Amazon, alongside five other major companies, has committed to purchasing carbon offset credits to support the preservation of the Amazon rainforest in the Brazilian state of Para. This agreement, valued at around $180 million, marks a significant step toward protecting one of the world’s most vital ecosystems in the fight against climate change.

Amazon LEAF Coalition’s First Amazon Deal

The carbon credits will be purchased through the LEAF Coalition, a forest conservation initiative co-founded by Amazon in 2021 in partnership with other companies and governments, including the United States and the United Kingdom. This deal is the LEAF Coalition’s first agreement in the Amazon rainforest, the world’s largest tropical forest. It plays a critical role in curbing climate change by absorbing massive amounts of greenhouse gases.

The Para state government and the LEAF Coalition announced the agreement during New York Climate Week, where more than 900 climate-focused events were held alongside the UN General Assembly.

Governor Helder Barbalho of Para shared details of the deal. He noted that the state will retain only the portion of the sales proceeds necessary to fund its ongoing efforts to reduce greenhouse gas emissions. The remainder of the funds will be distributed to local communities, including Indigenous peoples, former slave descendants, traditional extractivist communities, and family farms.

Barbalho emphasized the symbolic importance of the agreement, stating:

“Clearly it sends an important message: A company with a name referencing the Amazon making its first purchase with a state in the Amazon.”

Supporting Nature Conservation Efforts and Indigenous Communities

Amazon will purchase carbon offset credits alongside other big companies such as drug and chemical maker Bayer, consultancies BCG and Capgemini, H&M, and the Walmart Foundation. The fund will help protect the Amazon rainforest from deforestation.

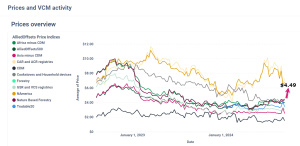

Under the agreement, 5 million carbon credits will be bought at $15 per credit, which is well above the average price of $4.49 for credits linked to nature conservation, per Allied Offsets data.

Each credit represents a reduction of one metric ton of carbon emissions through efforts to reduce deforestation in Para. This forest conservation initiative covers from 2023 to 2026.

An additional 7 million carbon credits will also be made available for purchase by other companies. Governments from the U.S., U.K., and Norway have guaranteed a portion of these credits, committing to buying them if other corporations do not.

How Significant is This Carbon Offset Deal?

The Amazon rainforest is a critical carbon sink that helps mitigate climate change. However, Para has been the Brazilian state most affected by deforestation since 2005. Despite the challenges, there has been progress, with deforestation rates in Para decreasing since 2021.

In the first eight months of 2023, an area larger than New York City was deforested in Para, representing a 20% decline from the previous year.

Para is also set to host the UN COP30 Climate Summit in 2025. This aligns with President Luiz Inácio Lula da Silva’s efforts to restore Brazil’s environmental leadership after years of increased deforestation. The hosting of COP30 reflects Brazil’s renewed commitment to environmental protection and sustainability.

For Amazon, this purchase aligns with its broader environmental initiatives and corporate responsibility goals. And that includes the Climate Pledge, which aims to achieve net zero carbon emissions by 2040.

Supporting Para’s nature conservation project through carbon credits is a big part of its carbon neutralization strategy. The retail giant is focusing on slashing carbon emissions within its operations as well as backing carbon-neutral initiatives.

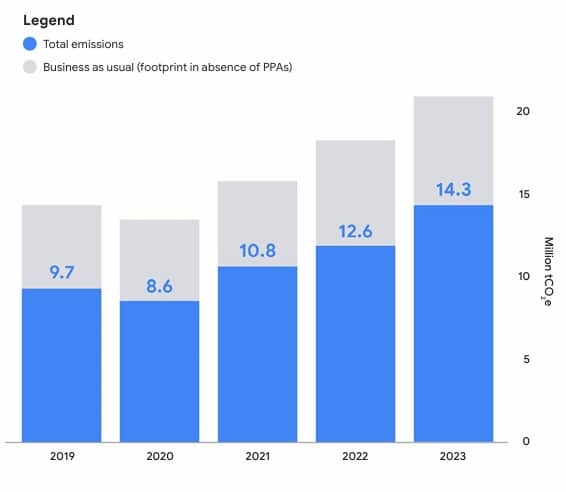

In 2023, Amazon cut its total carbon emissions by 3%, thanks to an 11% reduction in Scope 2 emissions (electricity) and a 5% decrease in Scope 3 emissions (supply chain). However, Scope 1 emissions (direct operations) rose by 7%, mainly due to increased transportation fuel use.

To tackle the increasing emissions, Amazon invests in various carbon neutralization efforts. The company partners with projects that protect tropical forests, such as the LEAF Coalition. It also supports programs that enhance forest carbon capture and improve local livelihoods while investing in new technologies for efficient carbon capture.

A Boost for Carbon Offset Markets

This deal comes at a time when global demand for carbon credits has slowed. However, major tech companies like Microsoft, Meta, and Google have recently invested in carbon offsets in Brazil, underscoring the growing recognition of nature-based solutions to combat climate change.

Amazon’s statement about the purchase highlighted the importance of preserving tropical forests in addressing climate change. The company’s involvement in this deal, especially given its association with the rainforest through its name, sets a strong example for corporate involvement in environmental conservation.

In addition to the carbon credit deal, Para’s state government is working to enhance supply chain transparency to combat deforestation. This is particularly true in the cattle industry. Cattle ranching has been a significant driver of deforestation in the region.

Governor Barbalho further announced that by 2026, the Para government aims to have full traceability of cattle supply chains, helping to prevent illegal deforestation and ensuring sustainable land-use practices.

While the purchase of carbon credits alone will not solve deforestation challenges, it reflects the critical role that corporations can play in financing conservation initiatives. This $180 million collaborative approach, involving governments, corporations, and local communities, offers a model for how other regions could approach forest conservation and climate action.

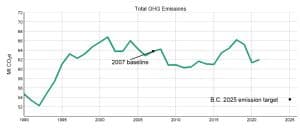

Source: Climate Change Accountability Report, British Columbia

Source: Climate Change Accountability Report, British Columbia

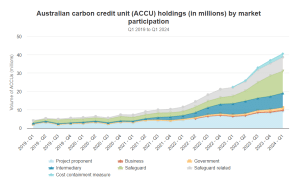

Source: IEA

Source: IEA

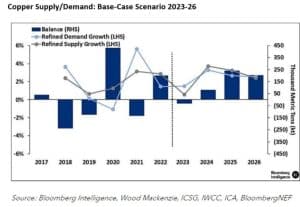

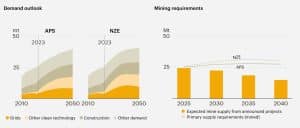

Source: Google

Source: Google