China is backing a Beijing-based startup called Orbital Chenguang with about 57.7 billion yuan ($8.4 billion) in credit lines to build space-based data centers, according to media reports. The funding comes from major state-linked banks and signals one of the largest known investments in orbital computing infrastructure.

The move highlights a growing global race to build computing systems in space. It also puts China in direct competition with companies like SpaceX, which is exploring space-based data infrastructure, too.

Orbital Chenguang Builds State-Backed Space Computing System

Orbital Chenguang is a startup in Beijing supported by the Beijing Astro-future Institute of Space Technology. This institute works with the city’s science and technology authorities.

The company has received credit line support from major Chinese financial institutions, including:

- Bank of China,

- Agricultural Bank of China,

- Bank of Communications,

- Shanghai Pudong Development Bank, and

- CITIC Bank.

These are credit lines, not fully deployed cash. But the scale shows strong institutional backing.

The project is part of a wider national strategy focused on commercial space, AI infrastructure, and advanced computing systems.

China’s state space contractor, CASC (China Aerospace Science and Technology Corporation), has shared plans under its 15th Five-Year Plan. These include ideas for large-scale space computing systems, aiming for gigawatt power.

Space Data Center Plan Targets 2035 Gigawatt Capacity

According to Chinese media reports, Orbital Chenguang plans to build a constellation in a dawn-dusk sun-synchronous orbit at 700–800 km altitude. The long-term target is a gigawatt-scale space data center by 2035.

The development plan is divided into phases:

- 2025–2027: Launch early computing satellites and solve technical barriers.

- 2028–2030: Link space-based systems with Earth-based data centers.

- 2030–2035: Scale toward large orbital computing infrastructure.

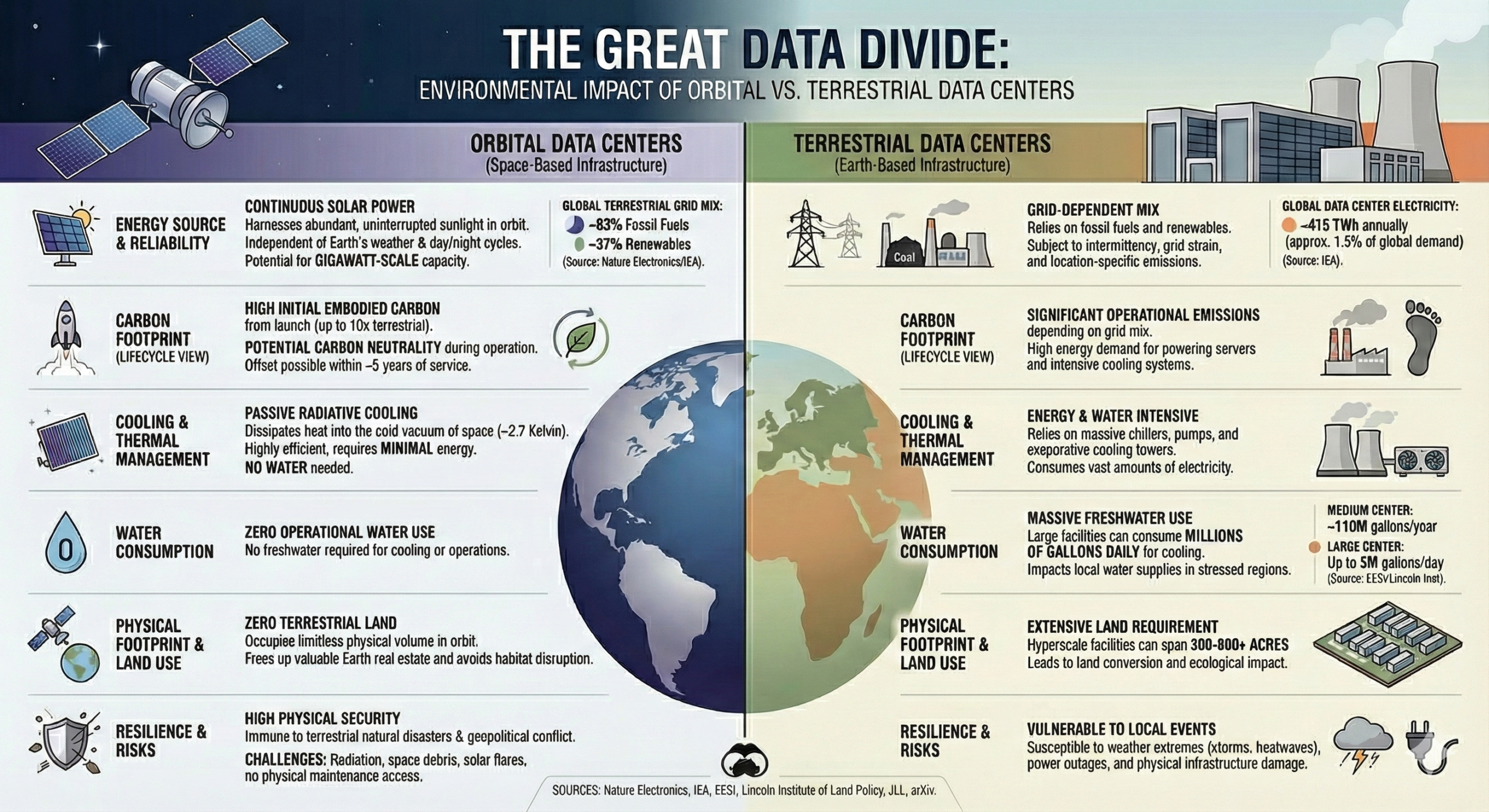

The design relies on continuous solar energy and natural cooling in space. These features could reduce reliance on land-based power grids and cooling systems.

