A war in the Middle East may increase demand for carbon credits if it continues for a long time. Analysts say energy supply disruptions from the conflict could push some industries back to higher‑emission fuels like coal. This, in turn, could raise emissions and force companies in regulated markets to buy more carbon credits.

The Middle East conflict has already disrupted liquefied natural gas (LNG) supplies. Qatar, a top LNG producer, has halted output at its largest LNG plant. This is due to disruptions in transport routes through the Strait of Hormuz. Qatar supplies about 20% of global LNG output.

LNG provides cleaner fuel for power generation than coal. When gas costs rise sharply or supply is limited, utilities sometimes increase coal use to meet electricity demand. Higher coal use increases carbon emissions. This can lead to higher demand for carbon credits in compliance markets.

Carbon Credits 101: How the Market Responds

A carbon credit represents one tonne of greenhouse gas emissions reduced, avoided, or removed from the atmosphere. Companies must hold carbon credits to meet emissions limits in regulated markets. These markets are part of government climate policy.

Compliance carbon markets, like emissions trading systems (ETS), require companies to lower their emissions. If they can’t, they must buy credits to stay within a limit.

Over 113 carbon pricing systems are in use worldwide. This includes ETS and carbon taxes, which cover about 28% of global greenhouse gas emissions.

In compliance markets, rising emissions usually increase demand for allowances or carbon credits. If companies cannot reduce emissions fast enough, they buy credits to stay compliant. Strong or rising demand can also influence credit prices.

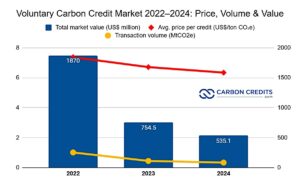

Voluntary carbon markets exist separately from compliance markets. In voluntary markets, companies buy credits to meet internal climate goals, not legal limits.

The voluntary market is smaller but growing. The global voluntary carbon credit market is expected to rise from $1.88 billion in 2025 to $2.29 billion in 2026. It could reach $4.92 billion by 2030.

From Gas to Coal: When Utilities Flip the Switch

The Middle East conflict has pushed energy prices higher. Global natural gas and oil prices climbed because of risks to supply routes such as the Strait of Hormuz, a key passage for crude oil and LNG.

When gas prices rise, utilities may switch from gas‑fired generation to coal, which is cheaper but emits more CO₂. Analysts observed that fuel switching happened in 2022 after Russia invaded Ukraine. European gas supply was disrupted, so utilities turned to burning more coal.

Coal prices have also risen in response to supply pressures. Some markets saw thermal coal prices climb about 26%, reaching highs not seen in more than two years.

Such shifts can put pressure on emissions limits in regulated markets. Higher emissions would require companies to buy more compliance credits to avoid penalties. This dynamic is central to why analysts say carbon credit demand could rise if disruptions persist.

Compliance Markets Under Pressure, So Who Pays the Price?

Compliance carbon markets form the largest portion of carbon credit demand. These include emissions trading systems in Europe, China, and the U.S., and expanding carbon pricing schemes globally. The Middle East conflict could affect these markets, which shows how energy security and climate policy are connected.

Demand for carbon credits depends on how countries and companies aim to meet climate goals, like those in the Paris Agreement. This agreement aims to limit global warming to below 2°C. Compliance markets set legal limits, and voluntary markets support corporate climate goals.

If more companies switch to coal and emissions go up, compliance markets might see a higher demand for allowances or credits. This happens as companies try to stay within legal limits. This could result in higher carbon prices and tighter markets, depending on how regulators respond.

In the European Union Emissions Trading System (EU ETS), companies must hold allowances equal to their emissions, or face fines. The EU is considering reforms to improve market stability and balance supply and demand for allowances. This scheme has been a key tool for reducing emissions in Europe since 2005.

In addition, more sectors are entering compliance markets. For example, China’s national ETS covers key industrial sources. It accounts for a big part of emissions from the world’s largest emitter.

Any rise in emissions from fuel switching could increase demand in these established markets. However, the exact impact will depend on how long energy disruptions continue and whether regulators adjust compliance caps or other rules.

Voluntary Market Volatility: Green Goals on Hold?

Global carbon pricing revenues topped over $100 billion in 2023 and in 2024. The World Bank reports that around $69 billion came from emissions trading systems and $33 billion from carbon taxes. This amount covers nearly 24% of global greenhouse gas emissions, which reflects the growing scale of these markets.

- RELATED: 2026 Could Redefine Voluntary and Compliance Carbon Market Convergence, with Japan Leading the Way

While compliance demand may rise if emissions increase, the outlook for the voluntary market could differ.

According to analysts, an energy crisis may temporarily constrain corporate spending on voluntary credits. High energy prices raise operating costs. This may lead companies to delay voluntary purchases as they will focus more on their core operations instead.

High-integrity voluntary markets have grown recently. This growth is driven by corporate net-zero commitments and new standards. Companies increasingly seek credits that meet quality criteria such as compliance eligibility, durability, and third‑party verification.

Sudden economic strains or changes in energy costs could quickly change how companies buy.

The Ripple Effect: Energy Security Meets Climate Action

A prolonged Middle East conflict could have ripple effects beyond energy prices. Disruptions to LNG supply may push some utilities toward higher‑emission fuels, raising emissions levels. That could drive demand for carbon credits in regulated markets where companies must meet emissions limits.

At the same time, short‑term pressures from high energy costs could slow voluntary demand as companies focus on operational priorities. The overall direction of carbon credit demand will depend on the duration of energy supply disruptions, policy responses by regulators, and the pace of the global energy transition.

Carbon markets are an evolving part of climate policy, linking energy markets and climate goals. As energy security concerns grow, the role of carbon credits in balancing compliance and emissions reductions may attract more attention from policymakers, investors, and companies in the coming years.