of critical minerals. Companies like Tesla, Ford, and General Motors want to source materials from projects tied to the partnership.

Mining firms are also responding. Albemarle Corporation and Pilbara Minerals will likely gain from more investment and quicker project timelines.

Investor interest in the sector is rising as well. Global spending on energy transition minerals is growing rapidly, supported by both public and private capital.

The International Energy Agency reports that investment in critical minerals has increased sharply in recent years. This trend is expected to continue as countries compete to secure supply chains for clean energy technologies.

A Defining Shift in the Global Energy Economy

The $3.5 billion Australia–US critical minerals partnership represents a major step in reshaping global energy supply chains. It addresses a key bottleneck in the transition to a low-carbon economy: access to essential raw materials.

In the short term, the deal may help stabilize supply and reduce risks linked to market concentration. In the long term, it could accelerate the deployment of clean energy technologies and support global climate goals.

For carbon markets, the impact is indirect but important. More minerals can help speed up the use of renewables and energy storage. This, in turn, cuts emissions throughout the economy. At the same time, higher mining activity may drive demand for carbon credits and new emissions reduction strategies within the sector.

The success of the partnership will depend on execution. Expanding mining and processing capacity takes time, investment, and strong environmental oversight.

If these challenges are addressed, the alliance could serve as a model for future international cooperation on critical minerals. It also highlights how energy security, economic policy, and climate action are becoming increasingly connected.

Ultimately, as demand for clean energy continues to grow, securing sustainable and reliable mineral supply chains will remain a key priority for governments and industries worldwide.