China has proposed two satellite constellations to the International Telecommunication Union (ITU). These plans include a total of 96,714 satellites. This shows China’s long-term goals for space infrastructure and spectrum control.

The AI Energy Crunch Pushing Computing Into Orbit

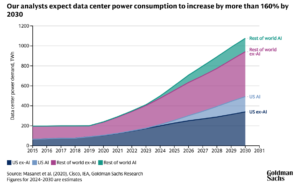

The push into orbital data centers is closely linked to rising AI demand. Global data centers consumed about 415–460 terawatt-hours (TWh) of electricity in 2024, equal to roughly 1.5%–2% of global power use. This figure is rising quickly due to AI workloads.

Some industry projections show demand could exceed 1,000 TWh by 2026, nearly equal to Japan’s total electricity consumption.

AI systems require massive computing power, which increases energy use and cooling needs. In many regions, electricity supply—not hardware—is now the main constraint on AI expansion.

China’s strategy aims to address this by moving part of the computing load into space, where solar energy is more stable and continuous.

Carbon Impact: Earth vs Space Computing Trade-Off

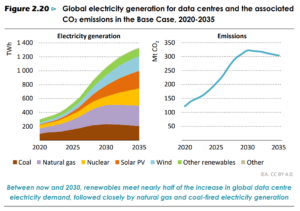

Data centers already create a large carbon footprint. In 2024, they emitted about 182 million tonnes of CO₂, based on global electricity use of roughly 460 TWh and an average carbon intensity of 396 grams of CO₂ per kWh. This is according to the International Energy Agency report, as shown in the chart below.

Future projections show even faster growth. The sector could generate up to 2.5 billion tonnes of CO₂ emissions by 2030, driven by AI expansion. This is where orbital systems come in. They aim to reduce emissions during operation by using:

- Continuous solar energy,

- Passive cooling in vacuum conditions, and

- Reduced dependence on fossil-fuel grids.

However, space systems also introduce new emissions. Rocket launches used about 63,000 tonnes of propellant in 2022, producing CO₂ and atmospheric pollutants. Lifecycle studies suggest that over 70% of emissions from space systems typically come from manufacturing and launch activities.

In addition, hardware in orbit often has a lifespan of only 5–6 years, which increases replacement cycles and launch frequency. This creates a key trade-off:

- Lower operational emissions in space, and

- Higher lifecycle emissions from launches and manufacturing.

Research suggests that, in some scenarios, orbital computing could produce up to 10 times higher total carbon emissions than terrestrial systems when full lifecycle impacts are included.

China’s Expanding Space-Tech Ecosystem

Orbital Chenguang is not operating alone. Several Chinese companies are working on similar in-orbit computing systems, including ADA Space, Zhejiang Lab, Shanghai Bailing Aerospace, and Zhongke Tiansuan.

These firms are developing satellite-based computing and AI processing systems. This shows that orbital computing is not a single project. It is part of a broader national push across government, industry, and research institutions.

China’s space strategy combines commercial space growth with national technology planning. It aims to build integrated systems that connect satellites, cloud computing, and terrestrial networks.

The Space-AI Arms Race: China vs SpaceX vs Google

China is not alone in exploring space-based computing. Companies in the United States are also developing orbital data infrastructure concepts. These include early-stage research and private sector projects by firms such as SpaceX and Google.

However, these systems face major challenges:

- High launch costs,

- Heat and thermal control issues,

- Limited data transmission bandwidth, and

- Hardware durability in space.

Despite these challenges, interest is growing because AI demand is rising faster than Earth-based infrastructure can scale. The competition is now moving toward who can solve energy and computing limits first—on Earth or in space.

Market Outlook: AI, Energy, and Space Infrastructure Converge

The global data center industry is entering a period of rapid expansion. Electricity demand from data centers could double by 2030, driven mainly by AI workloads and cloud computing growth. Power supply is becoming a limiting factor in many regions.

At the same time, the global space economy is expanding into a multi-hundred-billion-dollar industry, supported by satellites, communications, and emerging technologies like orbital computing.

- Orbital data centers sit at the intersection of three major trends: rapid AI growth, rising energy constraints, and expansion of space infrastructure.

China’s $8.4 billion credit-backed push through Orbital Chenguang signals confidence in this convergence. However, key barriers remain, such as high cost of launches, engineering complexity, short satellite lifespans (5-6 years), and regulatory uncertainty in orbital systems.

Because of these limits, orbital data centers are unlikely to replace Earth-based systems in the near term. Instead, they may form a hybrid system where some workloads move to space while most remain on Earth.

Space Is Becoming the Next Data Center Frontier

China’s investment in Orbital Chenguang marks one of the most significant moves yet in the emerging field of space-based computing. Backed by major Chinese banks, municipal science institutions, and national space contractors like CASC, the project shows how seriously China is treating orbital infrastructure.

The strategy connects AI growth, energy demand, and climate pressures into a single long-term vision. But the trade-offs are complex. Orbital data centers may reduce operational emissions, but they also introduce high lifecycle carbon costs and major technical challenges.

The global race is now underway. With companies like SpaceX, Google, and Chinese tech firms exploring similar ideas, space is becoming a new frontier for digital infrastructure. The outcome will depend on whether orbital systems can scale efficiently—and whether their carbon benefits can outweigh the emissions cost of building them.